Stock and GDP Outlook, for Week Ending 05/27/2022

Stock and GDP Outlook, for Week Ending 05/27/2022

Are we in recession?

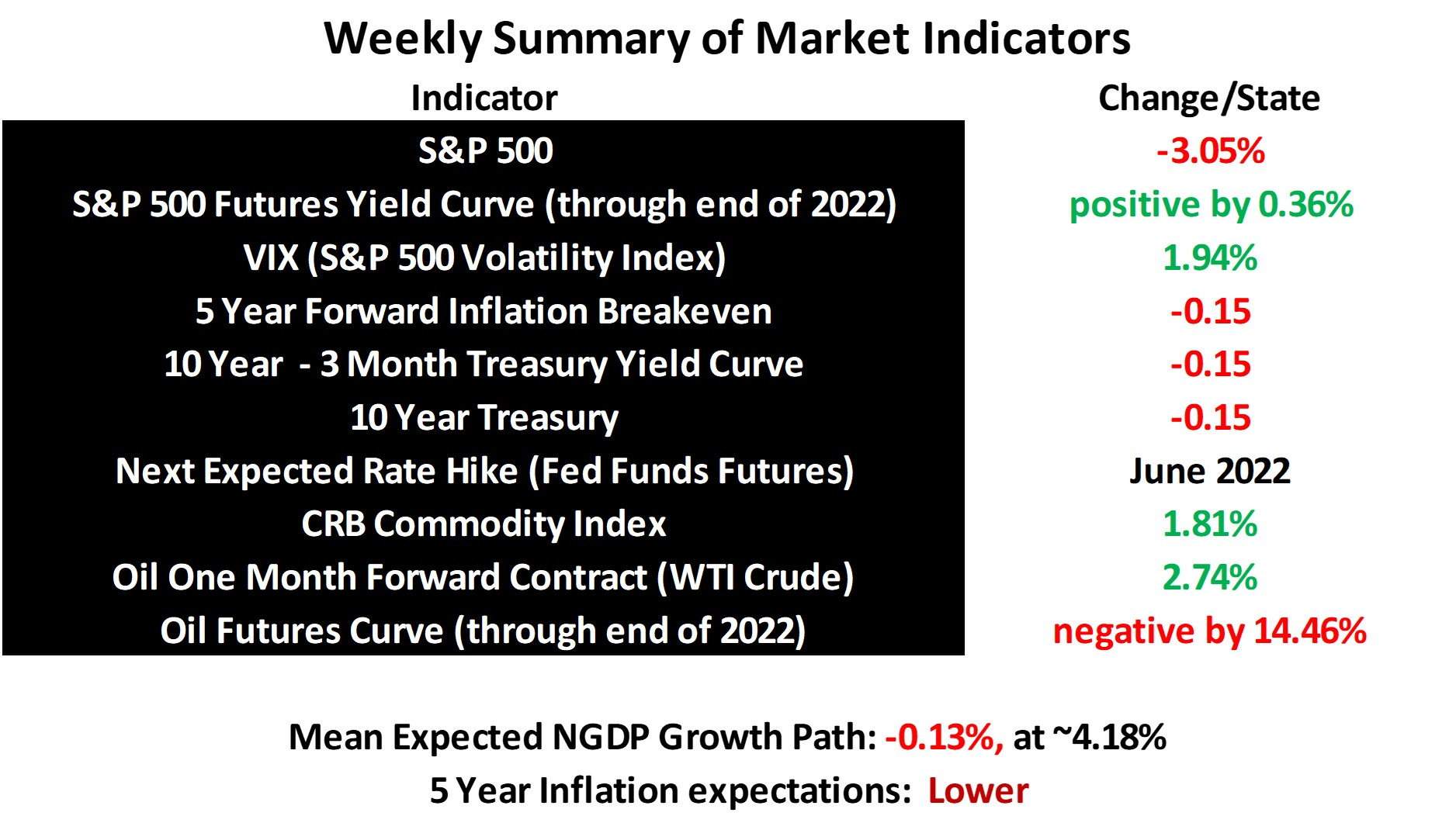

Stock prices fell again last week, along with aggregate demand, as the mean expected NGDP growth path continued its regression back toward 4%. Exactly how much lower the expected growth path will go is anyone’s guess, but it seems likely that it will not fall too far below 4%, and very unlikely that it will fall to 3% or below. Hence, the downward trajectory of the S&P 500 is likely getting close to its lower limit, unless the Fed surprises us all in a big way. That said, if the mean expected growth path falls to 3.5%, the S&P 500 still has nearly another 20% to decline. That would most certainly put us into a deeper than average recession.

But, the question on the top of many minds now is whether we’re in a recession or might be soon. In previous recent posts, I’ve acknowledged rising recession risks, but still thought the prospect unlikely. This is an increasingly difficult question to answer, however.

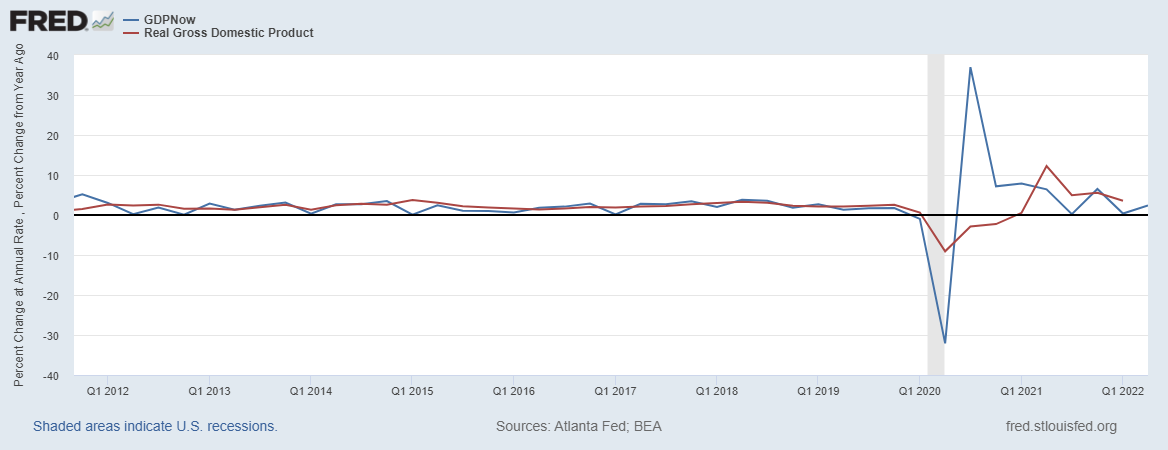

This is because, for one thing, while my imputed falling mean NGDP growth path indicates how much to subtract from present NGDP growth, it is unknown what the prior expected growth rate was for this quarter, for example. There are obviously forecasts, including the Fed’s GDPNow tool, but it’s been less reliable since the beginning of the pandemic.

I know of no market-based forecast that specifies the expected growth rate for a given quarter.

Also, of course, most define a recession as a period of negative real GDP growth that lasts at least 2 consecutive quarters. So, even if the prior expected NGDP growth rate for the oresent quarter were known, it would not tell us exactly what the expected real growth rate was. By the way, I tend to discount the weak first quarter GDP growth, because weak numbers aren’t unusual in Q1.

The 5 year inflation breakeven is down 46 basis points so far this quarter, and real GDP is typically much less sticky than core inflation. It’s thus not implausible that we’re in recession or will be soon, but I’m still not convinced. I wish I could be more certain.

Under ordinary circumstances, i.e. NGDP growth averaging a bit over 4% annually, and hence averaging around 1%-per-quarter(and ignoring seasonality), we would be very close to recession right now, but circumstances aren’t ordinary. We have a combination of real positive demand and negative supply shocks, coupled with formerly looser monetary policy now followed by nominal demand shocks. There is more uncertainty about the current moment than usual.

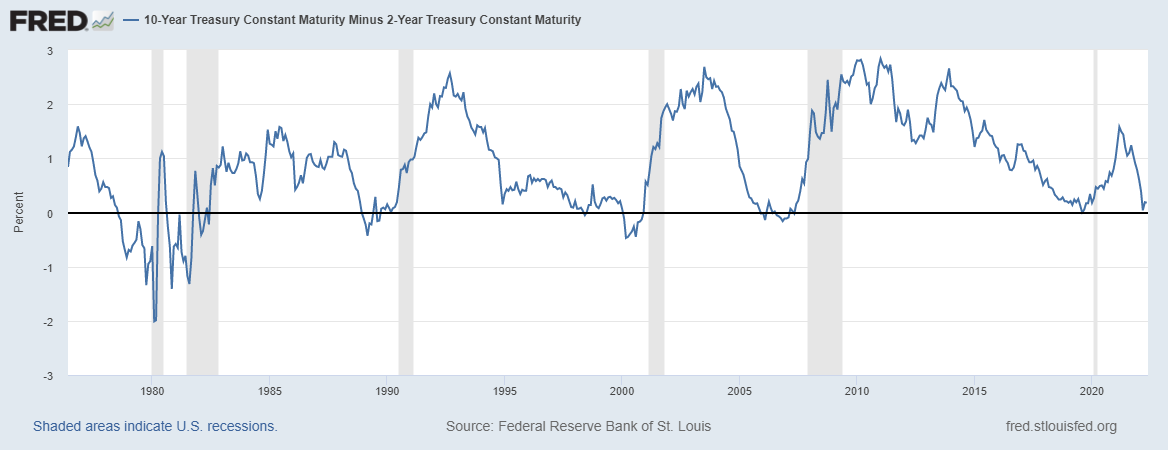

What about other indicators, such as the yield curve? While every modern recession has been preceded by an inverted yield curve, an inverted yield curve doesn’t always predict recession.

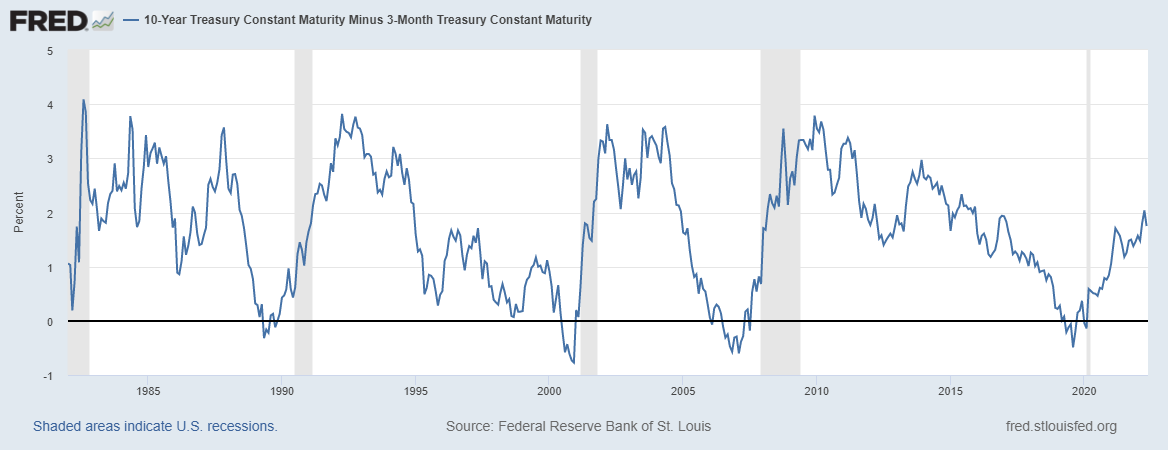

Yes, the 10 year minus 2 year Treasury yield curve was slightly and briefly negative on April 1st, but particularly in a relatively high inflation environment, it certainly does not mean a recession is imminent. Also, the degree of inversion should be taken into account. That said, currently, the 10 minus 2 year yield curve is only 18 basis points above zero.

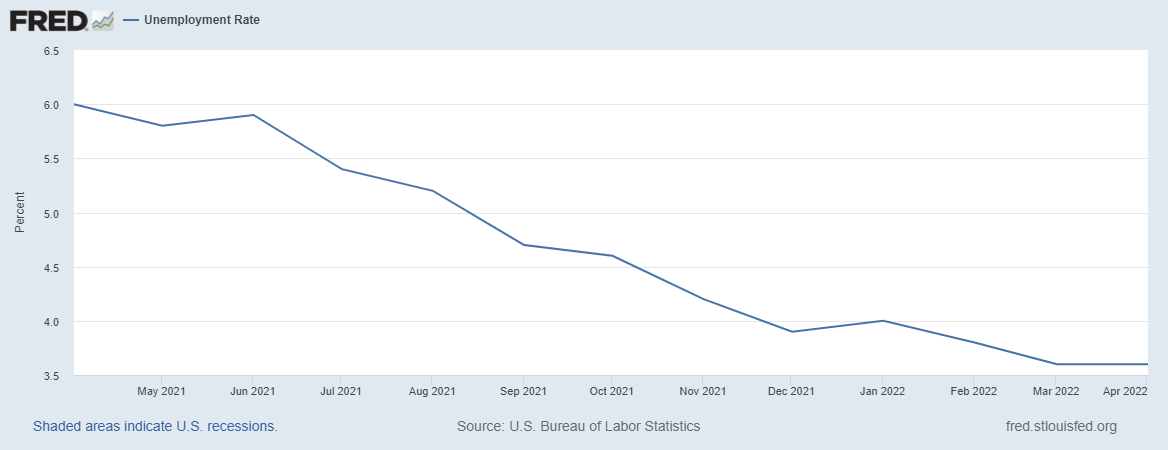

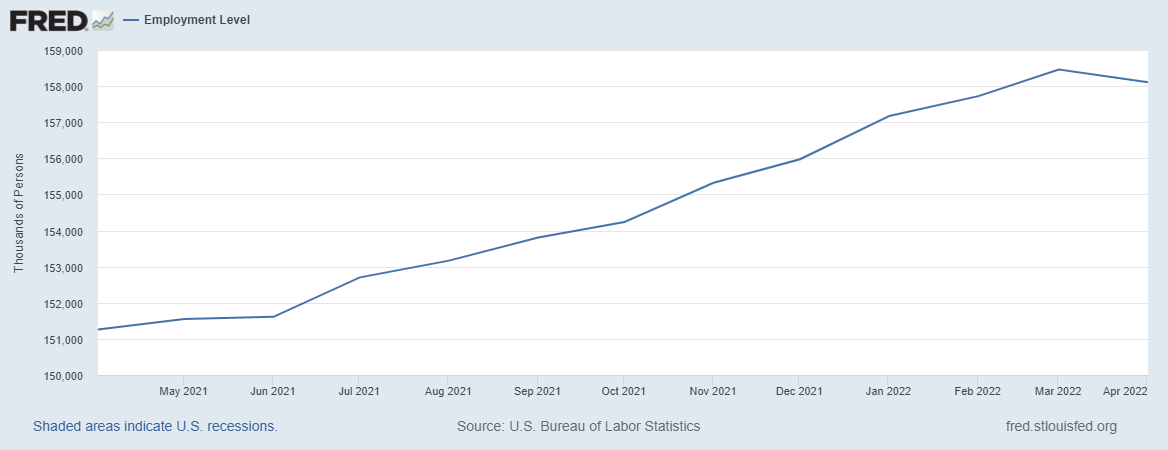

Lastly, I consider employment data. The unemployment rate was flat from March to April, with the unemployment level having fallen slightly over those two months. Also, weekly jobless claims have been rising lately(here and here). Alone, this is not significant enough data to draw any conclusions, but taken in context with other data, it is at least consistent with an economy being close to or in recession.

Sans large positive supply shocks, a recession in the near future would be unique in that the Fed won’t necessarily begin trying to loosen policy quickly, given that inflation could remain above its desired target. This could be an “interesting” situation to observe.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data