Stock and GDP Outlook, for Week Ending 04/12/2024

Stock and GDP Outlook, for Week Ending 04/12/2024

Danger Ahead? What will cool the economy?

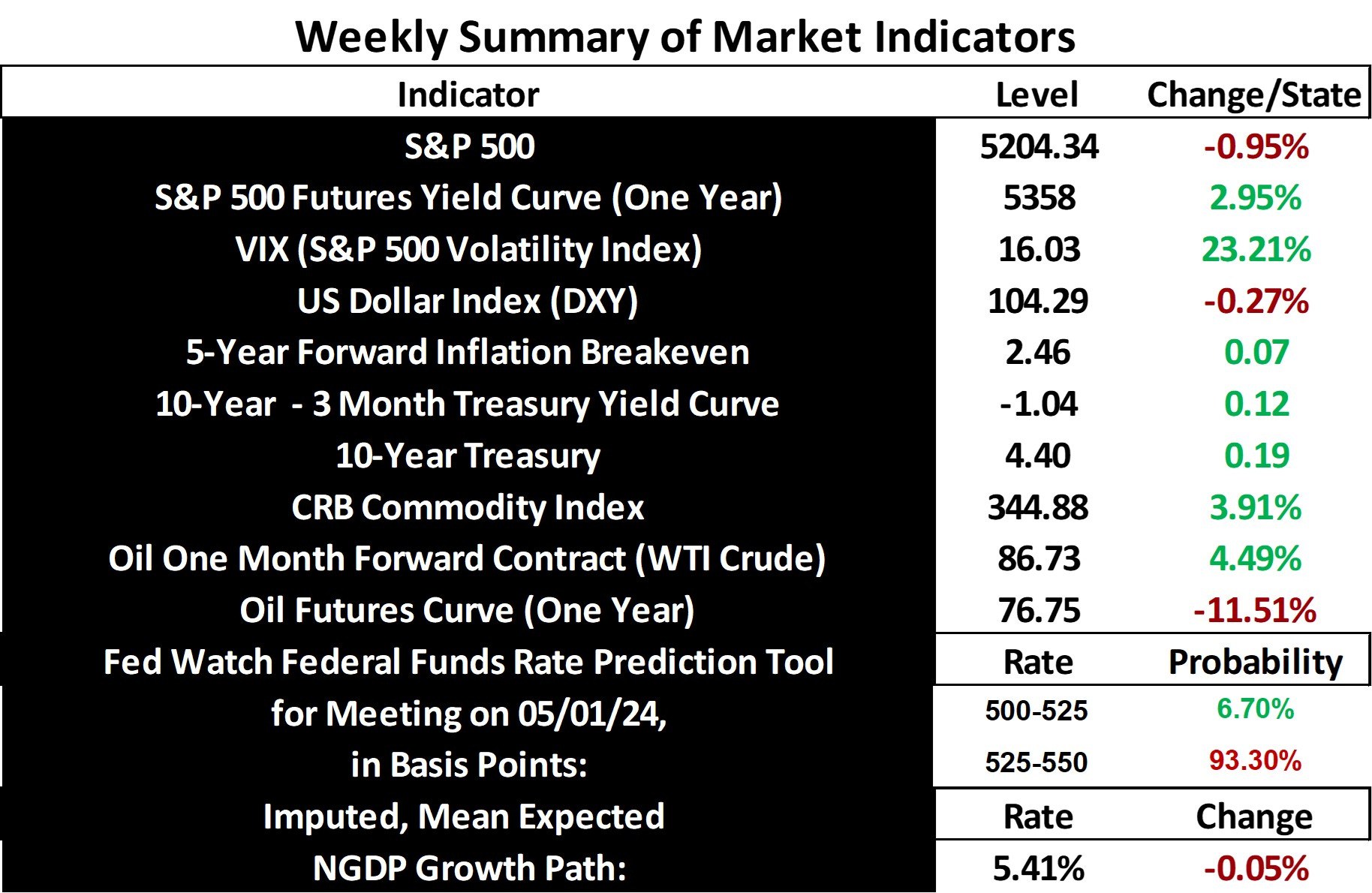

Stock prices and the mean expected NGDP growth rate fell last week, as index volatility spiked, consistent with risks related to rising inflation expectations and commodity prices. The latter is related to oft-mentioned geopolitical disruptions in the Middle East and Russia.

There was also further evidence that the economy continues to run hot, as the jobs report for March was hyper-strong, with more than 303k new jobs created. Also, S&P Global released the S&P 500 index earnings for Q4, resulting in an earnings yield of only 4.01%, versus 5.86% NGDP growth. This represents an increase in the NGDP output gap.

The gap for Q1 is likely close to this value, if not larger, as the projected earnings yield is an even lower 3.88% versus what is projected to be a very similar NGDP growth figure. For example, see the latest Fed GDPNow and inflation nowcast numbers.

Hence, there likely persists a significant positive output gap. We shouldn’t expect to see NGDP growth start to come down much until the Fed Funds rate exceeds the NGDP growth rate. This is because in an economy that is running hot, in absence of government default risk, the neutral nominal interest rate should be at about the level of the NGDP growth rate. The implicit expectation has been that real growth was already on a downward glide path, but now that assumption seems to be in the process of being tested. The real neutral rate must fall sufficiently if NGDP growth is to fall in presence of a positive nominal shock.

That said, markets still expect an economic slowdown and lower nominal interest rates, which seems increasingly puzzling, given the Fed’s recent more expansionary policy. Do markets expect a real GDP slowdown nonetheless, representing a real shock to most of us?

The rising expected earnings yield and the negative yield curve suggest an expected eventual passive tightening of monetary policy, which is hard to imagine, given the recent trend and where we are.

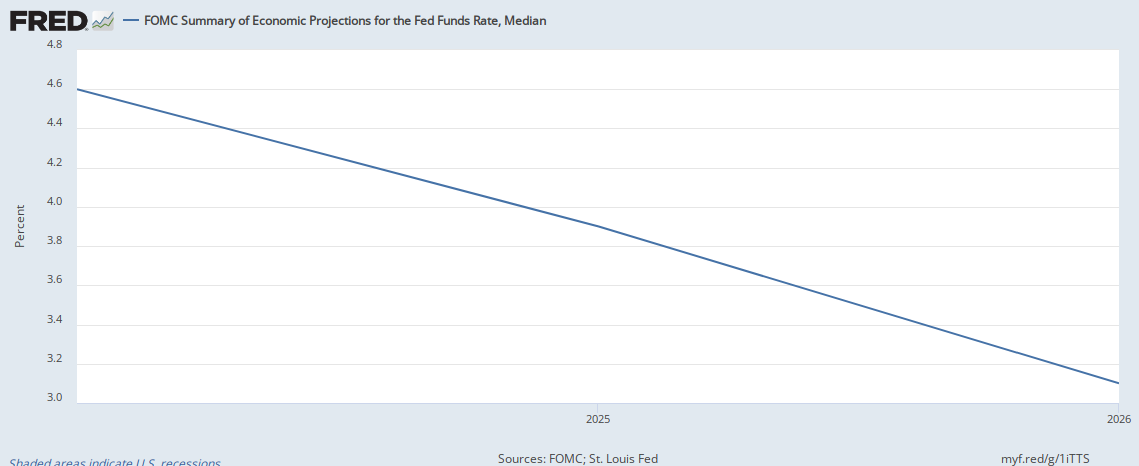

Downward revisions in recent NGDP and jobs numbers wouldn’t help much, given that rising inflation expectations still indicate an economy expected to continue to overheat. Likewise with a lower-than-expected NGDP print for Q1. And the oil futures curve suggests that the recent increase in oil prices isn’t expected to last long, with one year future prices nearly 12% below the current spot price. Also note that it isn’t just markets that expect the Fed to lower rates, beginning this year. The Fed itself projects rate cuts leading to a Fed Funds rate of just 3.1% by 2026.

{kind=link}

So, it is increasingly a mystery as to what will slow down the economy in this context of recent Fed monetary loosening, as expected inflation continues to drift above the Fed’s target. What do markets know that most of the rest of us don’t? My guess is that markets are expecting the Fed to suddenly realize the economy is too hot and to begin to correct. Hence, caution continues to be warranted, though markets still do not predict a recession at this time.

PS: I have an alternative form of this post written in a different style. Please let me know what you think of it, relative to my typical perfunctory approach.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: