Stock and GDP Outlook, for Week Ending 05/13/2022

Where is the bottom?

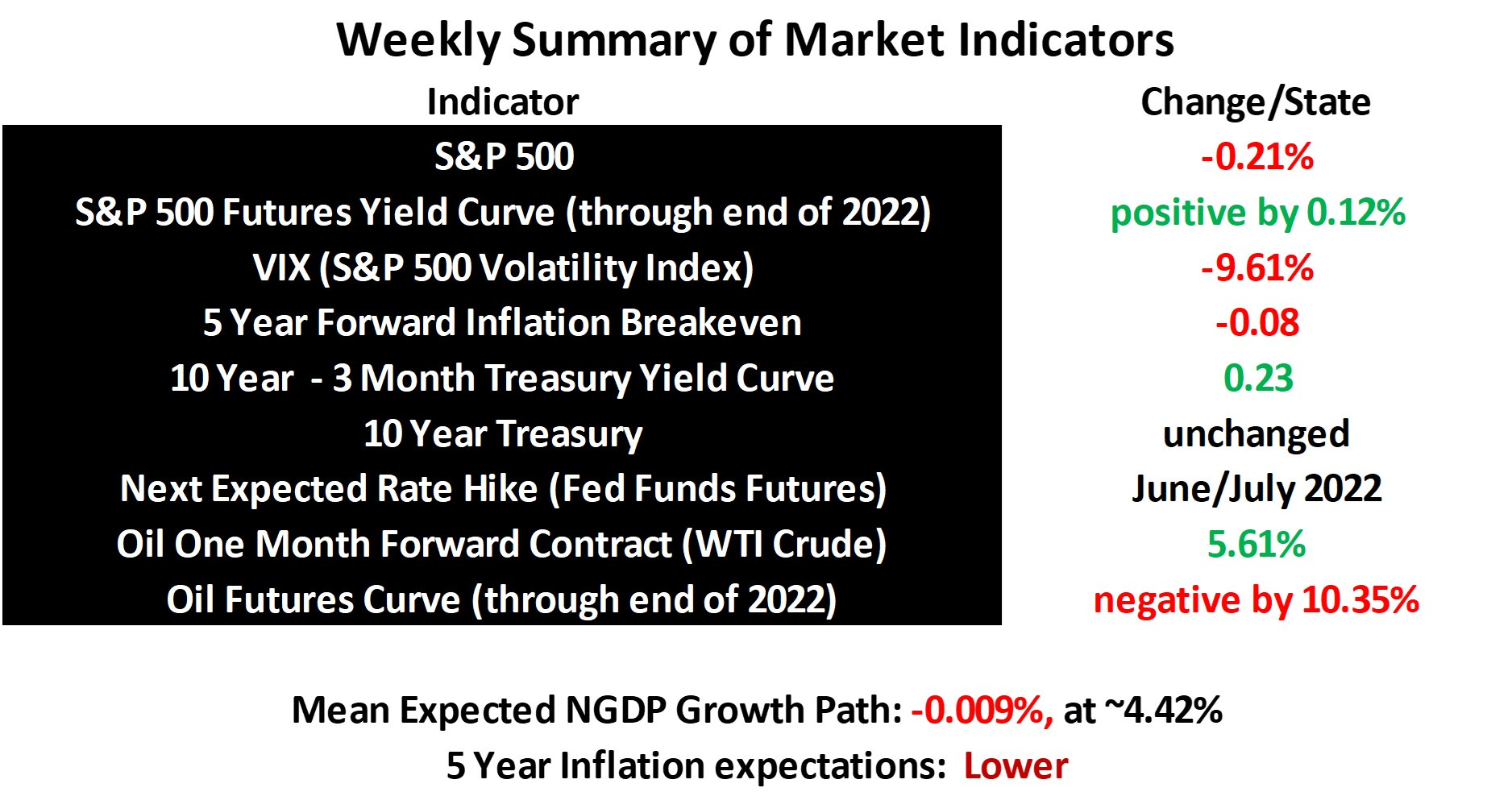

Relatively little changed last week in terms of stock prices and NGDP growth expectations, but the drop in inflation expectations was nontrivial. Hopefully, this is a trend that will continue. Going two months now with unemployment flat and with even the employment-to-population ratio having declined last month, I hope we’re nearing the end of the decline of economic growth to bring down inflation.

Indeed, looking at the S&P 500 over the past several months, and given it’s relationship to NGDP growth expectations, we see that the only significant surges upward in stock prices has been related to surges in inflation expectations, particularly after the invasion of Ukraine began. Hence, real growth expectations have taken a sizable hit.

This is why, though it may be tempting to bet big on the S&P 500 falling at least another 7.5% as the mean expected NGDP growth path retraces down to around 4%, and hence to begin to get inflation expectations closer to 2%, one should think twice. Unexpected good news on the supply side could boost real growth expectations while lowering inflation expectations.

This is one reason why, even under the asymmetric flexible average inflation framework, and even if the Fed treated the inflation target as symmetric, we should not assume that Fed will bring NGDP growth expectations down to 4% or less. Events in the real world will have their say.

Hence, prospects for Covid-related and Ukraine war-related supply-side issues in the future, along with any other supply shocks that may occur, must be considered strongly for all, but buy and hold investors.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data