Stock and GDP Outlook, for Week Ending 05/20/2022

Improving economy, for commodity producers

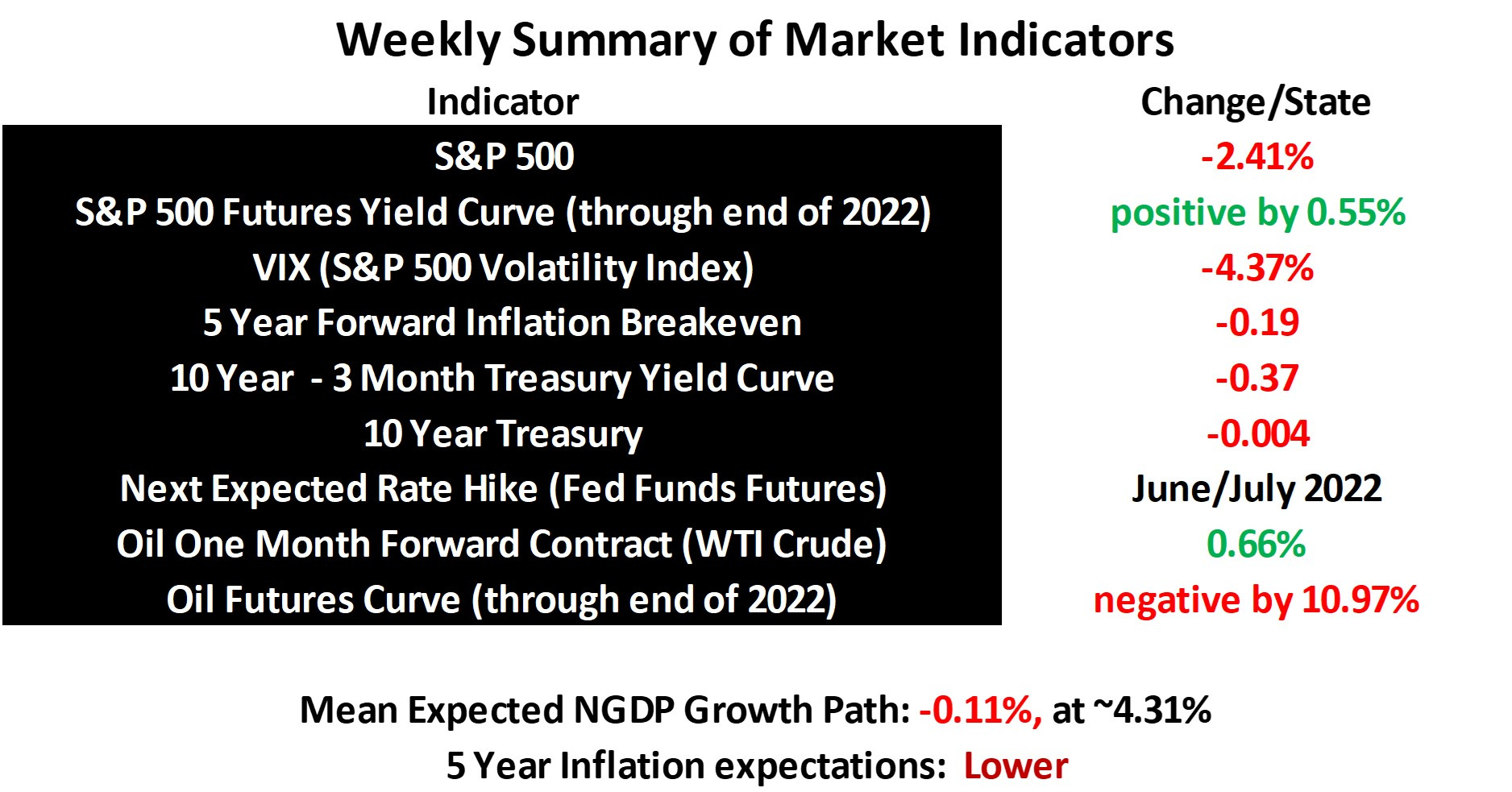

Another week, another drop in stock prices and NGDP growth expecations. Inflation expecations were down even more sharply than those of NGDP growth, and more so than Treasury rates, indicating a rise in RGDP growth expectations amidst all of the red.

So, was it a good week? Probably not. The monetary instability causing market instability is wholly unnecessary. Yes, bringing down inflation expectations is important in adhering to an average inflation target, and a clear monetary policy goal is important for macroeconomic stability. However, as regular readers know, I don’t think average inflation targeting is an optimal policy regime.

The moment we’re in illustrates how ridiculous an average inflation target is, setting aside how ill-defined it is. We’re currently in the midst of serious supply shocks caused by the pandemic, Ukraine invasion, and other factors. That increases inflation, while depressing real GDP. So, the Fed has overshot its 2% average inflation target, and now feels it necessary to lower NGDP to get inflation under control. And, to have any hope of monetary stability, the Fed must be expected adhere to its inflation target in some manner, or at least implicitly set other expectations on which markets can rely.

How much lower should inflation be, optimally? My model indicates that the current expected real GDP growth path is about 1.63%, so with 2% inflation, that would suggest the NGDP growth path should be around 3.63%. But, that’s below the pre-recession trend. That might be fine, particularly if 1.63% real growth is the new normal, but does anyone believe it is? It seems very likely that RGDP growth will rise with relief from the supply shocks. So, even if the Fed merely lowers inflation back down to 2%, leaving the average inflation rate above 2% for this period, it may depress sustainable real growth at some point.

This is why I favor an NGDP level target. This is the same as targeting aggregate demand. This allows inflation to rise and fall opposite real growth. It is the monetary policy approach that helps keep employment and nominal liquid asset prices as stable as possible. It keeps nominal economic growth on a constant trend.

In our current situation, the Fed could, for example, just adopt a 4.5% NGDP level target, boost the economy just a bit, and then just maintain the growth at 4.5%. No need for further tightening and resulting instability, and it would not threaten to cut the legs off of a recovery in real GDP growth that will presumably eventually come.

By the way, for those uninitiated, NGDP level targeting is certainly not an idea original to me. It’s an idea that’s existed for decades, currently championed by economists such as Marcus Nunes, Scott Sumner, and David Beckworth, among others, all of whom write excellently on the subject. Lars Christenson is another excellent so-called “market-monetarist” economist who writes very articulately on the topic, along with fellow travelers such as George Selgin. I borrow heavily from all of these economists, and others.

This is an idea whose time has come, and I hope a model like mine can contribute to the adoption of an NGDP level target. The Fed reviews how it conducts its monetary policy now roughly every 5 years. I hope sympathetic readers will help spread the word about the superiority of such an approach.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data