Market Outlook, for Week Ending 03/05/2021

Not boring.

In statistics, noise is effectively silence, and out of the silence of ambiguity early last week, the stark thunder of a signal of a potential large downward stock price movement startled me. This was not the prediction of a recession, or even close, but merely of a slowdown in NGDP growth path of just short of .4%, leading to a downturn in the S&P 500 in the 13% range. By Friday, the clouds grew darker, however, and the wind picked up noticeably.

If we ignore some potential important differences between the current situation and those in which prior signals never failed during the last monetary policy regime, since Friday, we should now expect a fall in the S&P 500 of almost 18.5% with a greater than 95% probability. However, we should not ignore differences between this and prior situations, as we are in a new monetary regime, namely average inflation targeting, and we are in an era of extraordinary interventions in the capital and credit markets by the Fed.

These differences would be important, even if the current discount rates for broad stock indexes were not so low. The current estimated discount rate for the S&P 500 is a bit over 2.5%, making it relatively sensitive to crashing in response to negative economic news, but also subject to booming in response to better than expected news. It will not take much in terms of Fed mistakes, or corrective action to make a huge difference in outcomes over the coming weeks.

Hence, and this is not investment advice, but merely a statement of my own position on the broad stock indexes, I have bought near the money puts and calls on major indexes in a 2:1 ratio, respectively. I obviously do not see this situation as an opportunity for unhedged bets, and expect high volatility to continue for several weeks, at least.

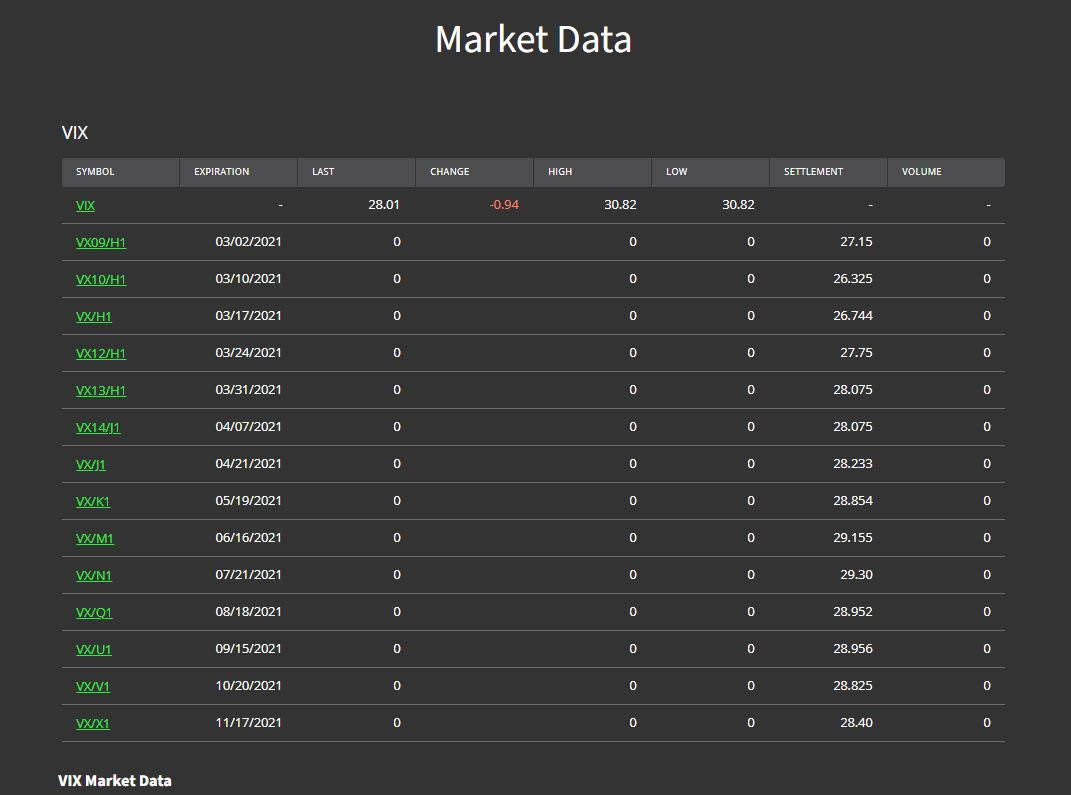

This is consistent with a steepness in the VIX futures market going forward, after a brief inversion in the first few weeks of March and the sharpest drop in the 5-year forward expected inflation rate since the stock market started climbing out of the pandemic crash last April.

Then, there are the Treasury yields, which really spiked at the end of last week, that, coupled with falling inflation expectations and stock indexes, would seem to be a really good sign of expected monetary tightening:

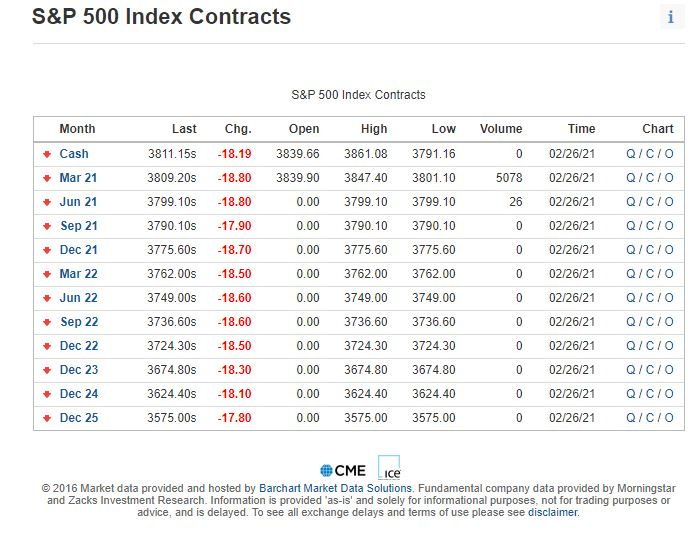

However, S&P 500 futures, while pessimistic, are not predicting a crash, but more of a gentle decline of the index for the remainder of the year:

Of course, a market signal indicator would be worth little if it were not ahead of the markets, so I feel comfortable with an outlook potentially significantly worse than markets currently anticipate.

Also, even if you buy the inflation trade notion, the Fed has never engineered a soft landing, so what begins as inflation concerns can easily be turned into disinflationary concerns, given the historically heavy hand of the Fed.

It will be an interesting next several weeks.

Note: This post does not constitute financial/investment advice. Advice should be sought from fiduciary professionals who can take individual investor charactersitics and circumstances into account. Warnings issued about changes in stock market prices are based on historical data, which may not necessarily reflect future price movements.