Market Snapshot, and Outlook for Week Ending 05/28/2021

Market Snapshot, and Outlook for Week Ending 05/28/2021

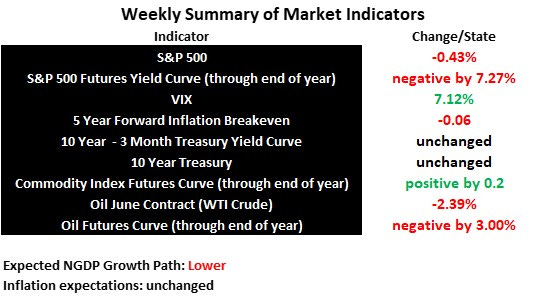

Recovery slipping away?

I’ve been disappointed both by the weak rise of longer term Treasury yields and the stock market sensitivity to the very modest rise that’s occurred. The 10 year rate is still below the pre-pandemic level, which can be construed to mean markets still don’t expect NGDP growth to return to the pre-recession trend on a permanent basis. An alternative perspective is that low Treasury rates reflect the lower global equilibrium rate, and much of the rest of the world hasn’t recovered from the pandemic recession as quickly as the US. I think that means the Fed needs to push harder to raise the equilibrium rate in the US. Future data will us which of these perspectives is closer to the truth.

So, I continue to be a bear on the recovery, and the events of last week don’t contradict that view. The S&P 500 index was down for a third straight week, while the S&P 500 futures curve fell further negative. The VIX again increased. I see no reason to expect a better week ahead, but still don’t anticipate an immediate crash. Of course, crashes are caused by shocks, so we can always be surprised.

More specifically, what I mean by being a bear is that I expect some above normal economic growth in the short-run, but disappointing growth longer-term. I expect it to take longer than necessary to get the US economy back to full-employment, as real factors fade in influence during the recovery.