Stock and GDP Outlook, for Week Ending 09/02/2022

Stock and GDP Outlook, for Week Ending 09/02/2022

The Not So Sweet Spot

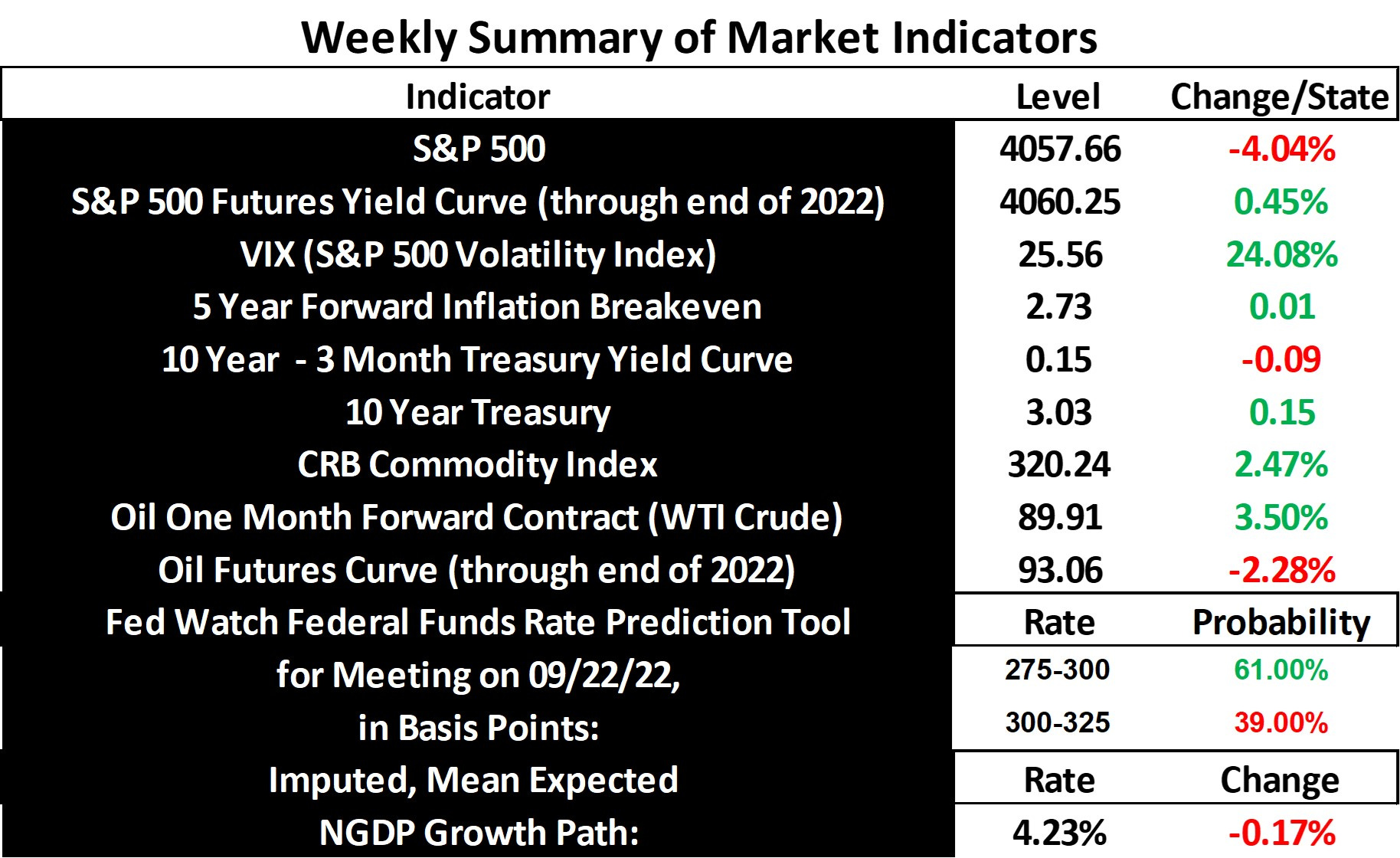

Fed Chairman Powell decided to shake markets out of their complacency last week, with some nominal shocks via comments, particularly at Jackson Hole. Most of the stock market losses for the week occurred Friday, during and after his speech. Hence, there was quite a bit of symmetry between the decline in the mean expected NGDP growth path and the rise in Treasury yields, with inflation expectations essentially unchanged.

Couple these facts with the rise in commodity prices, and there’s a pretty clear case that markets not only expect the Fed to tighten policy, but to do so largely in response to supply-side inflation, which is unfortunate. But, what else is new, in an inflation targeting framework?

This is all contrary to the sense I had, which was based on the sense markets had, that The Fed likely considered the current inflation outlook to be more or less acceptable. I thought the Fed had done a good job, indeed perhaps even too good, at seeing past supply-side inflation and avoiding compounding negative supply shocks with negative demand shocks.

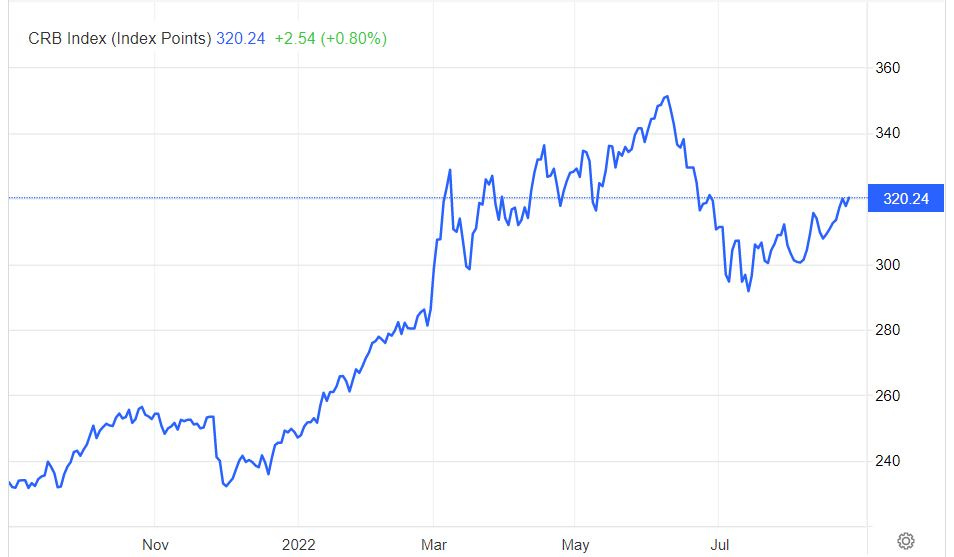

While the S&P 500 has risen steadily for about 5 weeks, commodity prices have also trended upward for the past 4 weeks.

Some of the rise in Commodity prices is likely due to increased aggregate demand, but some of it is also supply-side related, particularly as seen last week, as many stock indexes aroud the world declined in unison.

So, the outlook for stocks and the economy for the rest of the year has darkened rather considerably for the moment. In fact, as I write this, S&P 500 futures are down nearly 1%. Save some positive supply shocks, or some clarification by FOMC members that eases concerns, growth will be on a lower trajectory, at least. And that assumes that there are no further negative supply shocks and compounding demand shocks.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data