Stock and GDP Outlook, for Week Ending 07/01/2022

Real Improvement

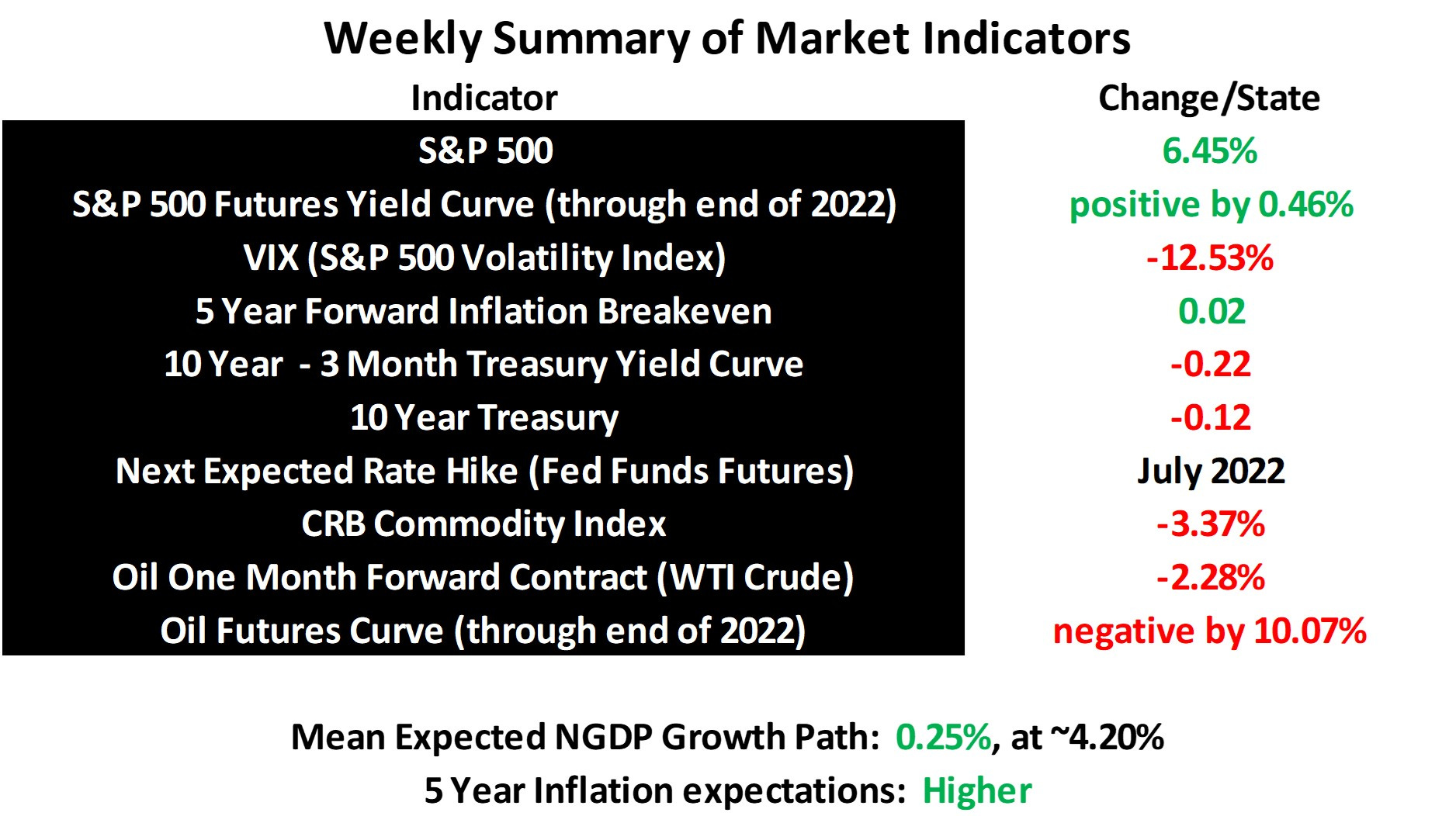

Last week saw yet another change in mean expected NGDP growth of over 2 tenths of a percent, but this time in a positive direction. Looking at the relative changes in inflation expectations and commodity prices, it was obviously mostly due to a rebound in real growth expectations. This is just another reminder of the uncertainty of this period for the economy and markets. It’s at least the greatest uncertainty since 2008, when an even sharper broad commodity shock combined with tight monetary policy led to the Great Recession.

So, what’s the outlook for markets at this point? I’ve complained repeatedly about the vagueness of the Fed’s average inflation targeting regime, and public statements I read from FOMC members don’t seem to help provide any clarity. What to make of an asymmetric average inflation target of 2%, with no specific information about how asymmetric it can be, and with no time frame specified? At least we’re pretty sure we’re at full-employment, given the real capacity of the economy at the moment, so we don’t have to consider employment, as part of their dual mandate.

One guess is that, given that the 5 year inflation breakeven is near 2.5% right now in core PCE terms, assuming the Fed has perfect credibility, they might bring the expected mean NGDP growth path down another half-percent or so. That would bring the expected growth path down to 3.7%, and mean a nearly 12% further decline in the S&P 500. That would also satisfy NGDP level targeting types who want to see the NGDP growth path return to the pre-crisis trajectory, if the Fed holds the path down long enough.

That also assumes, of course, an absence of additional real shocks, which is unlikely. Unfortunately, I think that’s the best that can be done in terms of guesses at the moment. These numbers should be treated as very fuzzy, as part of back-of-the-envelope spectulation, but then that’s always true of the outlook on this blog.

Perhaps a better way of putting it right now is, if one expects some positive real shocks in the near future, one can be bullish at the moment. Otherwise, there seems every reason to be bearish for the time being.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data