Stock and GDP Outlook, for Week Ending 02/09/2024

The Goldilocks Convergence

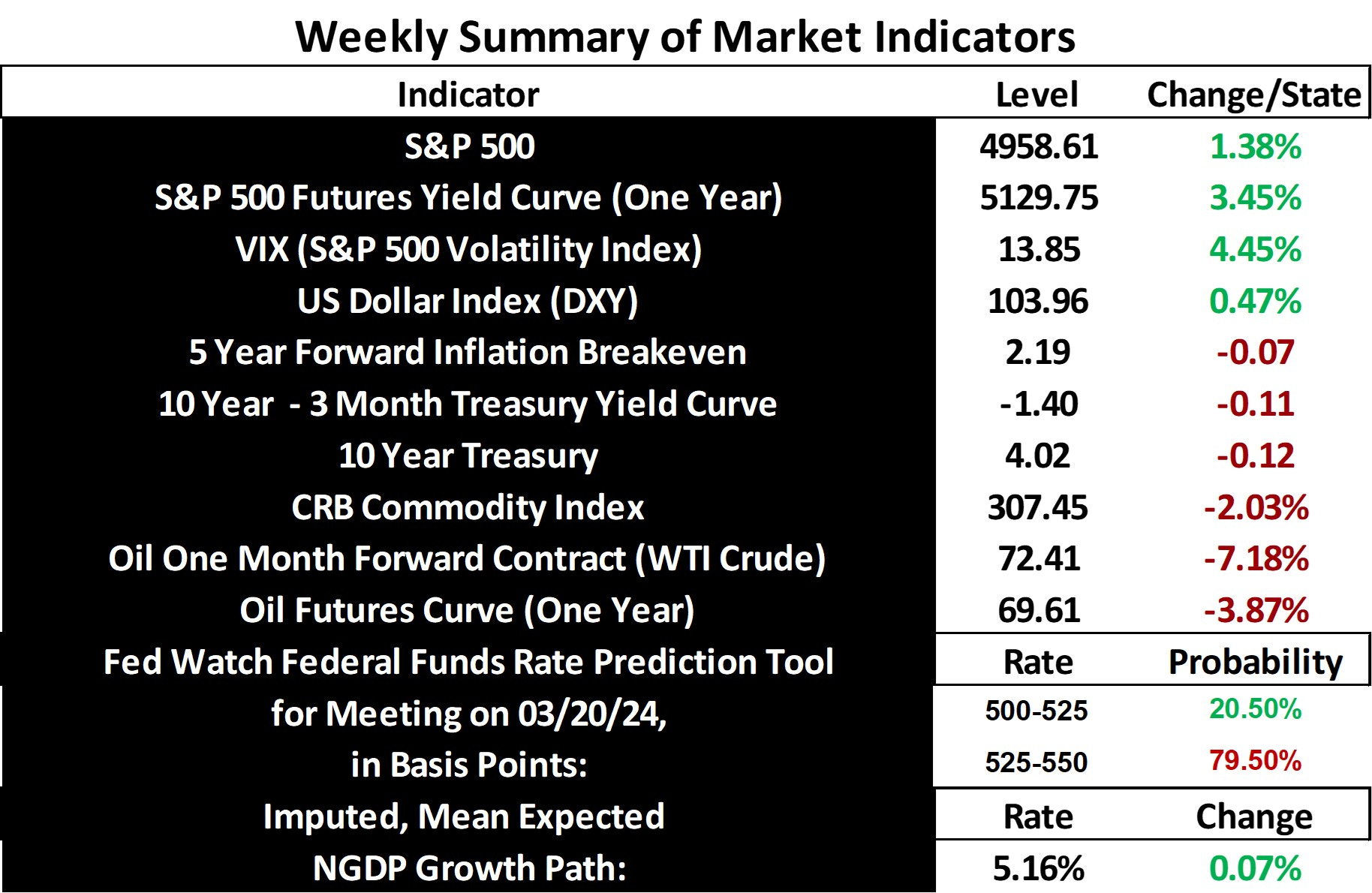

Another week, another net positive real shock. The S&P 500 and the mean expected NGDP growth rate rose yet again, with the former charging further into record territory. This was as inflation expectations declined, along with Treasury yields and commodity prices.

The boost in outlook was due in part to an extremely strong January jobs report, which vastly exceeded expecations. Hence, even a large downward revision could leave this number in the positive surprise range.

The only negative for forward-looking indicators was with respect to the VIX, which is continuing a recent upward trend. This is perhaps largely associated with growing geopolitical risks that could acutely affect commodity prices and international shipping. The spread and escalation of violence in the Middle East is of particular concern. For now however, the US economy still seems to be in the cliched “Goldilocks” state, as I’ve covered in detail in recent weeks, with seemingly wide and growing concurrence from other observers.

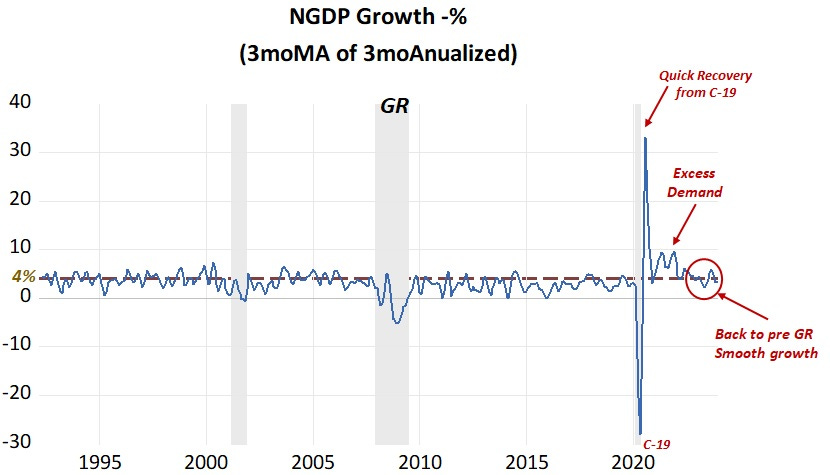

One concurring observer is Marcus Nunes, who shared a new indictor he developed recently that illustrates this point. This is the 3 month moving average of the 3-month annualized change in the NGDP percent change rate.

However, he’s not new to the Goldilock’s perspective, having been a leader in this view, rather than a convert. His blog is very much worth reading regularly.

Last week, I addressed the fact that the Fed Funds Futures curve suggests that economic growth might slow until 2026, before picking up pace later that year. I suggested a J-curve with respect to an AI productivity boom as one possible explanation. Of course, there are many other possible explanations or combinations thereof, including expectations for increased immigration or the beginning of a fiscal crisis, to name just a couple. The plausibility of an expected fiscal crisis is undermined by what is still a less than 1% implied default probability in 5-year credit default swaps, for example. Hence, it seems the apparent expected acceleration in nominal growth is likely due to expectations for a stronger real growth.

Even given that the economy seems roughly in equilibrium, there is still potential for significant increases in stock prices, due to continued supply-side healing and the potential for reduced geopolitical risks. As I pointed out a few weeks ago, commodity prices are still roughly 50% above their pre-pandemic levels, for example. Also, there can always be positive technlogy shocks, particularly in this era of accelerating innovation. And, even if the economy is above equilibrium, but inflation is not above target, there can still be room for the bull to run.

So overall, markets obviously still see the upside prospects outweighing the growing potential risks to growth, and I increasingly learn to argue with markets less as I age.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: