Stock Outlook, GDP Forecast, and the Week Ahead, for Week Ending 06/18/2021

Stock Outlook, GDP Forecast, and the Week Ahead, for Week Ending 06/18/2021

Bump?

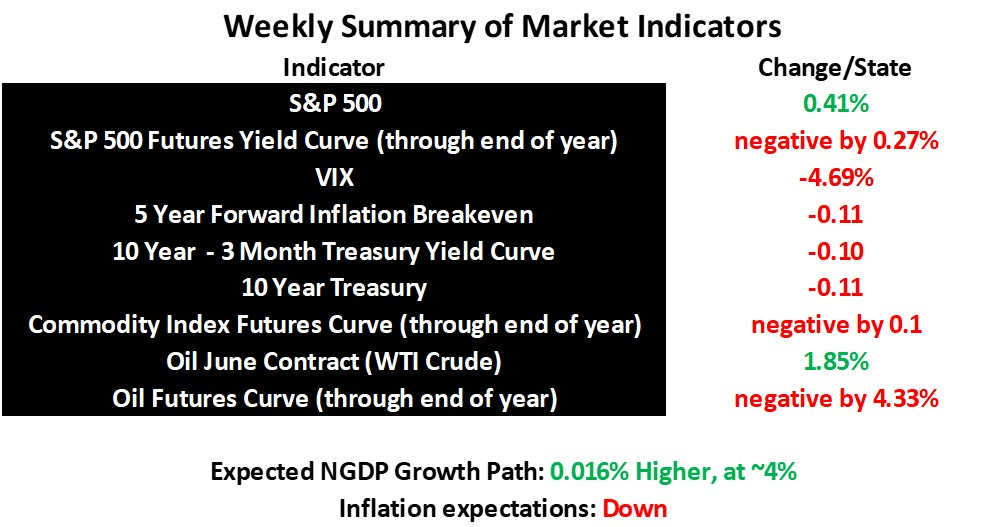

The S&P 500 rose near its trend weekly appreciation rate for the year-to-date, but there’s no reason to expect this to continue. There was a slight bump up in real GDP growth expectations, and inflation expectations fell. That probably won’t happen most weeks for the remainder of this year.

S&P 500 futures reflect the market expectation that stock prices will remain flat at best for the rest of the year, and will probably fall somewhat as the year progresses. While oil prices were up, the futures curve is negative for the second half of the year.

This is the result of market estimates of the Fed’s limited tolerance for average longer run future inflation, which as I stated previously, seems to be somewhere around 2.25%. They state willingness to tolerate higher inflation over the short-run, as the economy heals from the real effects of the pandemic. Among these real effects are supply shortages and bursts of pent up demand.

Hence, there’s no reason to believe the implicit long-run NGDP growth path will vary much from about 4% anytime soon, is about 1% lower than required to get closer to monetary equilibrium. Monetary equilibrium, theoretically, balances the supply and demand for base money.

So, as I’ve stated for weeks now, don’t expect the S&P 500 to vary by more than +/- 1% this week, unless something materially changes.