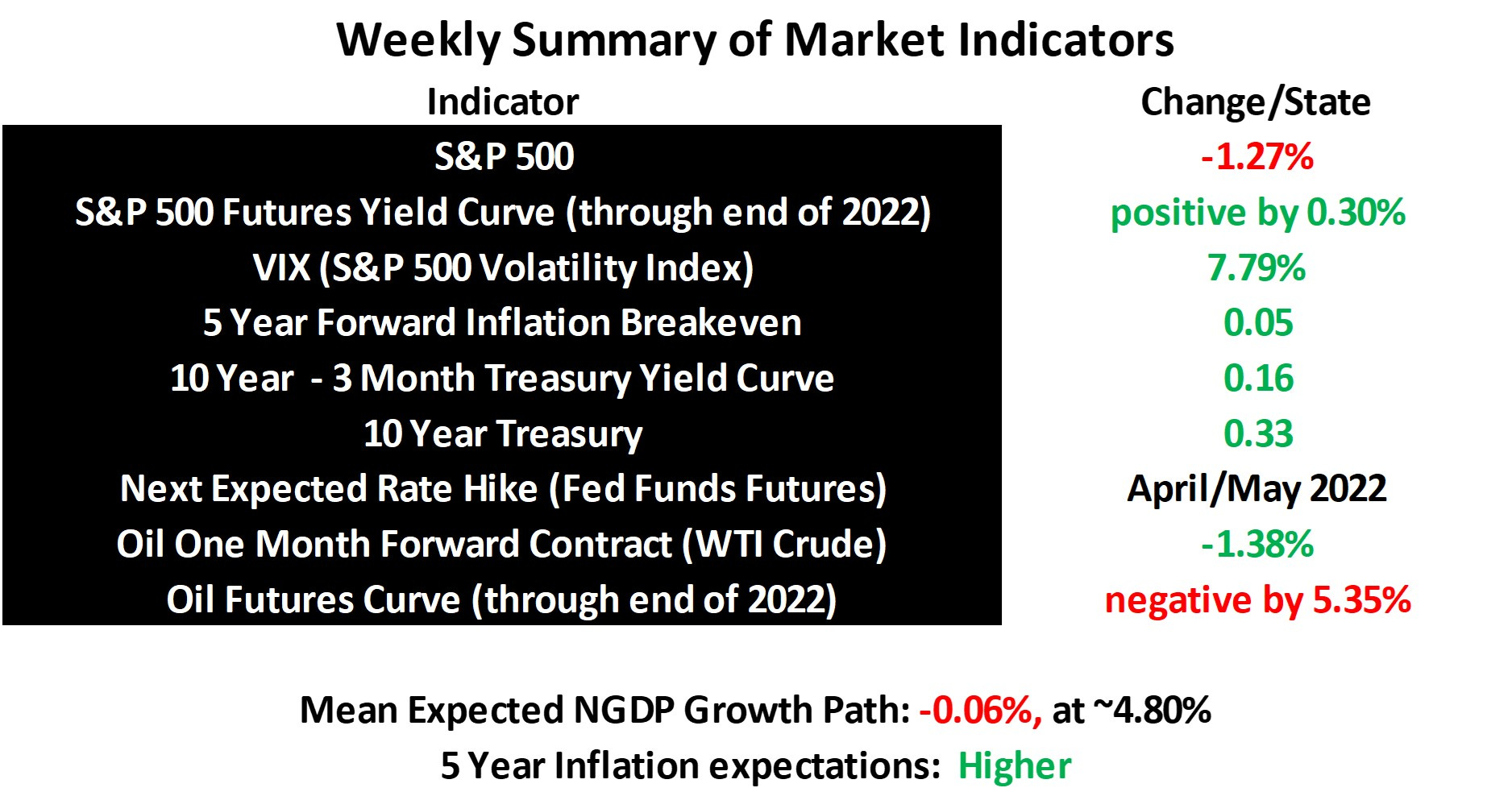

Stock and GDP Outlook, for Week Ending 04/15/2022

Hope in the near future?

Inflation expectations rose slighly last week, despite a signficant increase in Treasury rates. The net effect was that the expected mean NGDP growth path fell slightly, but is still near 5%. It will need to come down closer to 4% for the Fed to seriously reduce recession risks under the flexible inflation targeting regime, given the way it’s conducted policy. As stated previously, this would entail a further loss of nearly 20% in the S&P 500 index.

Adopting a 5% NGDP level targeting regime would save us all the trouble, and I think the S&P 500 could be used to do so, but it seems extraordinarily unlikely the Fed will adopt a new regime soon. That said, nothing prevents them from implicitly level-targeting NGDP.

While the outlook for stocks for the rest of the year seems dreary, there are always possible upside surprises. As I pointed out last week, hope is not a strategy, but it is useful to remember that positive surprises do happen. Possible surprises include, of course, an early end to the war in Ukraine, Covid having an unexpectedly small impact as it becomes endemic, surprisingly high productivity…

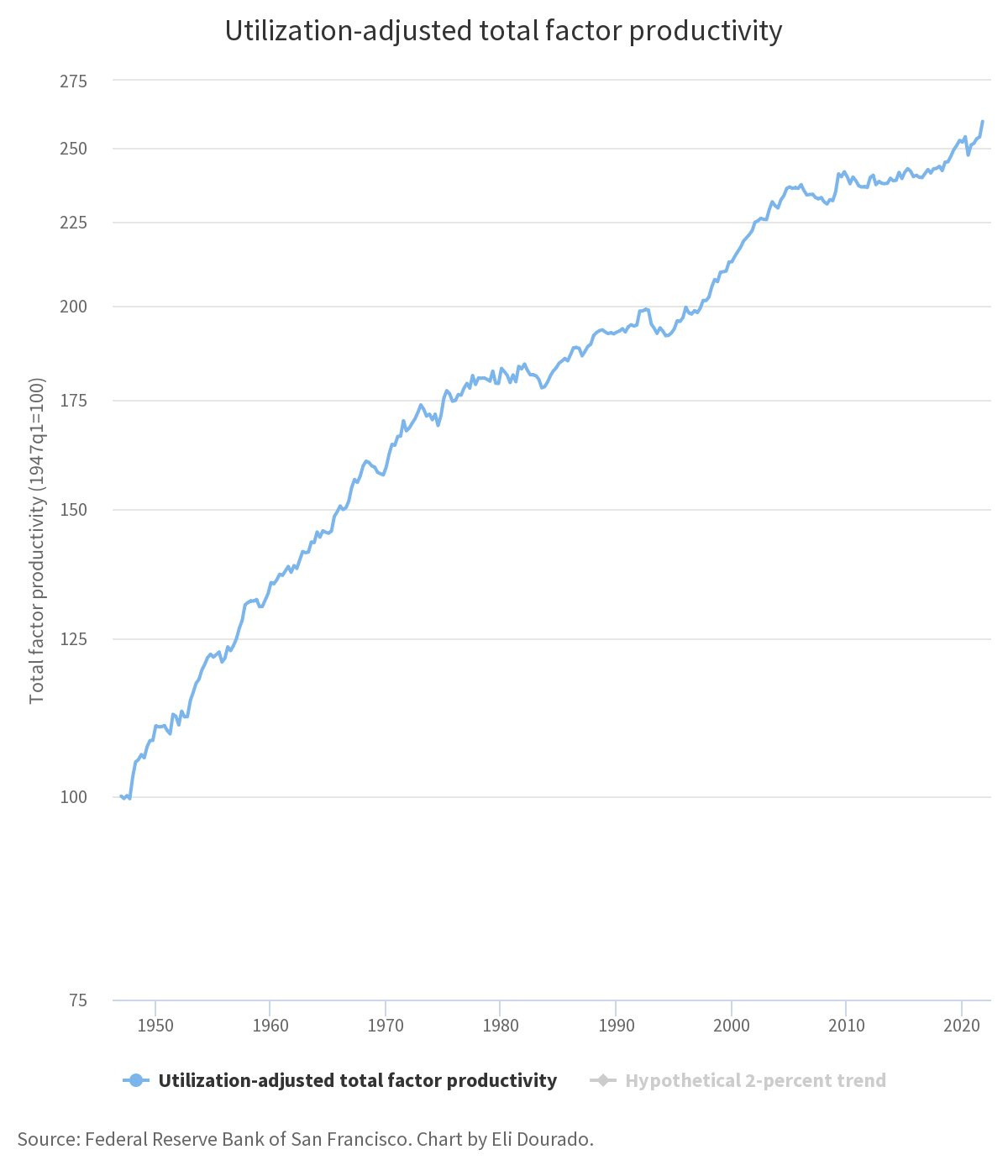

Speaking of high productivity, Matt Yglesias shared this graph showing a big recent pickup in US total factor productivity:

And here is a San Francisco Fed link on the topic. This is supposed to reflect efficiency increases in the economy.

This is great news, if sustainable and not just an artifact. I’ve stated before that I thought there was a good chance productivity would rise sharply as unemployment approached the natural rate, but it’s much, much too early to tell if such optimism was justified. It was much of the basis of my confidence in the S&P 500 reaching well above 5000 when the year began, before the initial tightening, war, and then increased inflation expectations. Of course, it is unknown how much the productive capacity of the economy was hurt by Covid.

As it stands now, I’m happy to be a long-term investor.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data