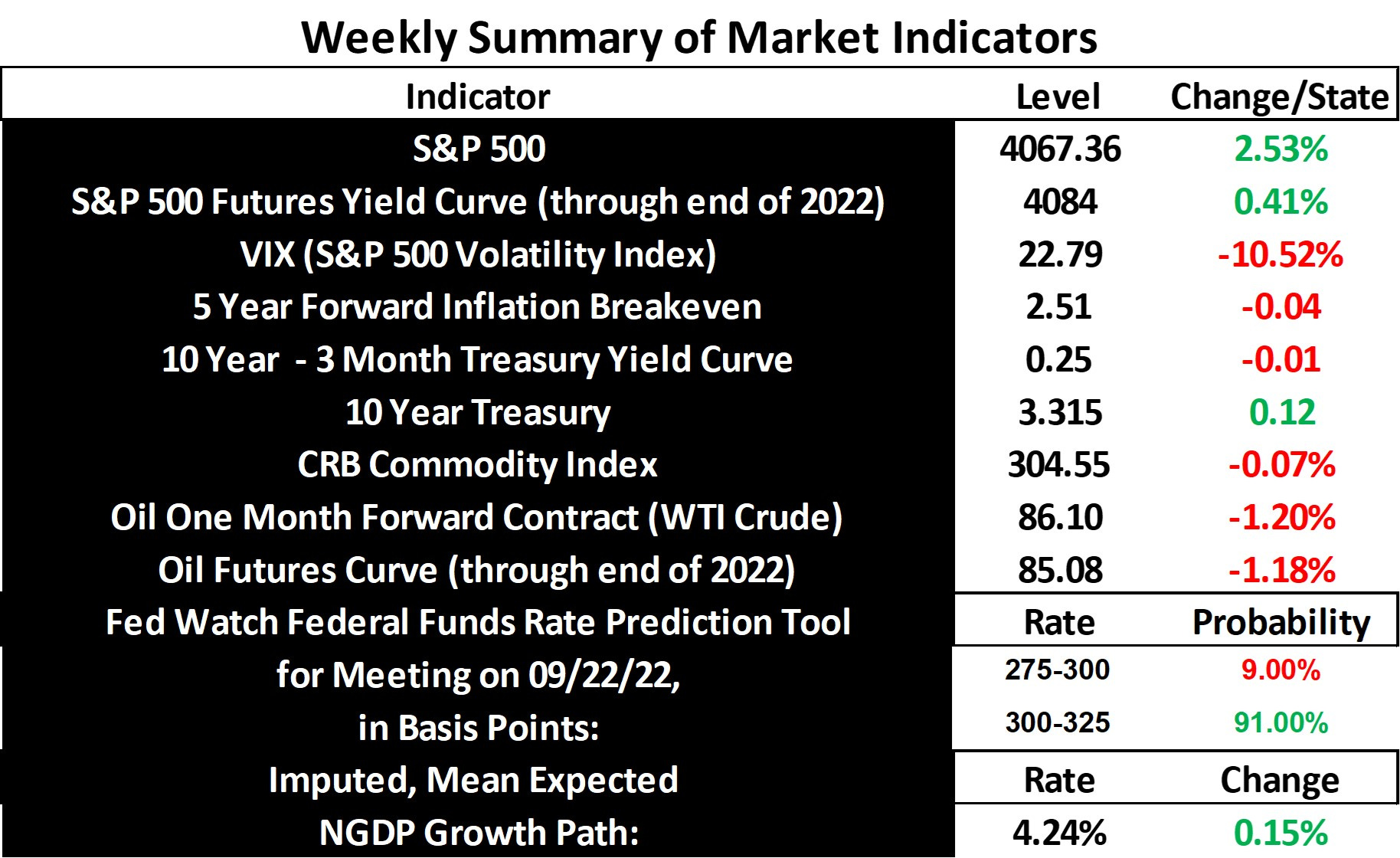

Stock and GDP Outlook, for Week Ending 09/16/2022

Stock and GDP Outlook, for Week Ending 09/16/2022

Not so bad?

Stocks and the mean expected NGDP growth path rebounded last week, as inflation expectations eased. The S&P 500 had fallen more than 9% over the previous 3 weeks, so last week came as a welcomed respite. But, is this just the eye of the storm? Markets don’t seem to think so. Hopefully, the Fed won’t punish them again for their optimism.

Confidence in a lift in the Fed Funds rate to at least 3% this month rose dramatically over the past few weeks, but the Fed Funds futures yield curve is not more negative than before the recent tightening fit.

This, coupled with a still positive 10 year minus 3 month Treasury yield curve suggests that markets still aren’t predicting a recession, or if they are, only a very mild one. The Fed would do well to declare victory and end this tightening cycle now.

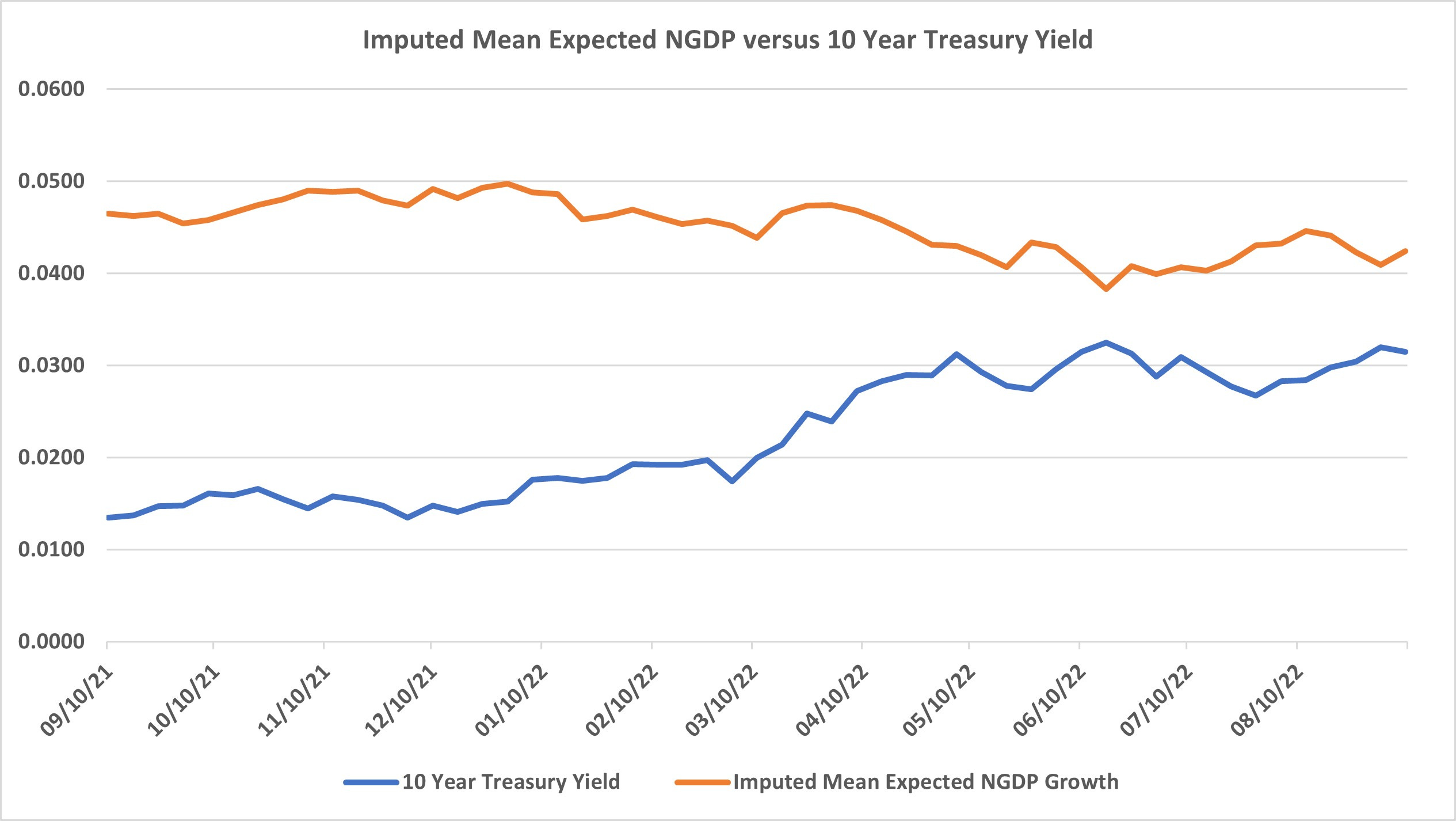

On another subject, I’ve mentioned the symmetry between changes in 10 year Treasury yields and the imputed mean expected NGDP growth path a couple of times during the past few weeks. I thought I’d create a visual.

It’s not just anecdotal, and the R-squared is 0.69, with an extremely unusally low F-statistic and P-value in the simple regression analysis. I’ll be writing more about this in a more formal setting in the future. The data was weekly, but presented as monthly to make the dates more readable.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data