Stock and GDP Outlook, for Week Ending 06/24/2022

New Lows

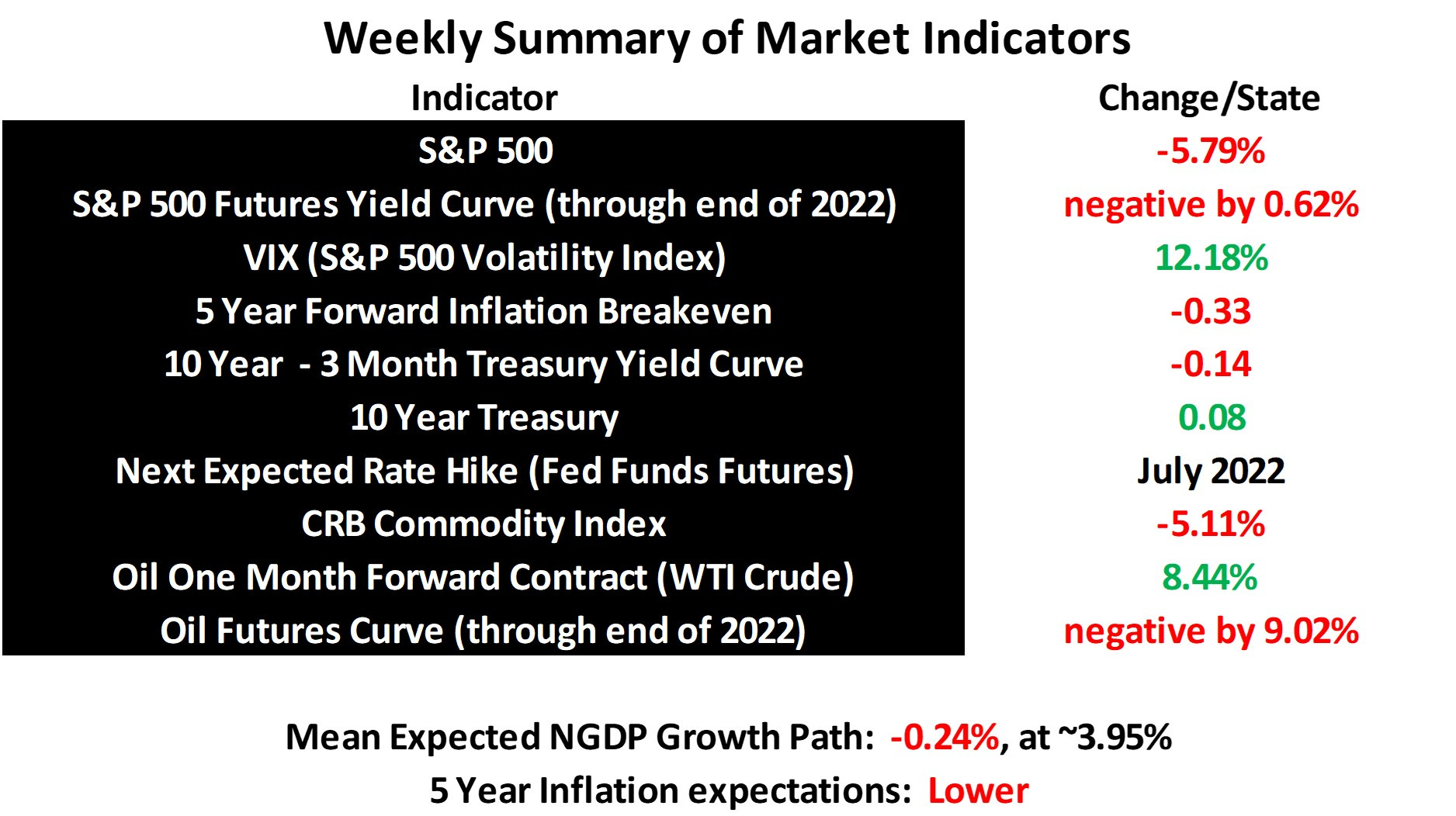

The S&P 500 index reached a new low for the year last week, now having fallen more than 23% from its all time nominal high on January 3rd. More significantly, from the perspective of NGDP growth, the mean expected growth path fell below 4% at market close for the first time since March of 2021.

I obviously can’t claim to know how much further the S&P 500 will fall, but as mentioned last week, if the Fed feels the need to bring the mean expected NGDP growth path all the way down to 3.5% to get inflation expectations closer to 2%, there’s another roughly 13% to go on the downside.

It may seem to some that I’ve been correct about the potential downside since the tightening cycle began on January 3rd, but some will also recall that I was very optimistic about prospects for S&P 500 gains when the year began. It could be years before the index reaches well above 5000, as I thought likely. And being right about how far the index may have to fall to hit an inflation target is just a matter of simple math, though the imputation of NGDP growth expectations in stock price changes helps.

I’ll remind some of you that I was originally optimistic about growth expectations for this year, because I thought there was more real GDP growth potential than seemed commonly recognized. That was based on the notion that there was still likely some catch-up real growth to be had, given that monetary policy was tight in late 2018 and throughout 2019, leading into the pandemic crisis. The only piece of evidence for that claim I want to cite here, other than the reaction of the stock market at the time, is that the Fed brought inflation expectations well-below its explicit 2% target, and even then-current YOY core PCE inflation rates fell below 2%.

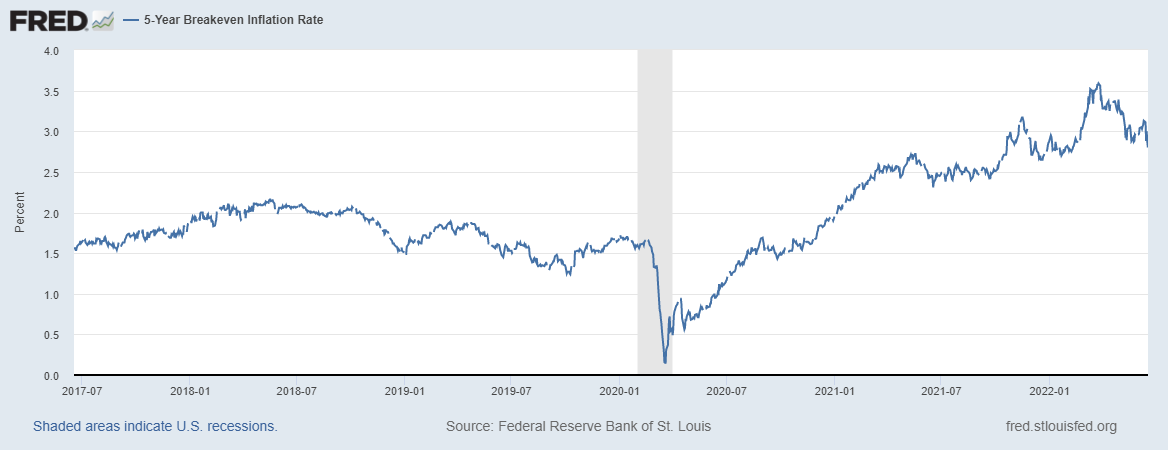

The drop in inflation expectations looks even worse when you subtract the roughly 35 basis points required to translate the CPI in terms of core PCE, the Fed’s preferred measure.

I obviously didn’t anticipate the war in Ukraine, and the severe effects it would have on potential real growth, though it wasn’t an entirely unpredictable event. There was already a Russian military buildup on the Ukraine border in December of last year, for example.

More fundamentally though, I assumed that a combination of additional catch-up real growth and higher than expected productivity growth besides would overcome any permanent scarring caused by the pandemic. Right now, those assumptions aren’t looking good, but it’s still possible that real growth will surprise on the upside once on the other side of these many negative supply shocks.

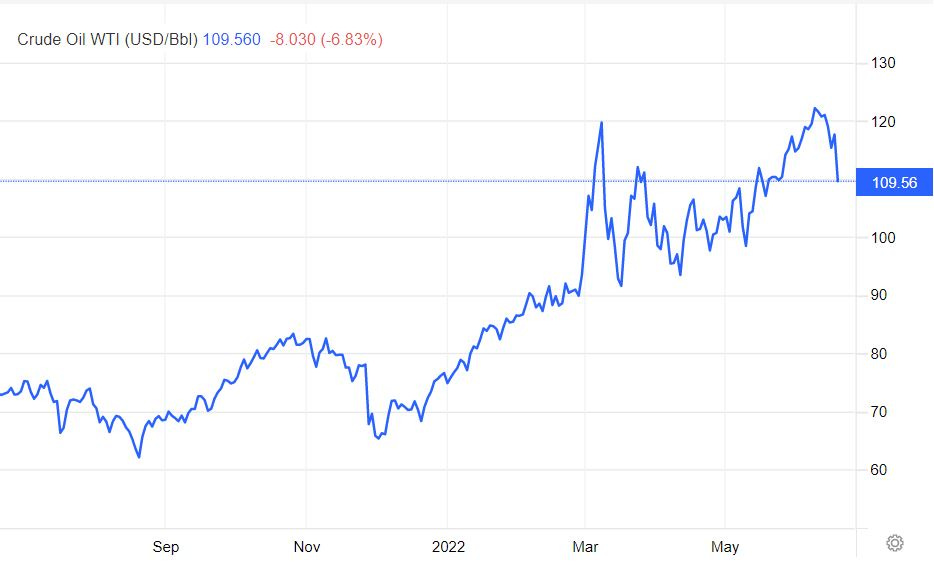

That brings me to something else that’s notable about last week. Inflation expectations finally fell precipitously, along with oil and other commodity prices. The upward march in prices had seemed relentless recently.

WTI Oil and CRB Index data provided by Trading Economics.

Lastly, I’ll address another question I’ve been addressing lately, and that is on recession risk. Negative growth for this quarter, and ultimately a recession, now seems more likely than not, and will probably be mild, but there is a non-trivial risk of a more serious downturn, given the Fed’s vague guidance and the challenge of conducting discretionary monetary policy in an enviroment of highly volatile real GDP growth potential. It seems more likely than not that the Fed will further tighten policy, but that’s obviously just a guess. Their ultimate policy goal and competence in achieivng it, along with any additional supply-side shocks will write this story.

Here’s another in a long, long series of examples of why NGDP level targeting would be a superior monetary policy regime. There’s no need for discretion over policy. Just keep NGDP growing at trend in outer years.

Had the Fed been using changes in stock prices and level targeting NGDP at the previous 10 year average trend, as many good economists would recommend, they would have began tightening policy in March of 2021.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data