Stock and GDP Outlook, for Week Ending 02/23/2024

Stock and GDP Outlook, for Week Ending 02/23/2024

Ceiling for stock prices?

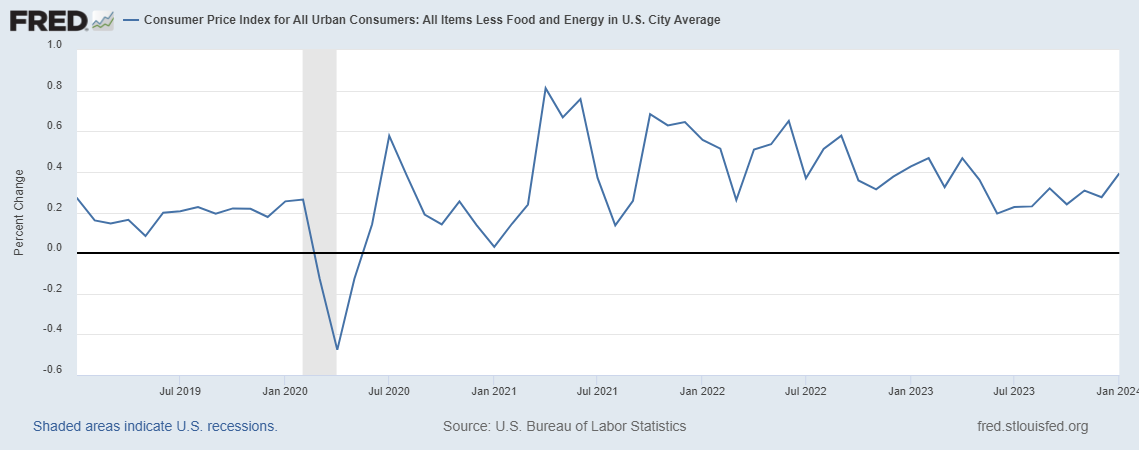

Stocks finally had a losing week, as the S&P 500 and the mean expected NGDP growth rate declined for the first time in over a month. This was mostly due to the report on last month’s CPI coming in at a hotter-than-expected 3.1%, on a 12-month basis. And it continued an upward trend, on a month-over-month basis.

However, year-over-year core CPI continues its downward trend.

The YoY trend notwithstanding, it does seem some limits to further significant stock market gains are emerging, at least for now. The 5-year inflation breakeven ended the week a bit above the Fed’s 2% mean target, in core PCE terms. This could be the end of the recent bull run, save some more positive shocks.

While the economy is still expected to roughly approach equilibrium, there are indications that expectations for unsustainably high NGDP growth are just beginning to show. For example, the gap between the 1-year forward S&P 500 earnings yield, at 4.39%, and the 1-year expected Fed Funds rate, at 4.24%, is slightly positive. Though one shouldn’t make much of such a slight difference, it is at least consistent with the expected inflation rate going slightly above the Fed’s target.

Meanwhile, the expected Fed Funds rate curve beyond 2026 became more steeply positive last week, rising almost 25 basis points for 2029. Apparently, expectations for the recovery after the expected soft landing have gained steam.

Overall, there’s obviously some increased reason for caution going forward. The increased VIX is also a signal in this direction, reminding us of the many risks to the soft landing, beyond Fed policy. The domestic and geopolitical situations continue to become more volatile as election season approaches, and various domestic and foreign actors seek to weigh in on the outcome.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: