Stock Outlook, GDP Forecast, and the Week Ahead, for Week Ending 08/27/2021

Stock Outlook, GDP Forecast, and the Week Ahead, for Week Ending 08/27/2021

Tapering returns

Last week ended in a sea of red for stock investors, as the Federal Reserve indicated they could begin tapering QE purchases before the end of the year. While it wasn’t a scary week, it was a reminder that though the economic recovery has been very consistent, it isn’t guaranteed.

That said, if the S&P 500 earning yield returns to its pre-recession level, the price level for the index should reach about $5300, with earnings of about $225. It won’t be surprising to many if this level is reached, but when will it happen?

If the trend prior to last week continues, we’ll reach that level in a little less than 3 quarters, meaning roughly early May of next year. If S&P 500 earnings for the prior quarter are on this trend, we should expect to see a number around $46, if not more, due to a temporary surge in demand. That is close to the earnings reported in Q1.

I want to be clear that if monetary policy weren’t somewhat tight, we’d be much closer to the $5300 level now. The Fed can’t affect the real factors related to the pandemic, but can boost earnings enough in future years to return stock market price growth to a trendline closer to its long-run potential. It’s great that the prices returned to the immediate pre-crisis trend line, but the market was already on a lowered growth trend at the time, due to money tightening before and during the 2018 trade war.

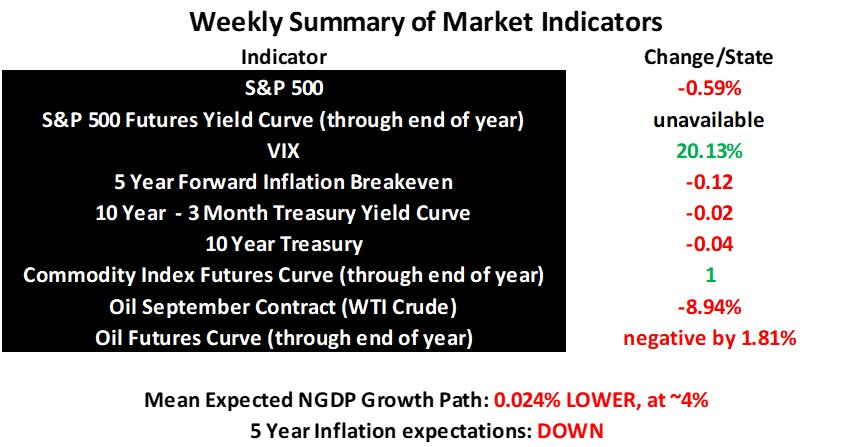

Data for the S&P 500 futures curve hasn’t been available as I write this, but it is still flat-to-negative, as it has been for months, unless something changed? In fact, it was negative going out for years. It’ll be interesting to see how this contradiction between these market forecasts and the trend growth in the S&P 500 price resolves. I’m betting that we’ll be closer to the growth trend than the flat-to-negative trend.