Stock and GDP Outlook, for Week Ending 03/22/2024

Stock and GDP Outlook, for Week Ending 03/22/2024

Topping Out?

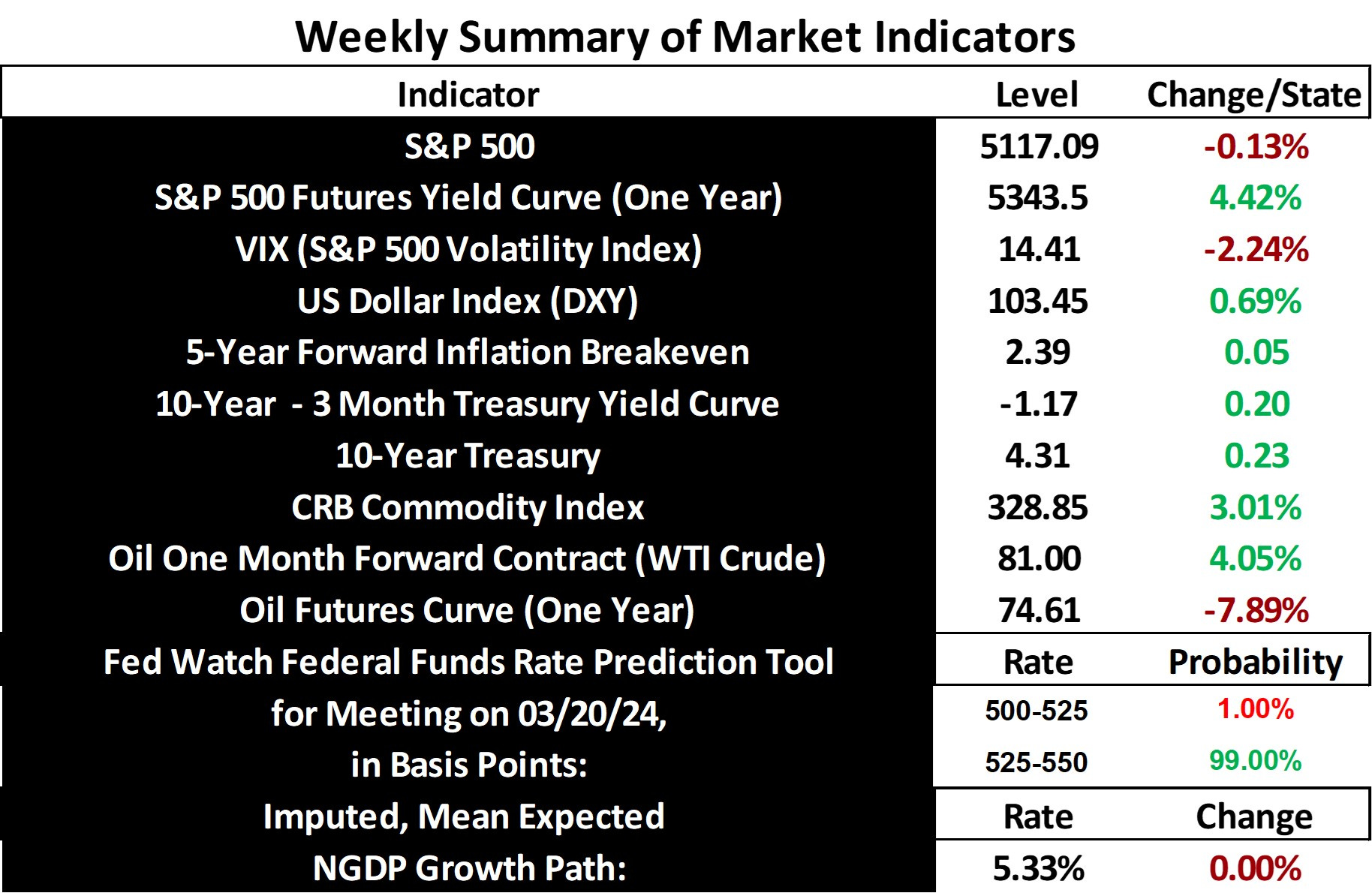

Stock prices and the mean expected NGDP growth rate declined for a second straight week, though just barely. The 5-year inflation breakeven remains slightly above the Fed’s 2% target in core PCE terms, so more resistance to the bull market run can be expected, sans more positive supply shocks.

There can always be such shocks coming from the AI field, as the pace of innovation appears to be accelerating. For example, this demo video released last week seems to represent amazing progress in humanoid robot development, despite having only integrated ChatGPT technology a mere 13 days prior. Of course, most impressive bench technology never even leads to a product, much less a successful one, so one shouldn’t overstate the accomplishment here. It is an impressive achievement, nonetheless, in a string of such achievements in recent weeks. For more examples, see here, here, here, and here. Despite these merely being well-planned demonstrations in highly controlled environments, it seems to indicate that some humanoid robots could start appreciably replacing human physical labor by the end of the decade.

This raises many questions, particularly in light of the immigration surge that is feeding the current real GDP boom in the US. Will such opportunities for immigrants greatly diminish within the next few decades? Will this kill the possibility of export-led development models that made Japan and South Korea wealthy? If economic growth does begin to rise at an increasing rate, economic policy mistakes could loom ever larger, partiularly for developing countries, potentially with irreversible consequences. The goal here is to point to potential pitfalls in what otherwise would seem to be an incredibly bright future for growth facilitated by AI.

For the time being, we still live in a world without this ever-accelerating growth trend. The US economy, though continuing to run hot, still has markets predicting return to equilibrium soon. Rather than rehash the various points I’ve made supporting this claim, I thought I’d share a recent blog post by Marcus Nunes, who makes the same point from a different perspective. If you’ve never read his blog, you should, if you like clear, concise arguments that are extremely well-illustrated and otherwise supported.

There will obviously be heavy focus this week on the FOMC meeting and decision on monetary policy adjustments. As you can see in the summary chart above, there is near market certainty that rates will remain unchanged, for now. I won’t be surprised if communication is issued that will suggest a delay in cutting rates versus expectations, which would be appropriate. However, I can’t claim to predict Fed behavior, beyond them displaying some minimum adherence to their mean inflation target. While I’m not predicting a move down in stock prices following their decision, it would not surprise me if it occurred.

So, while the outlook remains bright, caution is still called for, as the VIX is still elevated in the context of an overheating economy and heightened political and geopolitical risks.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: