Eye of the Storm?

Are stocks back to a bull run, or is this just a reprieve?

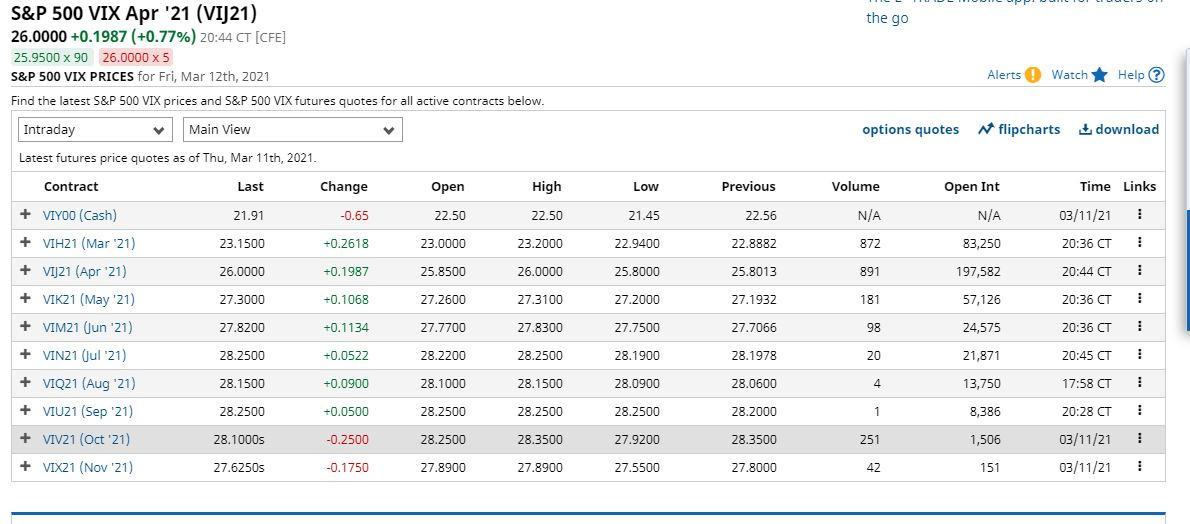

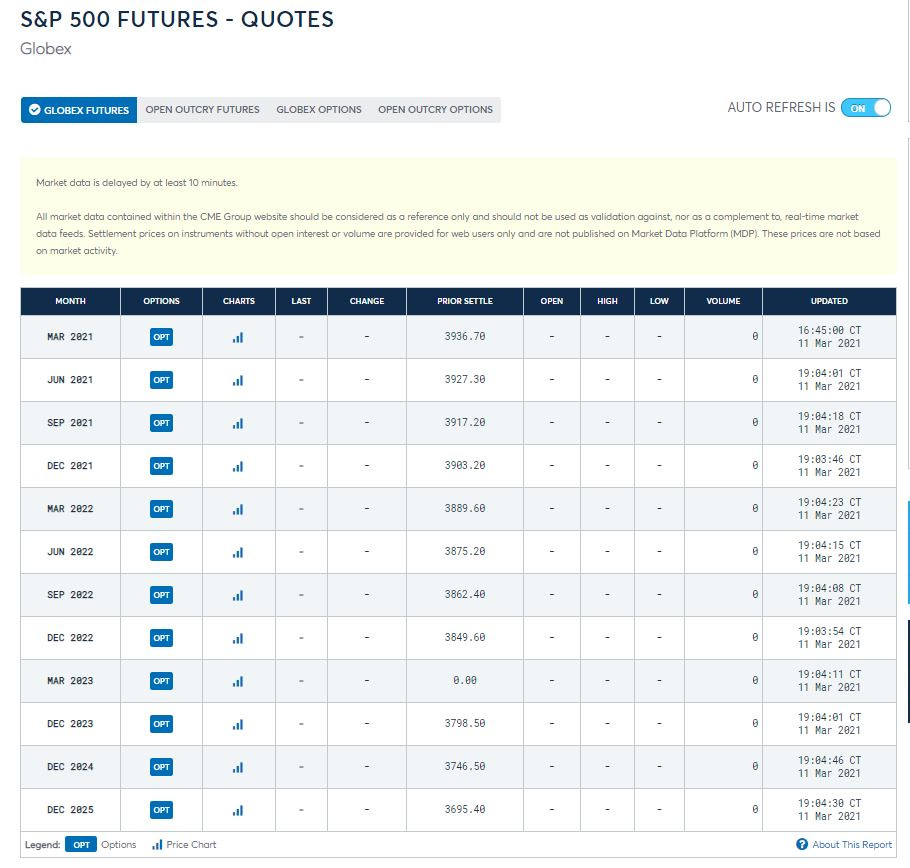

Right now, markets are predicting something in-between a crash and a bull market, for the rest of the year. VIX futures reveal expectations of higher volatility for the rest of 2021, after March, and S&P 500 futures predict the index will finish the year down over 6% from the new high reached today.

Meanwhile, 5-year inflation expectations have been on the rise a bit since the end of last month, which, if the 2.05% rate revealed here is to be taken seriously, should not cause the Fed to even think about raising rates yet.

The Fed targets PCE core inflation, the rate of which is typically .3-.4% below that of the CPI, the latter of which is the measure used in the graph above.

I also found this Cleveland Fed estimate of 10-year inflation expectations which look even lower than those of the 5-year horizon above.

So, have markets been wrong to assume that the Fed will raise rates sufficiently in 3 years to cut down the path of GDP growth for outer years, due to inflation fears? Not necessarily.

The Fed has historically acted upon overly optimistic internal inflation forecasts and pessimistic estimates of the natural rate of unemployment, though they are now targeting average inflation and say they are putting a greater emphasis on the full employment part of their mandate. To quote one paragraph from the Fed’s most recent monetary policy report:

The revised statement says that "the Committee's policy decisions must be informed by assessments of the shortfalls [emphasis added] of employment from its maximum level" rather than by "deviations"—the word used in the earlier statement.3 In previous decades, inflation tended to rise noticeably in response to a strengthening labor market. It was sometimes appropriate for the Fed to tighten monetary policy as employment rose toward its estimated maximum level in order to stave off an unwelcome rise in inflation. The change to "shortfalls" clarifies that, in the future, the Committee will not have concerns when employment runs at or above real-time estimates of its maximum level unless accompanied by signs of unwanted increases in inflation or the emergence of other risks that could impede the attainment of the dual-mandate goals.

The paragraph following the one quoted above discusses their average inflation targeting approach, which seems like an improvement over flat inflation targeting, but the time frame over which inflation is to average 2% isn’t specified, leaving markets to guess.

Unfortunately, in the very next paragraph, financial stability is mentioned as a condition for achieving their dual mandate. The path of GDP growth does vastly more to determine financial stability than financial stability does to determine GDP growth.

Also, it would be nice if the Fed’s dual mandate weren’t contradictory, given that inflation targeting has a disinflationary bias, which undermines full employment. Given the state of politics in the US, perhaps we’re fortunate policy is only this incoherent.

All that said, my own stock crash indicator is still predicting an S&P 500 crash of at least 15% over several weeks to a few months, and more strongly than before, with the caveats mentioned previously, in addition to the fact that YOY numbers right now are being compared to those near the low of the stock crash last year. The indicator has never been incorrect since the explicit 2% Fed inflation targeting regime began, but perhaps this time will be different. That’s why my puts on the NASDAQ index are hedged with calls, in a 2-1 ratio.

Note: This post does not constitute financial/investment advice. Advice should be sought from fiduciary professionals who can take individual investor charactersitics and circumstances into account. Warnings issued about changes in stock market prices are based on historical data, which may not necessarily reflect future price movements.