Stock and GDP Outlook, for Week Ending 02/18/2022

Yielding Less Optimism

The 10 Year Treasury minus 2 Year Treasury yield spread started getting attention last week, as stocks floundered. That spread is now down to just 42 basis points, from 85 basis points on January 3rd, when this monetary tightening cycle began.

This has many wondering aloud whether the Fed will be able to engineer a soft landing, which should it do so, would be the first time in its history. They could always tighten policy more gradually, if they must tighten.

This is a clearer picture of the Fed’s role:

The most recent downward trend in the yield curve began with the discovery of the Omicron variant in late November. Then, the Fed began issuing relatively hawkish forward guidance on January 3rd, associated with rising interest rates.

Fortunately, the Fed, under the current FOMC, seems to be the best informed, most competent Fed ever. They should be lauded for their relatively brilliant performance during the pandemic recession and its aftermath. There is a better chance that they’ll avoid causing a recession than past Feds, but that chance certainly isn’t 100%.

It is debatable whether the Fed slighly overstimulated the economy. Given that the 5 year breakeven inflation rate never even reached 3% in PCE terms during this recovery, I see no reason for much concern about inflation from a monetary policy perspective. The relatively high current inflation rate is due to shortages and demand surges related to the pandemic, rather than monetary policy, hence the implicit market expectation that the inflation is indeed “transitory”.

Yes, as I’ve stated a few times in previous weeks, the Fed has said it is using a 2% flexible average inflation targeting(FAIT) regime, but has not specified over what time frame. and has also acknowledged its dual mandate, which includes full employment, in addition to price stability. Hence, the Fed has given itself the flexibility to run the economy a little hot to try to get people back to work as quickly as possible as supply-side disruptions subside.

So the outlook for stocks and the economy for the week ahead, and indeed, for the remainder of the recovery is now considerably less certain than when the year began. There’s always the potential for positive real GDP shocks, especially if the Omicron variant is in fact the final challenge from Covid-19 as the US and much of the rest of the world reaches herd immunity. Forutunately, there is not much of a dilemma here for buy and hold investors.

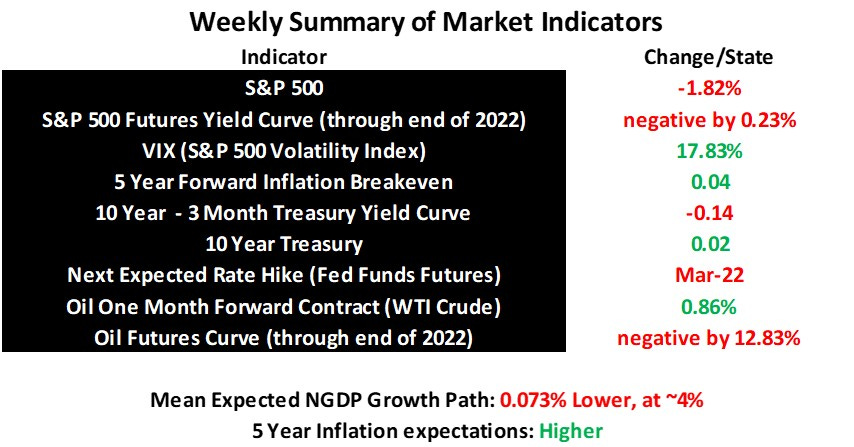

Just for those interested, here’s a breakdown of changes in key indicators since January 3rd:

S&P 500: -7.88%

Mean expected NGDP growth path: ~ -.031%

10 year Treasury Yield: +0.32

5 year inflation breakeven: -.13

10 Year Treasury Yield minus Two Year Treasury Yield: -.43

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data