Stock and GDP Outlook, for Week Ending 12/15/2023

How much more healing?

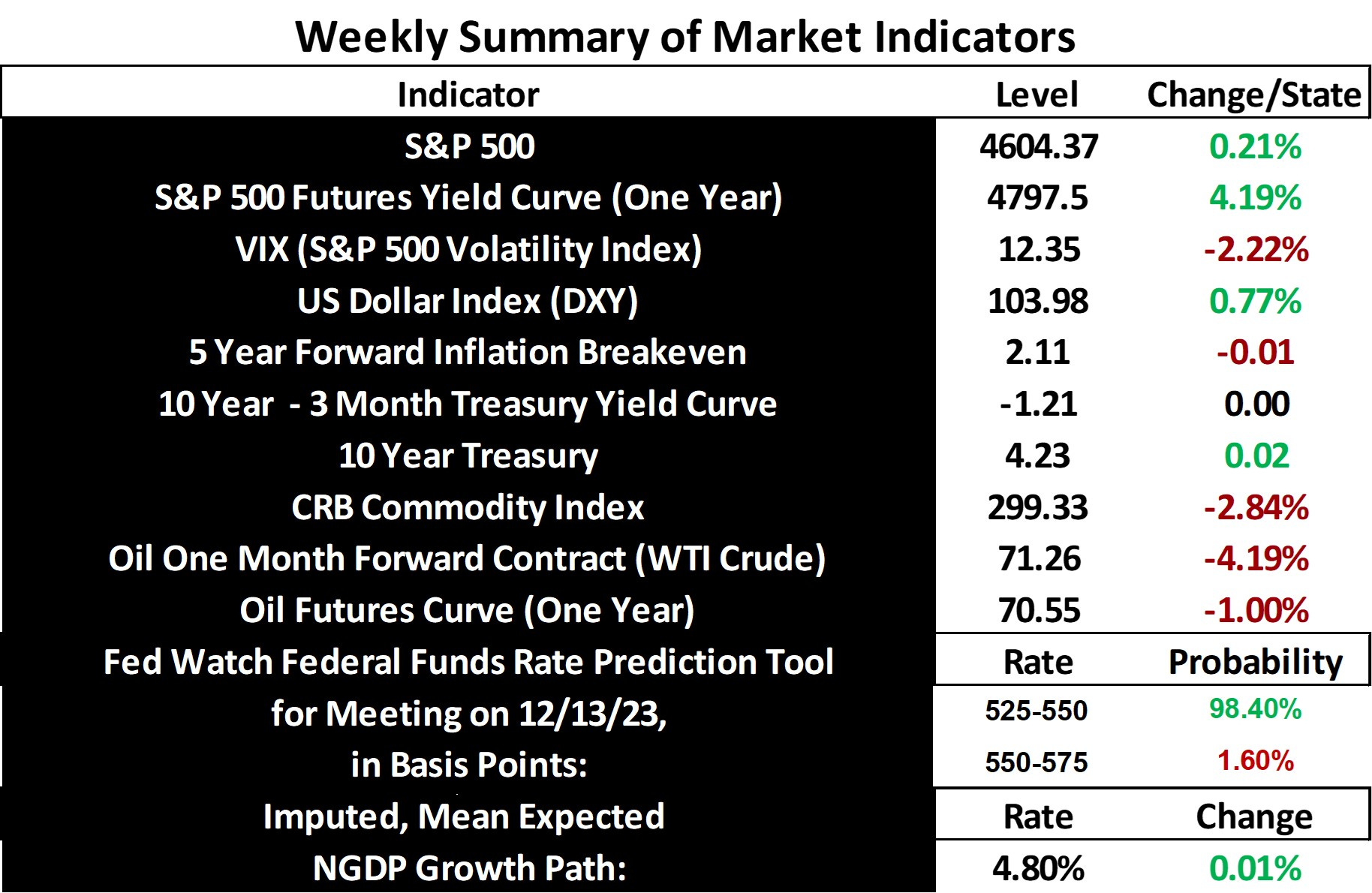

Rinse and repeat. For the 6th straight week, the S&P 500 and the mean expected NGDP growth rate closed higher, with stock price volatility and inflation expectations easing further. Commodity prices also eased, and are now back down to the range last seen in mid-July.

More good news for the real economy included an unexpectedly strong jobs report, returning unemployment down to 3.7%. So, the evidence indicates that the economy continues down a path toward, what for the US, is an unprecedented soft landing.

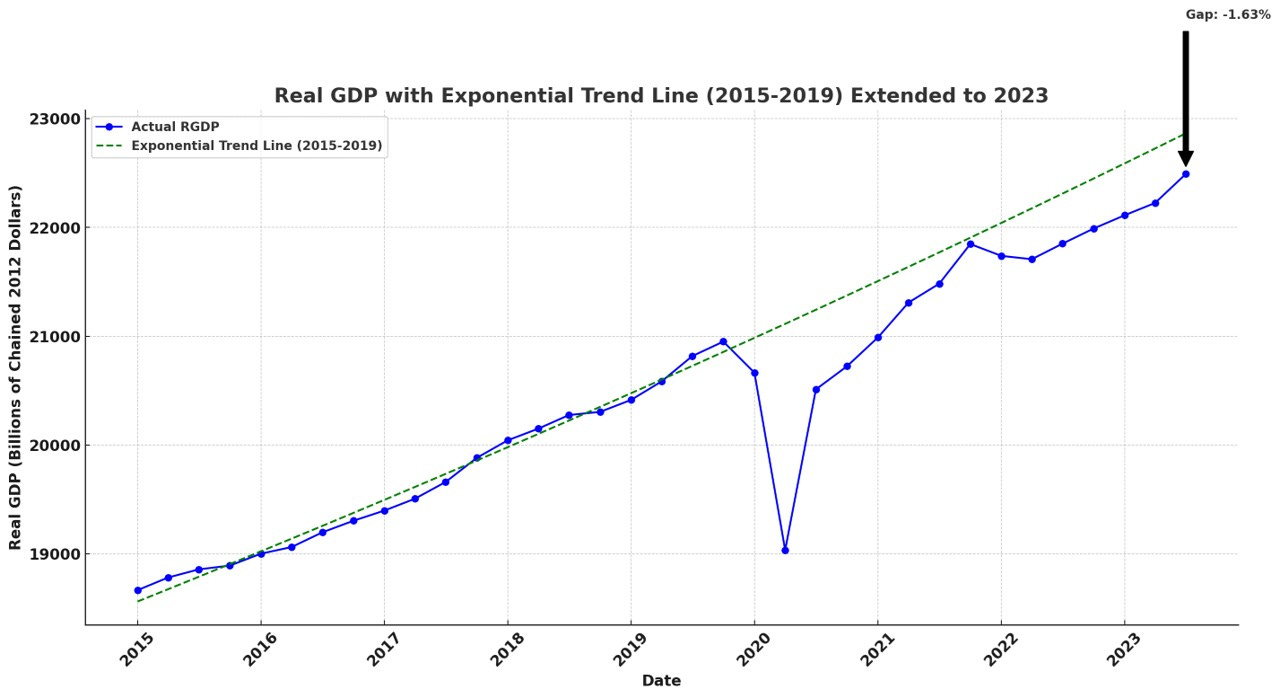

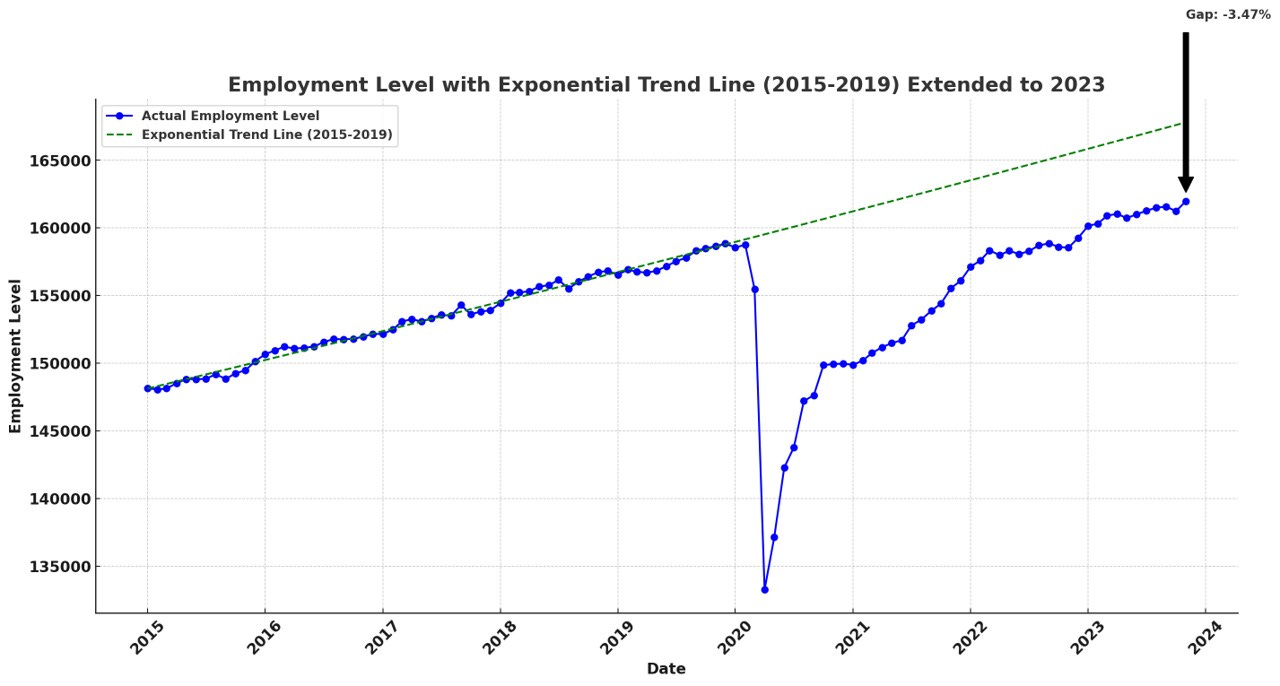

How much more healing can we expect for the economy? I recently pointed out that real GDP has not returned to its pre-pandemic trend. The same is true for the employment level.

It appears unlikely that real GDP will return to its previous trend line, without a productivity boom. That said, there is still room for healing of the non-labor supply side of the economy, as there are still wars and non-war related supply-chain shifts continuing.

For now, we’re still close to expected equilibrium, so the economy should continue toward its soft landing and subsequent recovery, sans additional shocks.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: