Stock and GDP Outlook, for Week Ending 08/19/2022

Stock and GDP Outlook, for Week Ending 08/19/2022

More Real Relief

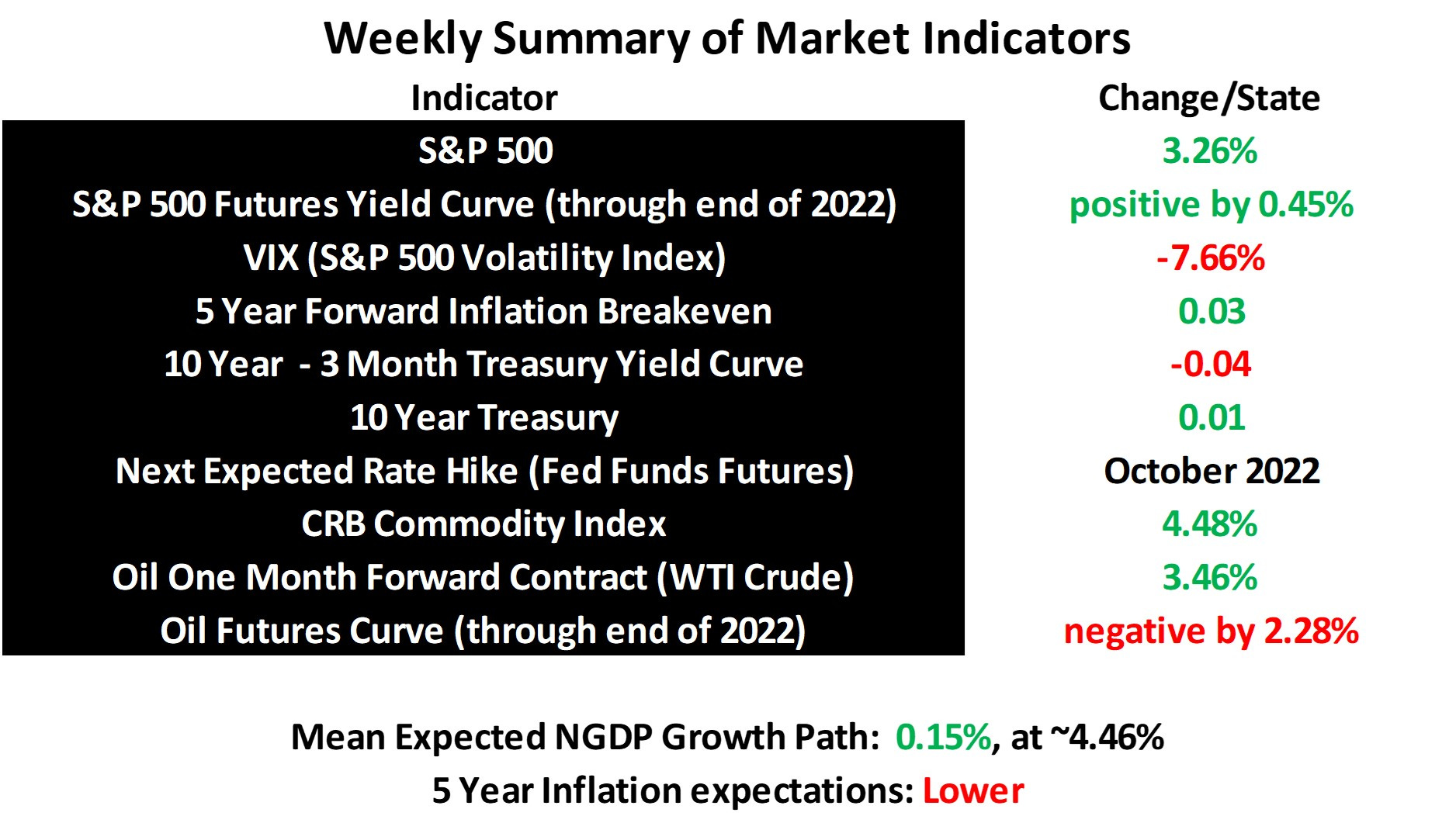

The supply side of the US economy continued to heal last week, with the mean expected NGDP growth path rising rather significantly, while inflation expectations barely budged. This was despite a rise in commodity prices.

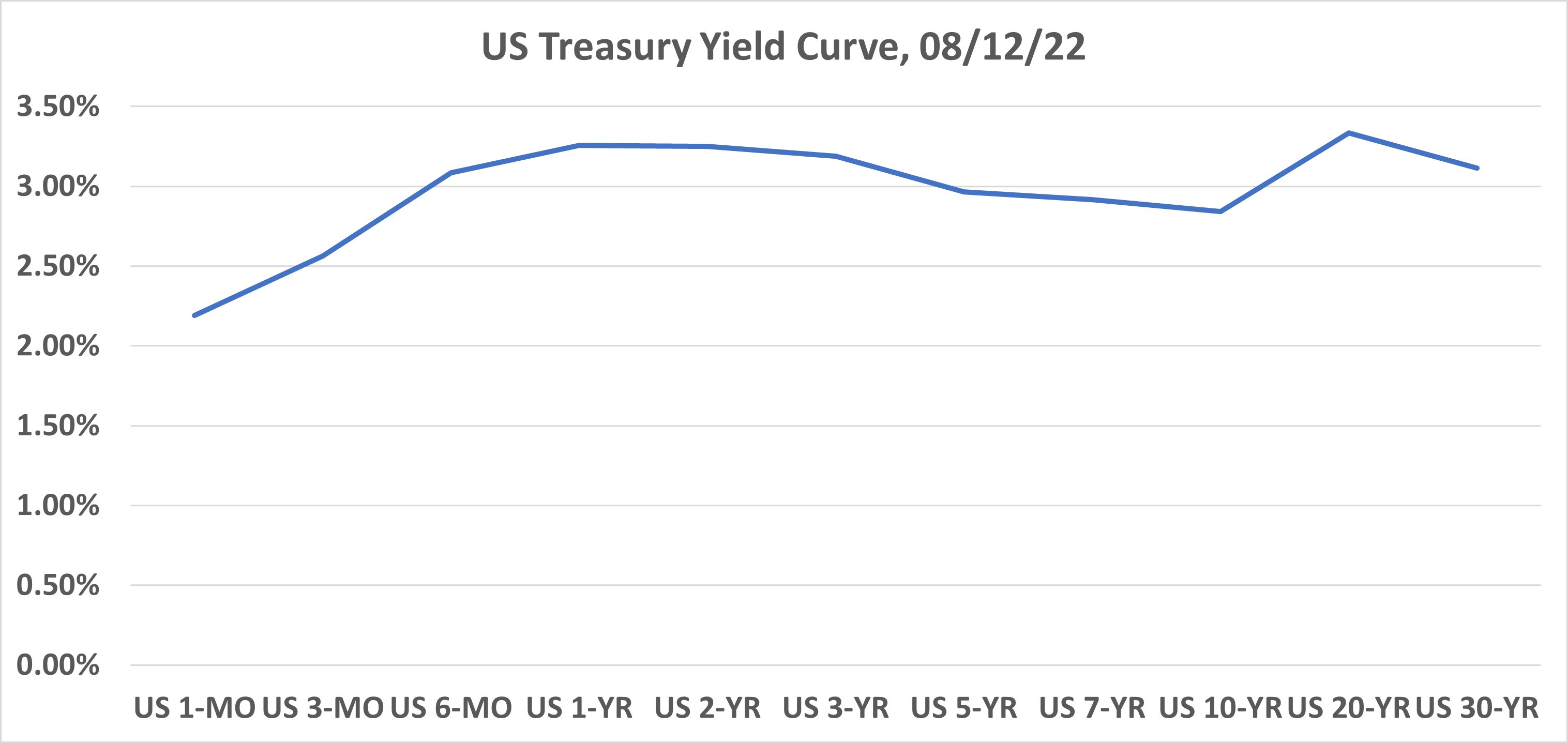

I’ve also noticed that the implied Fed funds rate curve and the Treasury yield curve have been converging lately, with short-term Treasury yields having returned to pre-pandemic highs.

I still think it’s unlikely that the negative yield curves are predicting recession, given how slightly negative they are, and that the 10-year-minus-3-month spread is still a bit positive. As pointed out previously, at worst, a very mild recession might be priced in for next year.

There can always be negative surprises, but as things stand now, the outlook for the US economy and stocks is increasingly positive. I continue to think there is signficantly more upside for the economy and stock prices than commonly recognized. The mean expected NGDP growth path and longer-term interest rates may seem too low to support that view, but the NGDP growth path is seemingly sustainably rising, with more healing potentially to occur.

I wouldn’t be susprised, for example, to see the S&P 500 rise 10% or more by the end of the year, putting the mean expected real GDP growth path well above the actual post-Great Recession mean RGDP growth path. How sustainable such real growth will be remains to be seen, but more familiar readers will know I think we’ve entered an era of technological progress in which productivity gains will more than offset the increasing headwinds an aging, and even shrinking population can present, at least in the US.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data