Stock and GDP Outlook, for Week Ending 09/30/2022

Stock and GDP Outlook, for Week Ending 09/30/2022

Aggregate Misery

The Fed continued its lashing of the economy last week, as the S&P 500 fell nearly 5%, as the mean expected NGDP growth rate continued to fall below its pre-pandemic rate. The Fed is treating inflation like a suspected burglar in the dead of night, thrashing blindly with a baseball bat, long after the intruder has fled. There is the risk they could do more damage now than the high inflation itself would have done. Jeremey Siegel made the point last week better than I have.

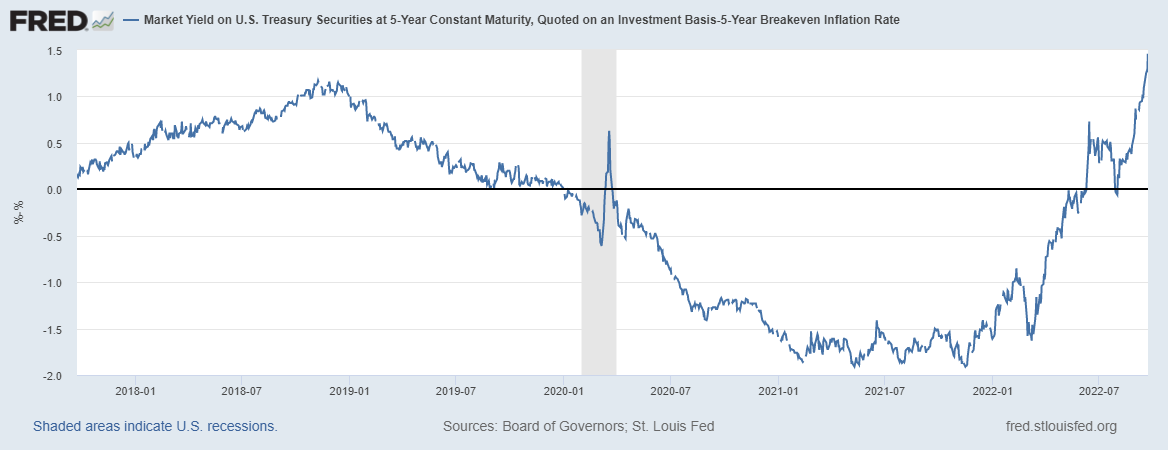

Here’s a look at real interest rates, or in this case, expected real rates, which Siegel correctly points out are now quite positive.

The Fed seems allergic to principles of good monetary policy, such as clearly defining their objectives and the regime to achieve them, and using reliable forward-looking metrics. Oh, and their regime is suboptimal. Other than that, they’re doing a fabulous job.

I hate to be so critical, as the Fed did an unusually good job at keeping aggregate demand growth expectations near trend during the pandemic. However, we need a monetary policy of rules, not of men and women. A rule, such as NGDP level targeting, perhaps using the S&P 500 to impute the expected NGDP growth path, would allow the Fed to avoid embarrassing situations such as inverted yield curves while they’re hiking rates. Do they ever see the irony?

While recession still seems unlikely, the risk is obviously growing for at least a mild one, and it is, of course, completely unnecessary. It’s tempting to continue to say that the stock market and economic outlook are near bottom, but the Fed is starting to hint that it might be less competent than assumed. If this trend continues, look out(!), particularly if coupled with a negative supply shock.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: