Market Snapshot, and Outlook for Week Ending 06/11/2021

Market Snapshot, and Outlook for Week Ending 06/11/2021

Flat.

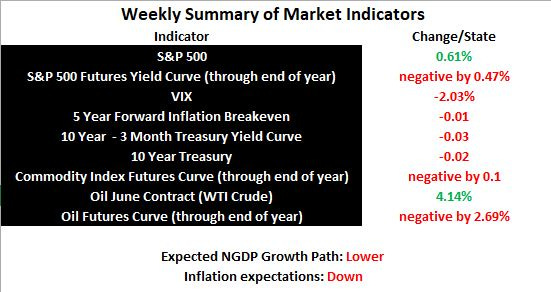

The future expected path of US NGDP growth fell a bit last week, as the VIX reached a new post-pandemic low of 16.42. This indicates expectations for a weak post-pandemic recovery continue to set in, as fears of potential negative shocks wane.

The S&P 500 was up last week, but has been flat since late April, and the slightly negative futures curve indicates it will remain that way through the end of the year, and even into 2025, sans unforeseen positive events. The rise in the index last week was likely due to a falling discount rate.

As I mentioned in the summary of last week’s changes in market indicators, the implied future NGDP growth path in the S&P 500 data is not much over 4%, with most of that being inflation, rather than real growth.

Why will real growth be so low? I speculate that some workers who were put out of work by the pandemic will not return to work, or at least will work fewer hours, and that perhaps the decline in population growth was accelerated on a permanent basis. It is also possible that the fiscal stimulus and investment efforts are having a net effect that ranges from somewhat negative to perhaps slightly positive. If the market forecast is correct, this will be very disappointing for Democrats, in particular.

Links to Data

https://fred.stlouisfed.org/series/SP500

https://www.cmegroup.com/trading/equity-index/us-index/sandp-500.html

https://www.cnbc.com/quotes/.VIX

https://fred.stlouisfed.org/graph/?g=Ee9i

https://fred.stlouisfed.org/series/T10Y3M#0

https://fred.stlouisfed.org/series/DGS10

https://www.cmegroup.com/trading/agricultural/commodity-index/bloomberg-commodity-index.html

https://oilprice.com/oil-price-charts/

https://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_quotes_globex.html