Stock and GDP Outlook, for Week Ending 04/26/2024

Stock and GDP Outlook, for Week Ending 04/26/2024

Risks Still Rising

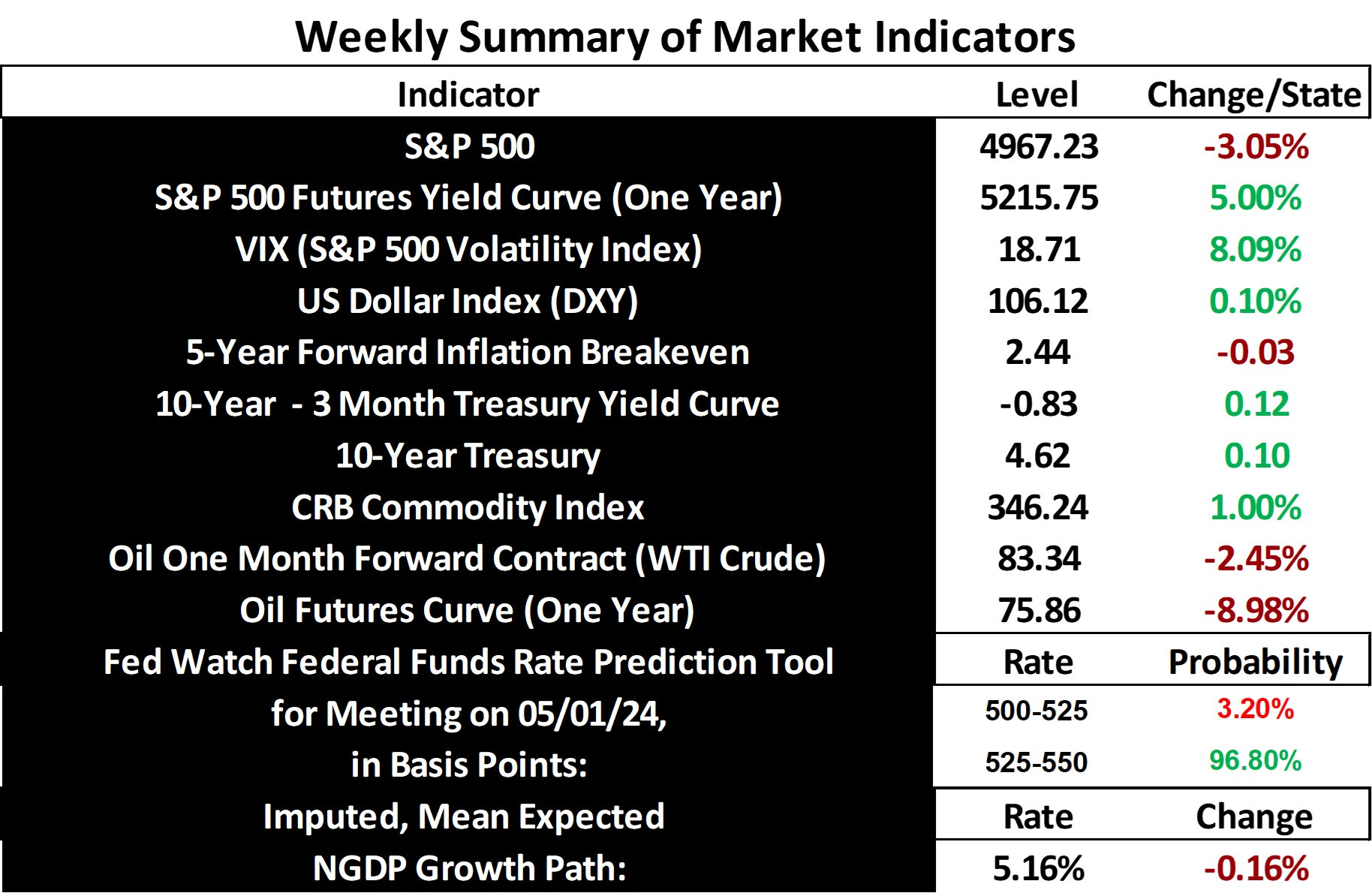

Stock prices and the mean expected NGDP growth rate fell sharply last week, as long-term Treasury yields continued to rise, while inflation expectations eased a bit. Expected inflation remains above the Fed’s 2% target, however. Hence, we should not be surprised to see more down days for stocks in the near future, save for some positive real shocks.

Commodity prices have been climbing this year, due in no small part to conflict-related supply disruptions in the Middle East and elsewhere, but this is not primarily responsible for the higher inflation expectations. As stated repeatedly in recent weeks, NGDP growth is simply too high. I do not expect relief in the commodity markets before November, because the disruptions to supply are, at least in part, due to a coordinated effort on the part of Russia and Iran, supported by China, to influence the American election. The goal, I surmise, is to raise prices in the US and create a sense of chaos in US foreign policy. That is, unless the Biden administration can manage to better deter or otherwise prevent such disruptions. Oil futures suggest that these supply disruptions should begin to ease considerably within a year.

I mentioned last week that if the Fed were to slam on the brakes to bring the economy immediately back into equilibrium, the S&P 500 would decline around 35%. The index is now down more than 5% since reaching its all-time high at the end of March. It will likely need to decline another 2.5% or so, if the Fed lowers inflation expectations back down to target, allowing the economy to glide back down to equilibrium growth rates very gradually.

Of course, either of these outcomes is possible, as are more extreme outcomes, but it’s more likely that we’ll see something closer to the glide path scenario that markets have been predicting for several months. The S&P 500 certainly isn’t predicting a sharp downturn right now, though the rising VIX does indicate increased risks for negative nominal and real shocks in the near future.

So, yet again, there’s good reason for traders to proceed with yet even more caution as we approach this election season and numerous, complex cross currents compete to determine the direction of the economy.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data:

Thank you for exposing factors that influancing the economic conditions and consequently the equity market.

The comprehensible writing helps the reader to understand the content and make investment decisions with confidence.

Kind Regards from Helsinki.