Stock and GDP Outlook, for Week Ending 02/16/2024

Opportunity in Crisis

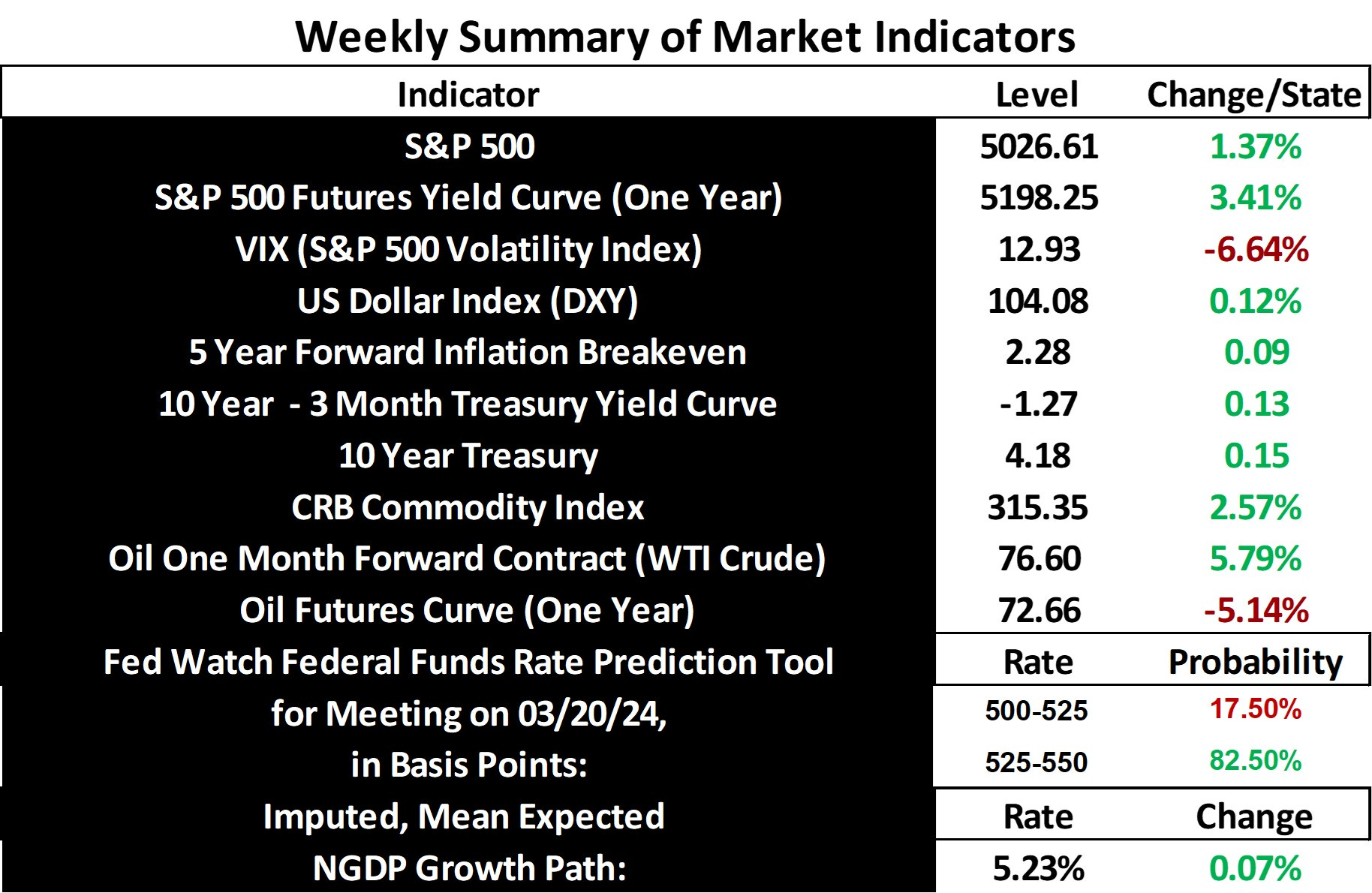

It is becoming cliché to say the stock market made a new high, but that’s what happened again last week, as the S&P 500 and mean expected NGDP growth rate both rose sharply. At this rate, 5000 will soon be a distant memory, with the next arbitrary threshold firmly in view.

Unlike last week however, this week’s rise was due to a net nominal shock, as commodity prices and inflation expectations ended the week higher. Inflation is still expected to remain within the Fed’s target range though, in core PCE terms. So, the Goldilock’s scenario persists.

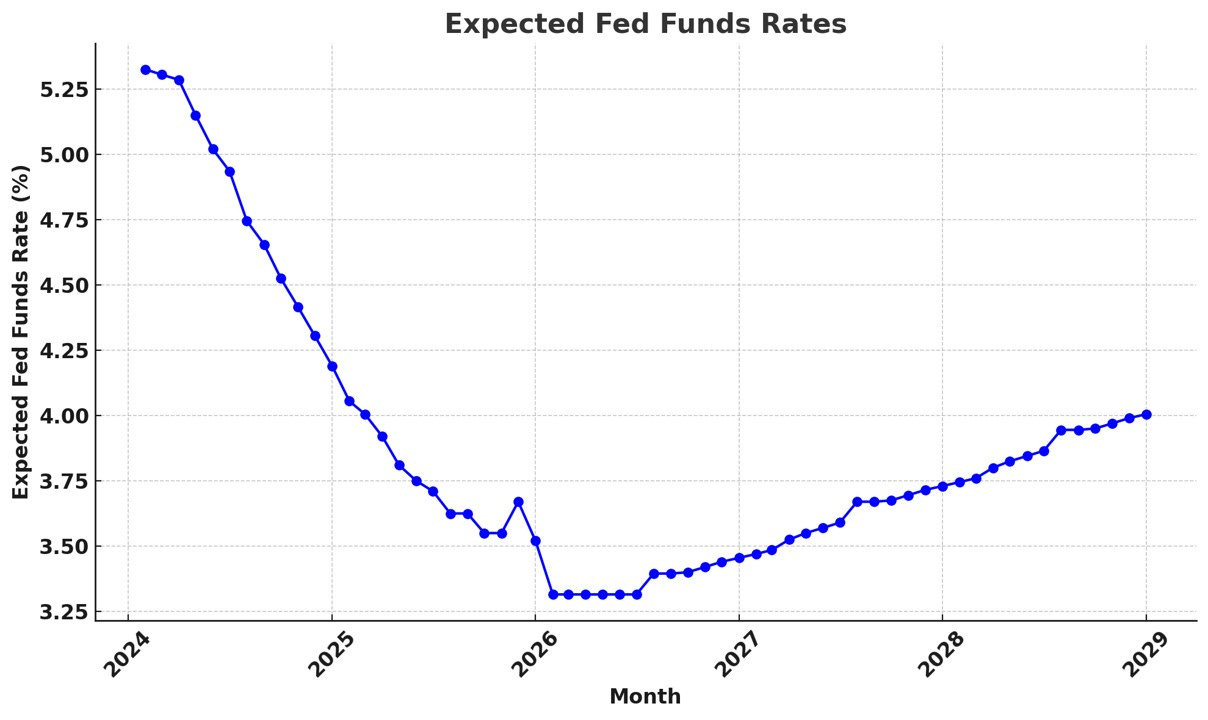

Last week, I speculated that expected increases in immigration might account for at least some of the apparent expected pickup in economic growth reflected in the positively sloped Fed Funds yield curve, starting in 2026. A CBO report issued last week credits increased immigration for at least some of the recent positive real shocks, and the expectation is that this trend will continue until at least 2034, adding $7 trillion to real GDP (HT: Scott Sumner). Not surprisingly, we’re benefitting from a real opportunity in that “crisis” at the southern border.

Of course, the economic projections in that report seem to conflict with expectations implicit in the the Fed Funds yield curve, with the former predicting a recovery beginning in 2025, rather than 2026. Markets integrate more information, more efficiently, and so should be better trusted.

In any event, if we add a positive immigration shock to the potential for more supply-side healing, and to the potential for a near-term AI-fueled productivity boom, the long-term economic outlook is indeed much better than prior to the pandemic. The usual warnings about seemingly rising domestic and geopolitical risks apply, but there could indeed be a considerably higher ceiling for stock prices than thought just months, or even weeks ago.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data: