Stock and GDP Outlook, for Week Ending 03/15/2024

Stock and GDP Outlook, for Week Ending 03/15/2024

Growing Caution

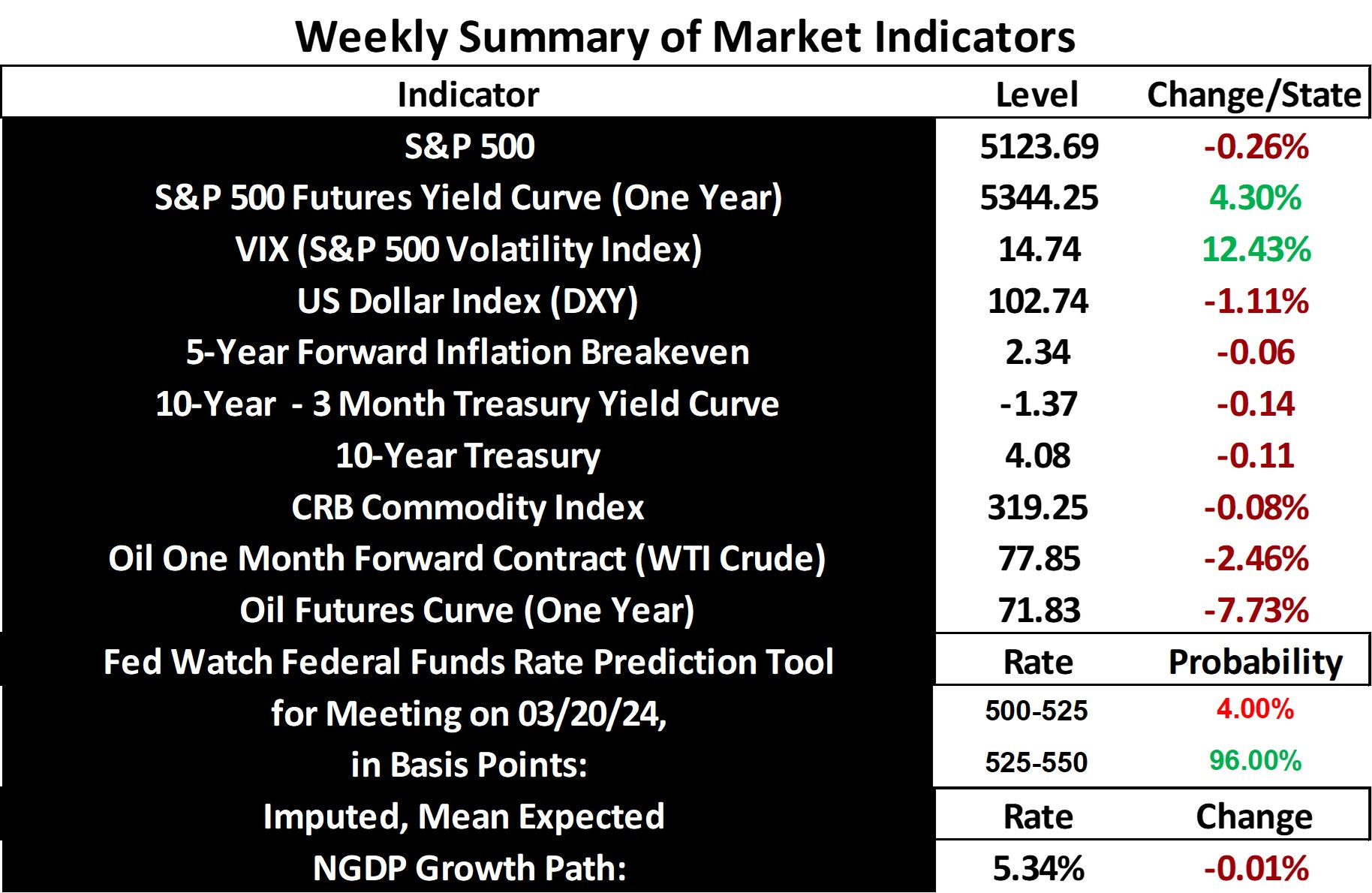

Stock prices and the mean expected NGDP growth rate declined last week, representing a rare recent retreat, as the VIX rose. We should continue to expect more such weeks, as I’ve been indicating since the first half of last month, save some additional positive news for real growth. While 5-year expected inflation fell a bit, it is still running up against the Fed’s 2% mean target in core PCE terms.

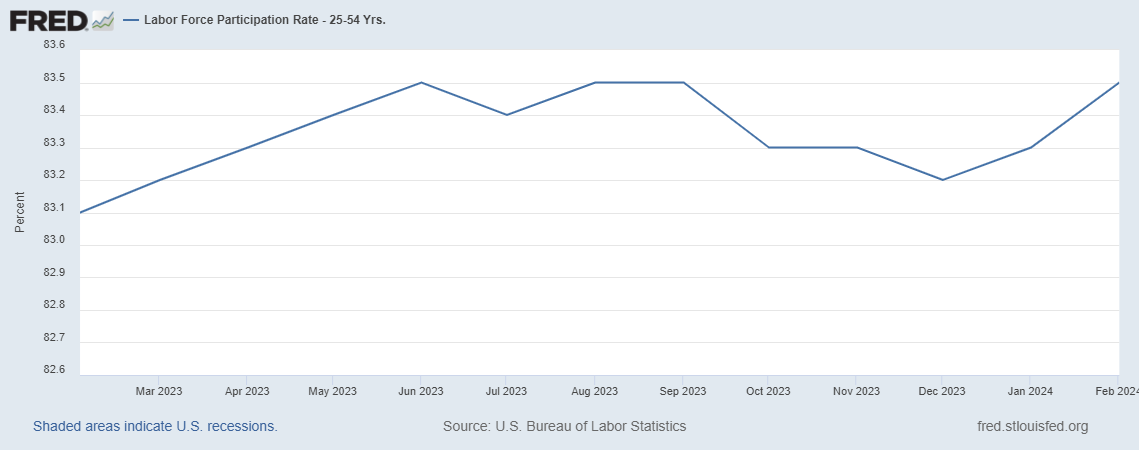

This represents a net negative nominal shock, after a very strong February jobs report that also saw the unemployment rate rise to 3.9%. This change in unemployment is consistent with an increase of the prime age labor force participation rate, indicating no current slowdown in an economy that is still running somewhat hot. The Fed’s GDPNow is currently at a bit over 2.5%, which is pretty high in the context of typical Q1s. I would not be surprised to see NGDP growth exceeding 5.5% for the quarter.

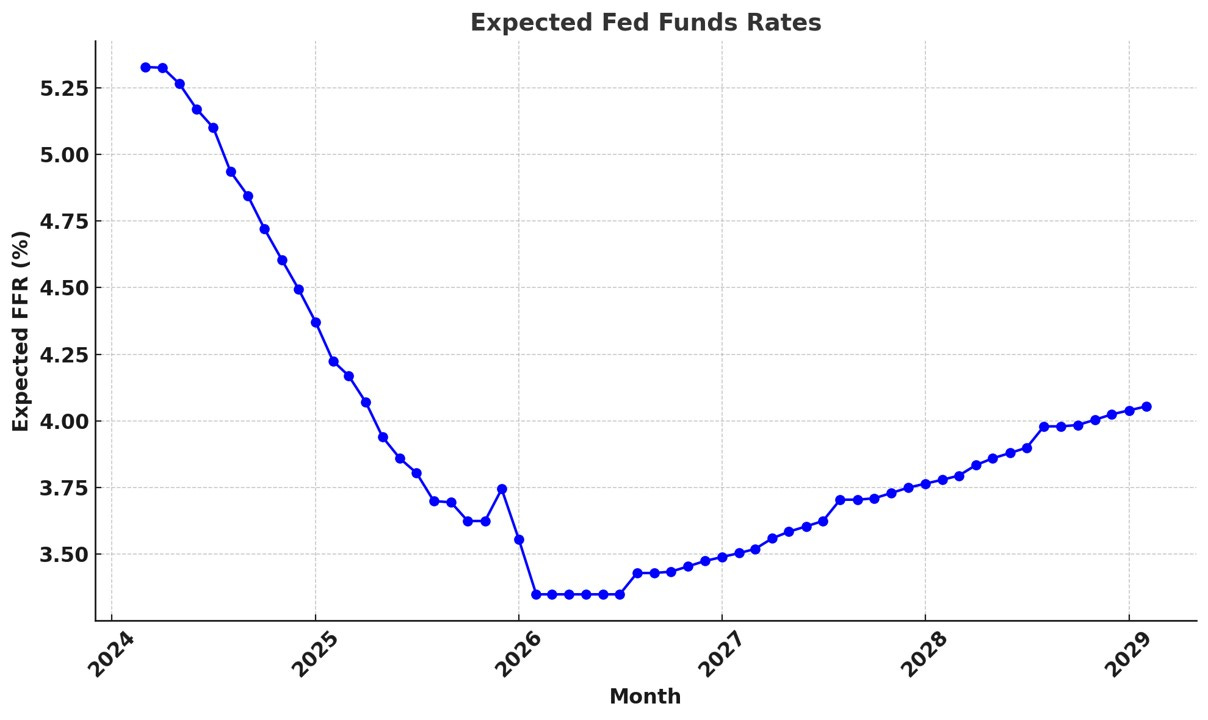

The current state of the economy is secondary to the expected state of the economy however, and it is still expected to be close to equilibrium within the next few years or so. It is not a coincidence, for example, that the current and various measures of forward S&P 500 earnings yields, and the one-year forward expected change in the S&P 500 price have been converging for months. They are all well within about 0.50%. The two-year Treasury yield, at 4.8% is likewise close to this range, suggesting that not many adjustments versus expectations are required to keep growth relatively healthy for the foreseeable future. This is also consistent with the view from the Fed Funds futures market, which still has rates bottoming out within about 2 years.

So, we’re still looking at a slowdown soon, but nothing like a recession in the foreseeable future, at least as market expectations currently stand.

There could certainly be more positive shocks in the near future, but given the seemingly unlikely string of such shocks over the past couple of years, amidst increasing political and geopolitical risks, it seems we are testing our luck. There is still some post-Covid healing to expect, but expect is the key word here. Positive shocks in this trailing recovery seem increasingly unlikely, and will obviously be of diminishing magnitude as supply chains stabilize. More surprises in AI development and immigration rates are still wild cards here, but it’s important not to overlook the possibiity for near-term disappointments in these areas as well.

It’s nearly always a good time for long-term investors to buy US stocks, but for the rest, some caution is increasingly in order.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: