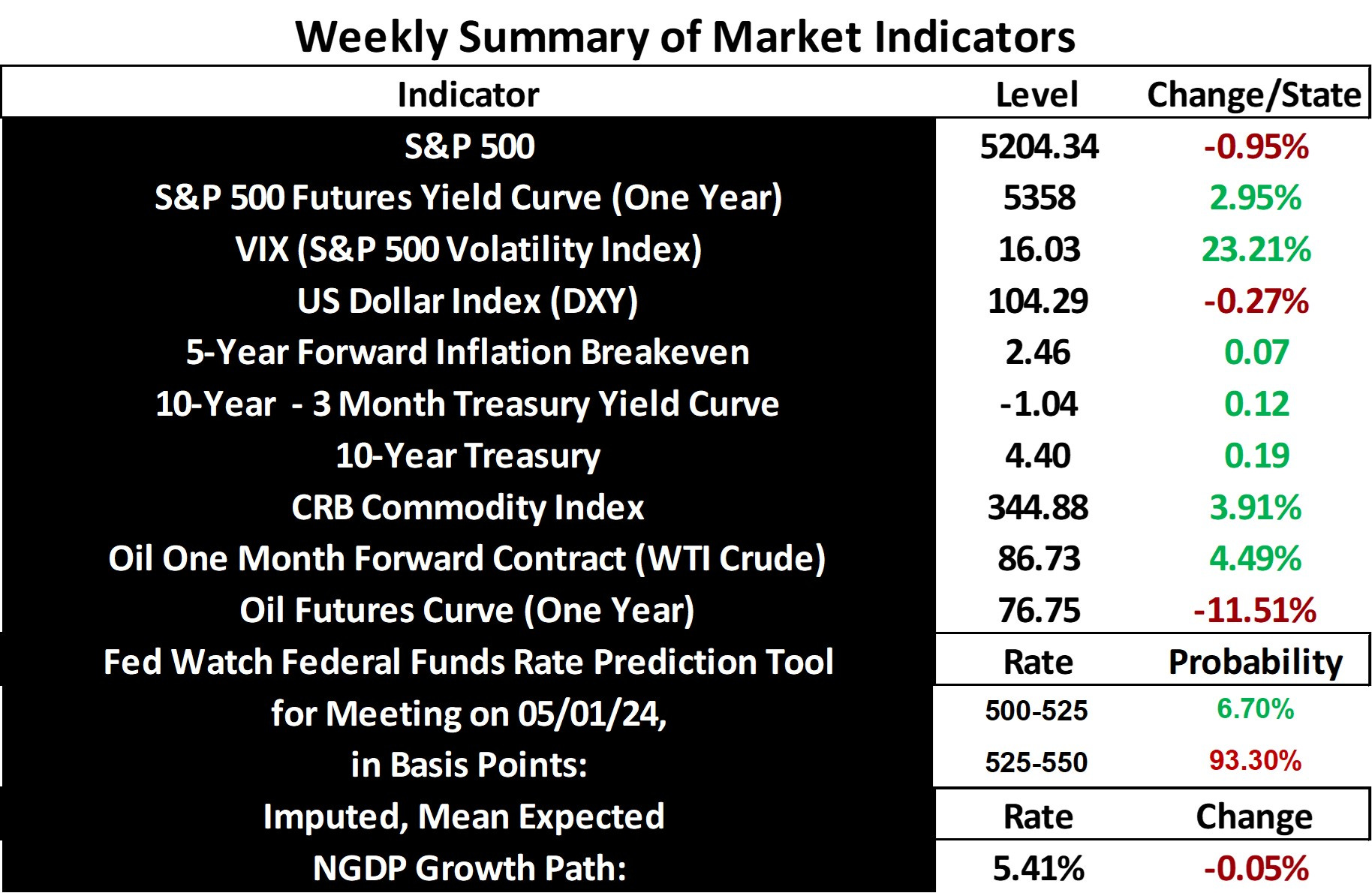

Stock and GDP Outlook, for Week Ending 04/12/2024 (Alternative Form)

Markets Wobble as Inflation Sizzles

Equity markets stumbled last week, shedding gains amidst a decline in expected nominal GDP growth. Volatility surged, hinting at the unease swirling around rising inflation expectations and commodity prices – a trend exacerbated by geopolitical tremors in the Middle East and Russia.

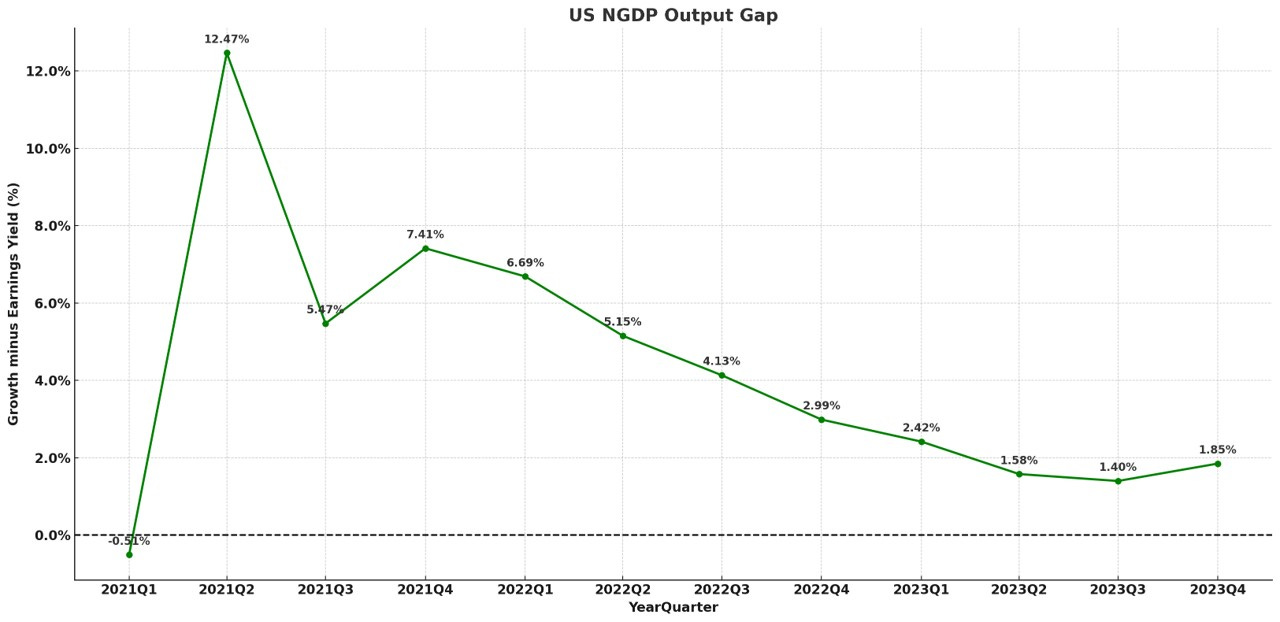

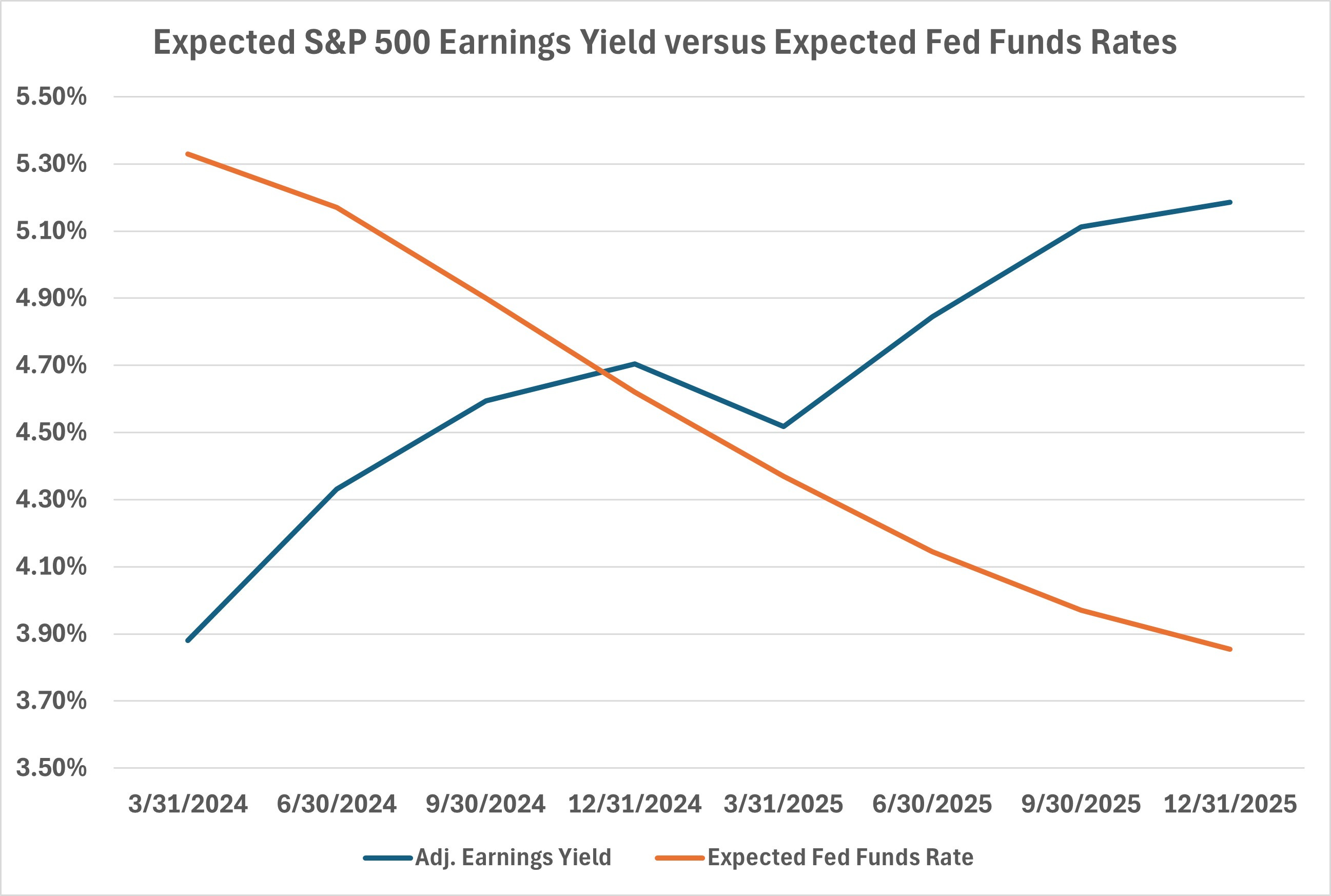

Further evidence of an overheating economy arrived in the form of a robust March jobs report, boasting over 300k new positions. Meanwhile, S&P Global's Q4 earnings release revealed a paltry earnings yield of 4.01% for the S&P 500, a stark contrast to the 5.86% NGDP growth. This divergence signals a widening output gap.

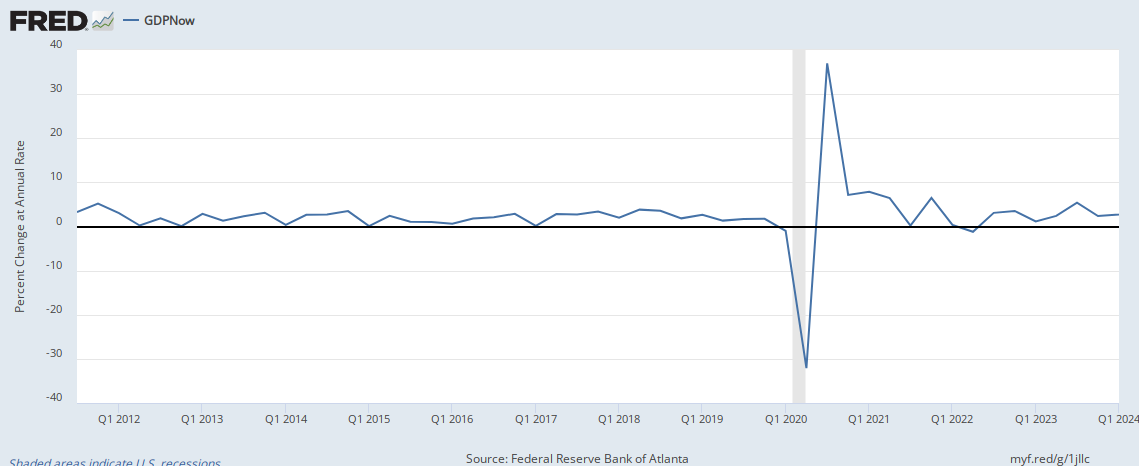

The gap for Q1 likely mirrors these figures, if not worse. Projected earnings yield dips to 3.88%, set against a near-identical NGDP growth prediction. Consult recent GDPNow and inflation nowcasts from the Federal Reserve for confirmation.

{kind=link}

Consequently, a stubbornly positive output gap persists. Realistically, NGDP growth won't ease until the Fed Funds rate surpasses it. In a hot economy, absent government default risk, the neutral nominal interest rate tracks NGDP growth. Until now, the assumption has been a gradual decline in real growth; that assumption is now being tested. To rein in NGDP growth amidst a nominal shock, the real neutral rate must drop substantially.

Yet, markets anticipate an economic slowdown and lower interest rates – a puzzling prospect given recent, expansionary Fed moves. Could a true GDP slowdown be the markets' secret, a real shock hiding in plain sight?

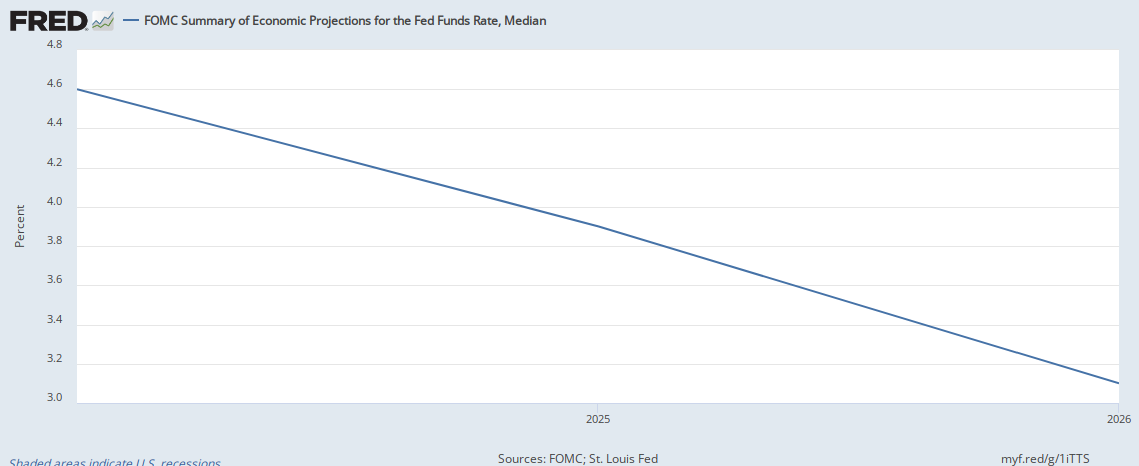

Rising expected earnings yield and a negative yield curve hint at a future passive tightening of monetary policy – a seemingly unlikely scenario considering recent trends. Recent downward revisions to NGDP and jobs figures are unlikely to shift this trajectory; inflation expectations stubbornly point to continued overheating. A lower Q1 NGDP print would do little to alter this course. Similarly, the oil futures curve implies that the recent spike in oil prices is ephemeral, with one-year futures nearly 12% below spot prices. Tellingly, both markets and the Fed itself envision rate cuts, with the Fed Funds rate projected at just 3.1% by 2026.

{kind=link}

Thus, the mystery deepens: how will the economy cool against a backdrop of Fed easing and persistent inflationary pressure? What insight do markets possess that remains obscured to the rest? The best guess is the Fed will suddenly see the error in its ways and begin to correct. While recession isn't on the immediate horizon, heightened caution is warranted.

PS: Please let me know what you think about this style, versus my usual more perfunctory approach.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data:

Excellent presentation. Thank you very much for your kindness to expose your valuable analysis on Substack for free.

Cheers from Helsinki.