Market Outlook, for Week Ending 04/02/2021

Is better good enough?

First, let me make a confession. I’d been eyeballing the growth in the S&P 500 since the pendemic began and thinking that it had grown below the pre-pandemic trend rate. Now, after having done the calculations, I see that it’s actually grown above the pre-crisis trend rate. It should have been obvious, considering that the index reached the previous high roughly halfway between the crash and today. But, confirmation bias is very strong.

The Fed has historically allowed growth to fall below trend after recessions, but fortunately this time is different. Hence, the Fed has been doing a better job than I’ve indicated. I would apologize if they knew I exist.

Adding to this good news, the 5 -year forward inflation expectations rate has again reached its precious post-recession high.

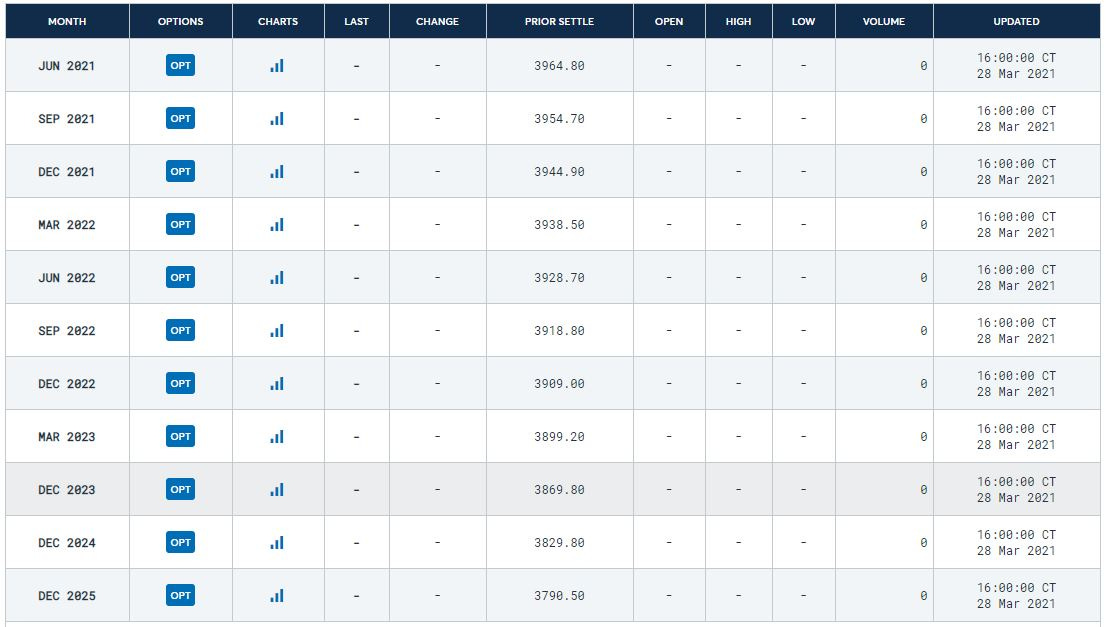

This doesn’t change my recent stance, however, that we’re flirting with a tipping point, beyond which the market doesn’t think the Fed will maintain it’s low Fed Funds rate, and will hence overreact when slowing economic growth. Fortunately, a recent small real shock and some assurances from the Fed have given the market a little more room to run, but concerns are still apparent. S&P 500 futures are still pessimistic for the remainder of the year.

Also, VIX futures are predicting a rougher ride for the market soon, for the remainder of the year, at least, though the pessimism has eased some over the past week.

Overall, the Fed’s done a bit better than in post-recessions past, and markets are indicating that a stock market crash is somewhat less likely than just a few weeks ago. Hence, there’s no reason to believe there will be anything worse than a mildly down week ahead, and it could be a modestly good week.

It’ll be intersting to see what this eventually means for my previously reliable stock market boom/bust indicator. It may require calibration, or become too irrelevant to matter.