Stock and GDP Outlook, for Week Ending 06/10/2022

Precisely Vague

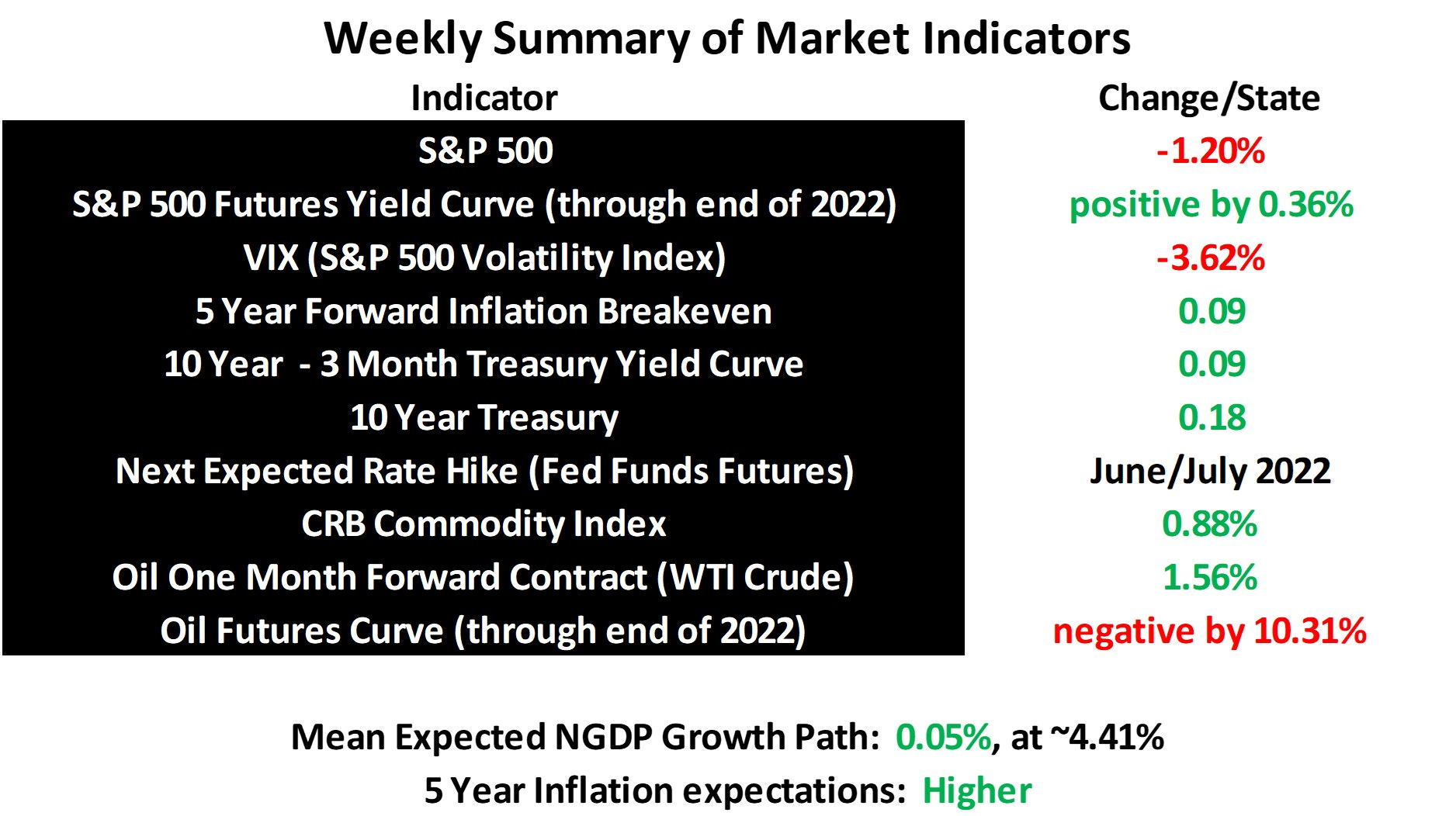

Climbing commodity prices continued to undermine growth expectations again last week, after the big bounce in stocks the week before. As it stands, it could hardly be more difficult to guess where growth expectations, and hence the stock market, will go from here. Even the unpredictability of possible positive or negative supply shocks aside, what is the Fed’s ultimate goal, quantitatively? They don’t seem to want us to know.

They have a flexible inflation target that takes unemployment into account. Chairman Powell says that periods of above 2% inflation do not necessarily mean there need to be later periods of inflation below 2%, so there must be asymmetry in the target. But, how much, and under precisely what circumstances? I’m guessing the zero lower bound for interest rates is a factor, in addition to employment data, I shouldn’t have to guess.

If the Fed wants to get inflation back down to 2% anytime soon, ceteris paribus, expected NGDP growth will have to be brought down further. That obviously means more pain for most stock investors. That would likely mean bringing the mean expected growth path down into the 3.5-to-4.0% range, which would represent a further decline in the S&P 500 of anywhere from about 10%-to-26%.

That raises the question: If the forward inflation expectations are above the Fed’s desired rates, why are they waiting to further tighten policy? Are they waiting to see if supply-side factors will do much of the job for them? Do they still rely too much on internal forecasts, as they did during their previous inflation targeting regime?

If they’d just level target the S&P 500 at roughly the current expected NGDP growth rate, monetary policy would be just fine. Expectations would be precise and firm, and results verifiable. There would be no concern about losing the inflation anchor. Instead, we have confusion.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data