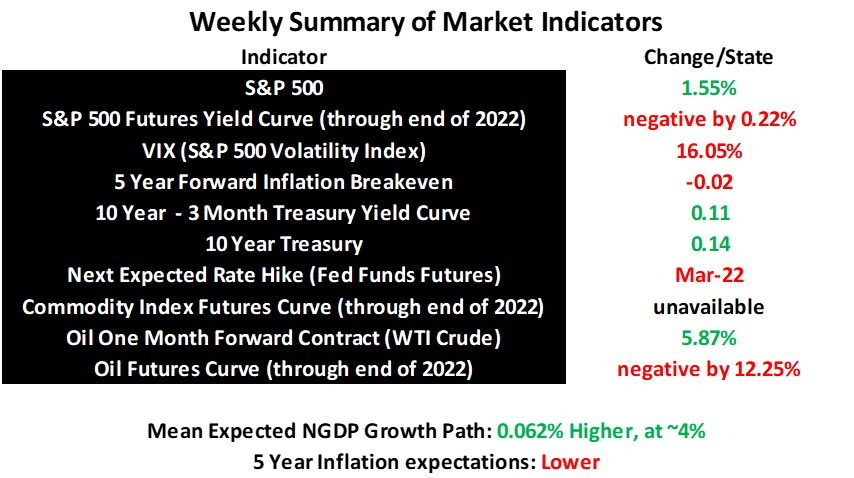

Real GDP growth expectations rose last week, as the S&P 500 finished with second consecutive weekly gain. Given the Fed’s expressed lower tolerance for inflation, we’ll likely have to depend on gains in real GDP expectations for stocks to outperform going forward. At this point, we may be lucky to see 5000 reached by the S&P 500 by year’s end, well short of my previously expected 5300-to-5800 range.

This is perhaps not as bad as I would have thought for the economy as, at least for the moment, it appears that the mean expected real GDP growth path is close to potential, given that long-term Treasury yields have been rising as inflation expectations fall. If markets thought the Fed was overdoing the tightening, presumably long rates would fall. It may be that long-run US real GDP growth potential is lower than I imagined. There is still the possibility of surprises though, particularly if nearer term real GDP growth potential can increase sharply.

In the meantime, I hope for more positive real surprises, with those still unemployed getting back into the workforce very soon.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data

https://www.marketwatch.com/investing/future/sp%20500%20futures

https://www.cmegroup.com/trading/agricultural/commodity-index/bloomberg-commodity-index.html

https://www.cmegroup.com/markets/interest-rates/stirs/30-day-federal-fund.quotes.html

https://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_quotes_globex.html