Stock Market Blues

The stock market has been rather rough since mid-February, and particularly during the last two weeks. While I wouldn’t say the market is crashing yet, it’s certainly on a downward trend with increased volatility.

I gave the Fed credit for the S&P 500 index at least exceeding it’s pre-crisis trend during the first year of recovery after a deep recession. This was certainly progress. Average inflation targeting is somewhat of an improvement over straight inflation targeting, but how much progress does it really represent? Sadly, the likely answer is, not much.

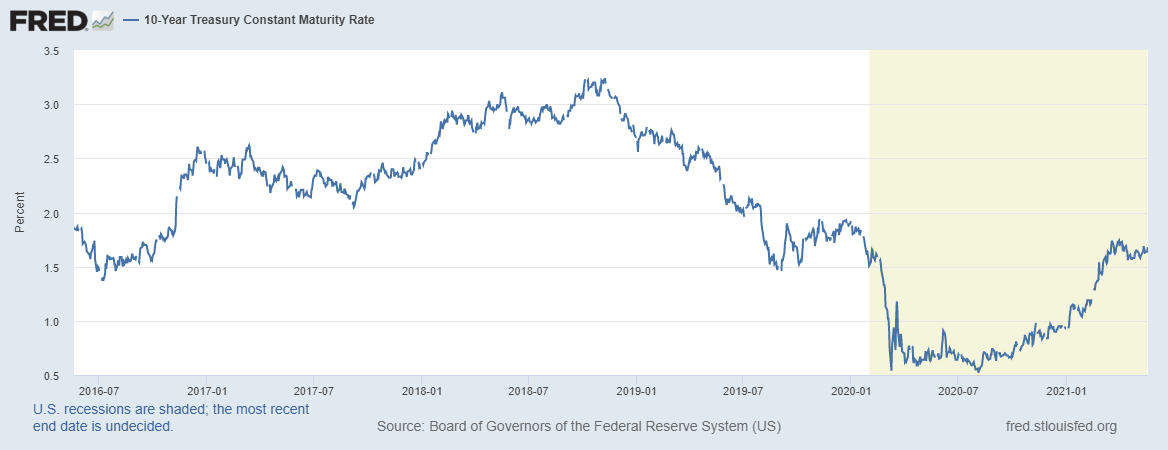

Consider two simple facts. First, as mentioned above, the S&P 500 is above its pre-pandemic trend. Second, however, the 10 year Treasury rate, for example, is roughly only half its pre-Covid level. The interpretation seems straightforward.

That is, earnings growth is likely not expected to return to the pre-crisis trend, because NGDP growth is not expected to return to trend. Most of the price performance of the stock market during this recovery has been due to a lower discount rate.

What about the stock market crash prediction, based on my signal indicator? It is not sending as strong a signal as it did in late February and early March, but one should be very cautious in this market. It remains to be seen how reliable this indicator is in the era of average inflation targeting.