Pandemic Recovery: The Bear Case

Pandemic Recovery: The Bear Case

Taking stock of forecasts

Before I discuss where the stock market may go, let’s talk about where we’ve been. The S&P 500 returned to it’s pre-recession trend line in March of this year:

This coincided with the return to trend of NGDP:

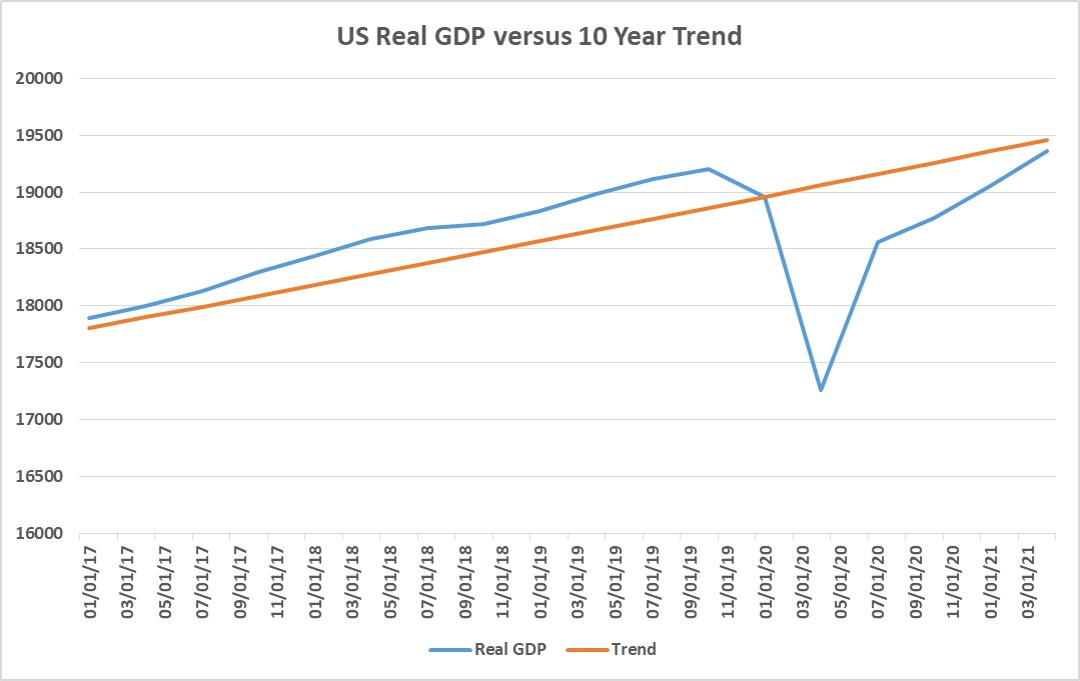

However, real GDP lagged, while inflation spiked. Still, real GDP was obviously close to trend:

Looking at this, it is already tempting to think we won’t see much more, if any, appreciation in the S&P 500 for a while. The Fed could conclude that it’s job is largely done, without some unforeseen downturn. Adding to this view, the S&P 500 futures curve has been negative-to-flat for months, and still is.

But, this is only the beginning of the bear case. Consider the S&P 500 earnings yield. It has not returned to the pre-recession level, which averaged well over 4%. That could mean a good bit of appreciation to come, if not for the earnings and GDP forecasts.

The most recent reported S&P 500 earnings yield is still that from the first quarter, which was 3.23%, with quarterly earnings at $45.97. And, as you can see at that same link, if you add the projected earnings for this year, you end up with $175.67. Without a non-trivial downturn in earnings this year, this should be close to the final number. Given that the today’s closing S&P 500 figure was 4395.64, it implies a 2021 earnings yield of roughly 4%.

Why should we care about the earnings yield? Well, first, it’s the same as the discount rate, and second, the mean S&P 500 earnings yield tends to be very close to the NGDP growth rate over time.

Speaking of the NGDP growth rate, let’s look at 2022. The Hypermind prediction market has Q4 NGDP growth at 4.6%. The S&P 500 forward P/E ratio for that quarter is 4.5%, with projected earnings of $196.16 for the year. That would lead to an index value of 4359.11, which would be down a little less than 1% from today’s close.

Note that all of that negativity is before consideration of possible tax increases that could hit stock prices over the next year or two.

How seriously should earnings forecasts be taken? Well, such forecasts are historically pretty inaccurate. They tend to overestimate earnings. That would seem to be another reason to be bearish, given the usual direction of error.

And what about the Hypermind NGDP forecasts? Market forecasts tend to be the most accurate, but that is currently a small, incomplete market, so its forecasts should be taken with a grain of salt. It does agree however with the afore-mentioned S&P 500 futures market.

So, not only are multiple forecasts with different modalities predicting a bear market for through at least 2022, but they all converge on very similar numbers for the period. So, that’s the bear case.

So, why am I a bit bullish, even over this short period? Perhaps I’m foolish, but I think pre-recession upward productivity trend will continue to surprise, and we’ll see the results sooner rather than later. The pandemic has moved forward some innovation and technology adoption, such as work-from-home, while AI applications continue to branch out at surprising speed. My best guess is that we’ll see the S&P 500 closer to 5000 sometime next year, rather than close to the current level. But, probably better to trust the markets.

{kind=link}

It doesn’t matter much to me whether I’m right or wrong over the next year or so, as I mostly favor a long-run approach.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.