Stock and GDP Outlook, for Week Ending 04/29/2022

Stock and GDP Outlook, for Week Ending 04/29/2022

Closer to Bottom

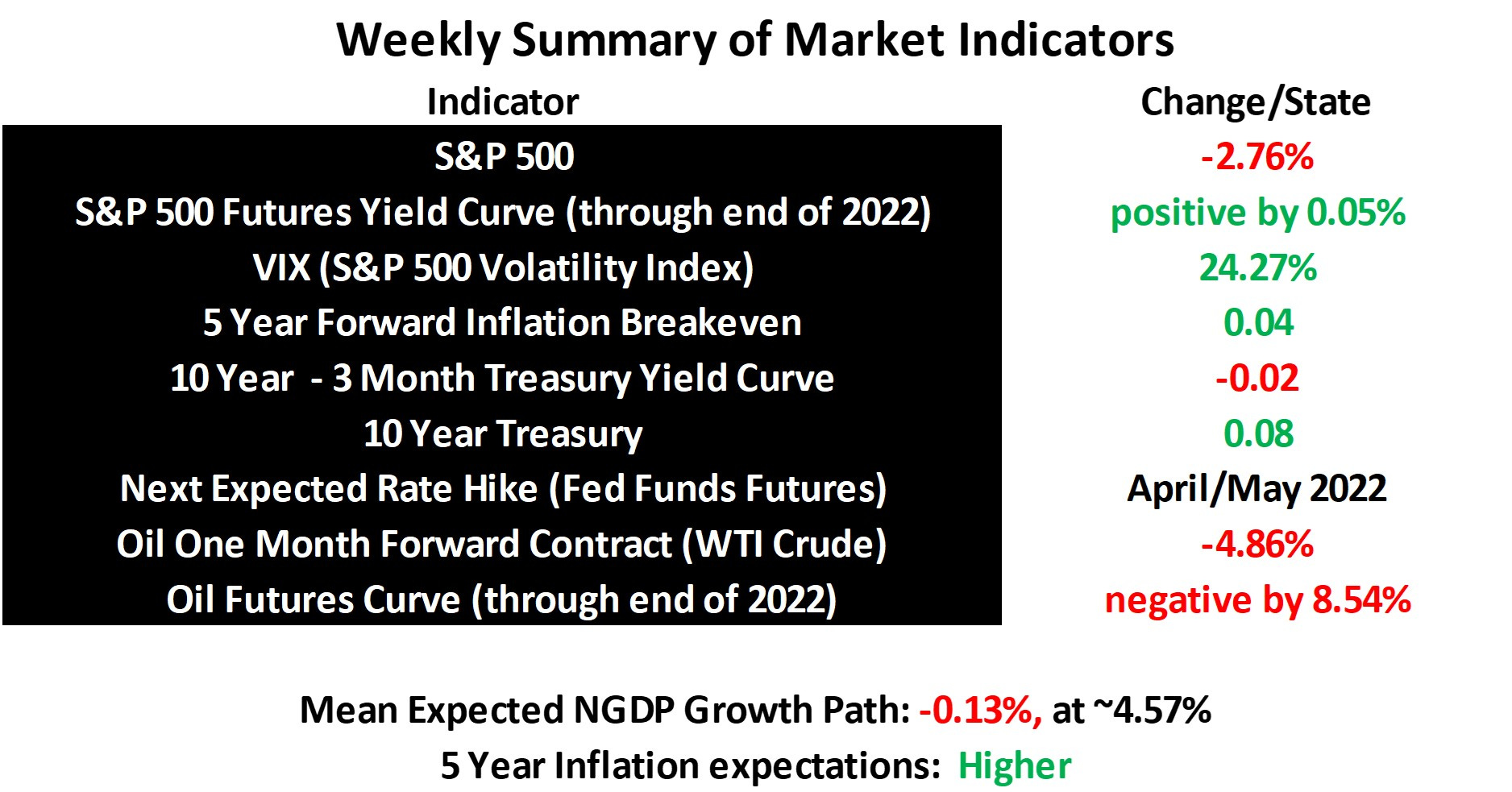

The mean expected NGDP growth path fell closer to 4% last week, finishing at 4.57%, as the S&P 500 had another losing week. The index has another 12.5% to fall before the mean NGDP growth path returns to its pre-pandemic level. Of course, the Fed may want to take it a bit below 4%, to make up for above trend growth-to-date. While the rate of this correction probably feels rapid enough for stock investors, the Fed could nonetheless bring the expected growth path down much more quickly, to help ease consumer concerns about inflation.

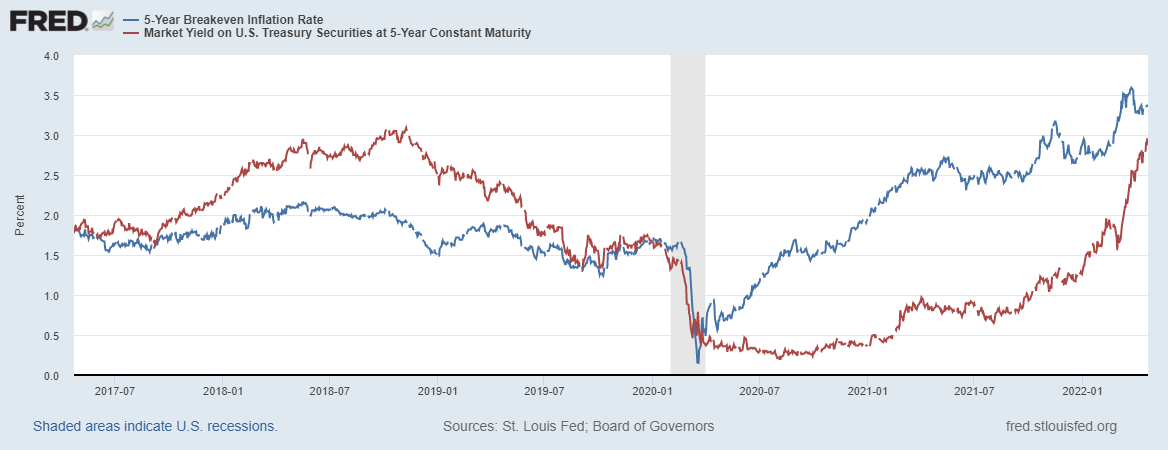

Meanwhile, the 5 year inflation breakeven remains just above 3% in core PCE terms, indicating little progress has been made at lowering inflation expectations, as real growth prospects sink. This is despite the continued spiking of the 5 year Treasury rate. The Fed needs to convince markets it will withdraw the money supply more rapidly.

The odds for recession continue to slowly rise as the NGDP growth continues above trend with the Fed’s further correction for inflation pending. Recession though, at this point, is still not likely.

I remind readers I’d prefer to see a 5% NGDP level target adopted, so that this current cranking down of aggregate demand wouldn’t be necessary. Perhaps one day, some central bank somewhere will have nearly optimal monetary policy.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data