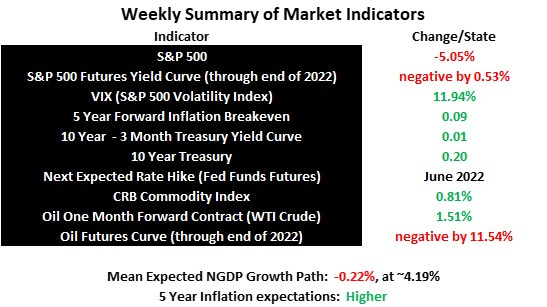

The mean expected NGDP growth path fell back near its low point of the year last week as inflation data surprised on the upside. It is not implausible that the Fed will have to bring the growth path as low as 3.5% to get inflation expectations close to 2%, if that is indeed its goal. That would mean a futher 20% drop in the S&P 500 and could bring a recession.

Since the average inflation target is not symmetric however, the Fed’s goal is not known with any confidence, as I pointed out last week. That said, save some positive supply shocks, there’s every reason to be pessimistic about the near-term outlook for the economy and stocks. This week’s FOMC announcement will be followed more closely than usual.

At least we know we weren’t close to a recession last month, as the May jobs report revealed over 390,000 new jobs. And, for what it’s worth, the Atlanta Fed’s GDPNow has the growth forecast for the current quarter at 0.88%. Hopefully, it will soon prove to be as reliable as it was pre-pandemic, making it easier to combine it with the forward-looking market-based mean NGDP growth path forecast to consider scenarios that might lead to recession with much greater precision.

For now, for long-term investors, this is a perfect illustration of the benefits of dollar cost averaging.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data