Market Snapshot, and Outlook for Week Ending 06/04/2021

Market Snapshot, and Outlook for Week Ending 06/04/2021

Real problems ahead.

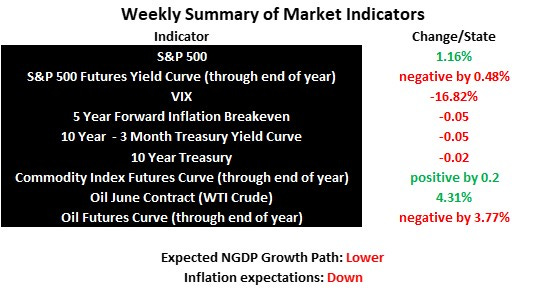

Nominal GDP growth expectations seemed to decline slightly last week, while those for real growth ticked upward. It was thus, a week of slight improvement in economic outlook. This is evident in the fact that the S&P 500 index, for example, rose a bit more than 1%, while inflation expectations fell just a bit.

As a reminder, it is easy to read too much into such slight changes in weekly figures. So, I decided to go beyond the weekly numbers and decode what the stock market has to say about real and nominal GDP growth going forward.

What the S&P 500 index reveals about future nominal growth is a question I’ve addressed previously, and it has NGDP growth roughly on the pre-pandemic trend. This is seen both in the fact that the S&P 500 index returned to it’s pre-crisis trend, and that the current S&P 500 level is pricing in about 4% growth. I find this by multiplying Friday’s S&P 500 closing level, 4204.11, by .04, which yields expected annual nominal earnings of $168.16, which is just above the ~$163 level expected if earnings had continued growing at the pre-crisis rate of roughly 4%. This is a back-of-envelop calculation, but good enough to tell us much about what markets expect in terms of real versus nominal GDP growth going forward. By the way, the data I used is found here, and substituting the expected average economic growth rate for the earnings yield is based on the equilibrium condition presented here.

So, if we’re to take indicators of inflation expectations seriously, like the 5 year breakeven rate quoted in my summary of indicators above, we can expect an inflation rate of roughly 2.25% or so over the next 5 years, as a rough adjustment is made to translate the core CPI rate into core PCE rate. This leaves only about 1.75% for real growth. This is lower than even the low real growth rate the US experienced between the Great Recession and pandemic, which was around 2%.

Hence, as stated previously, we can expect a temporary large boost in NGDP growth as the economy continues to reopen, but with somewhat higher inflation than the average over the past generation, but with lower real growth. This will not bode well for getting back to full-employment or higher sustainable wage growth quickly.

Expect the next week to be very much like recent weeks, as it markets continue to believe the Fed’s only willing to tolerate inflation in the range markets are currently predicting.