Stock and GDP Outlook, for Week Ending 06/03/2022

Big Bounce

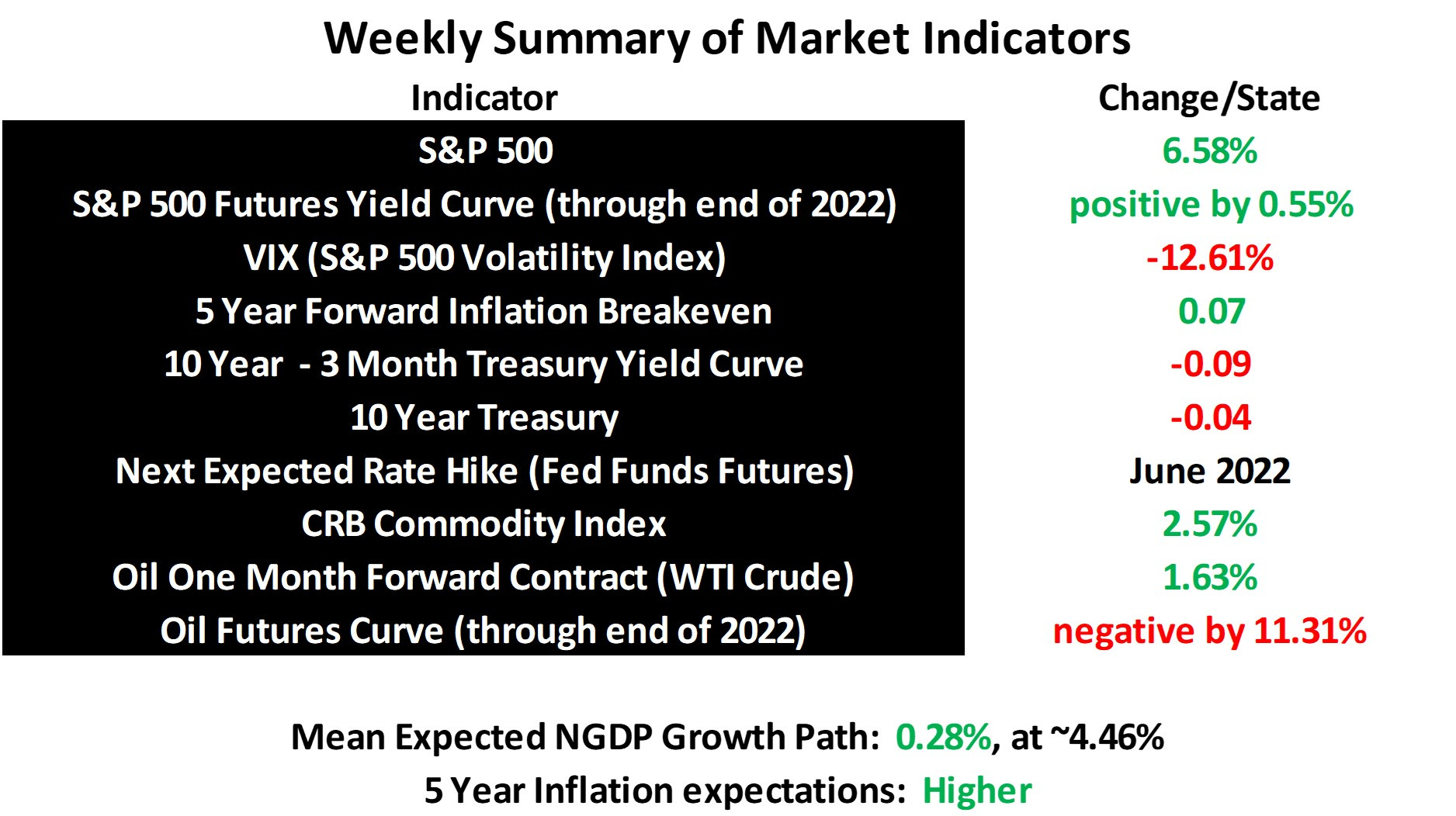

The jump in the implied mean expected NGDP growth path last week was significantly larger than the rise in expected inflation, indicating a relatively large increase in real growth expectations. This is despite rather large rises in commodity prices. This means the prospect for avoiding a US recession. which I addressed last week, have diminished, at least for now. Predicting the outlook going forward is as easy as predicting future events that will affect real growth and inflation, and the Fed’s reaction to them within a vaguely defined average inflation targeting framework. In other words, it’s child’s play.

And to add to the confusion, we really have no idea what the sustainable real GDP growth rate will be, after the supply shocks resolve. Many assume that rate will be around 2% or less, but I’m still skeptical about that assumption.

I refer again to the very optimistic view that I had when the year began, when I thought it likely, absent serious real or nominal shocks, that the S&P 500 would rise well above 5000. Of course, the Fed’s tightening cycle began just a few days later, and the war in Ukraine and pandemic-related lockdowns in China have further dampened real growth prospects for the foreseeable future.

I thought it likely that US productivity growth would surprise on a sustainable basis, despite noticeable supply-side damage due to the pandemic. This is due, in part to the increasingly wide spread adoption of early stage deep learning technology, which should result in a general productivity boom at some point. Hence, I was also skeptical of claims that inflation was too high from a monetary policy perspective, as inflation expectations were much tamer than current inflation, though rising.

I began to become concerned about inflation expectations myself, however, when the 5 year breakeven exceeded 3% in core PCE terms in March, as this made it more likely the Fed could lose its anchor on what I interpret as a 2% asymmetric average inflation target that takes employment into account. But, I never abandoned the possibility, as I also stated before, that even a 5 year inflation breakeven at more than 3% was not necessarily as bad as it looked.

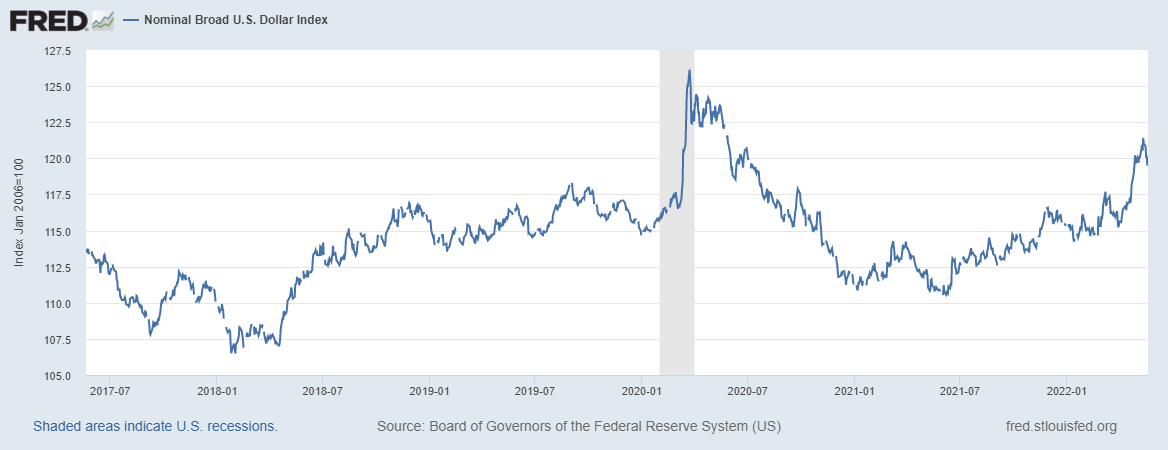

As one bit of evidence that may support that last point may be seen in the nominal broad US dollar index data:

If inflation really is seen to be sustainably too high relative to that of other currencies, why has this dollar index been rising since last summer? One possibility is that differential expected real US GDP growth is even higher.

The US isn’t the only country employing deep learning technology, of course, but might the US be employing it more quickly than other countries, as was the case during the internet boom of the 90s and early 00s?

Of course, this does not necessarily mean inflation rates aren’t too high, or at least that under the current Fed targeting framework, that running the economy this hot is without risks. But, it does suggest that perhaps we should be at least a bit more optimistic about the medium to long-term future.

Such questions wouldn’t matter to monetary policymakers under an NGDP level targeting regime, as I argued a couple of weeks ago. We could, as I’ve stated before, adopt a 4.5% target and simply maintain it. Monetary policy could be adjusted daily, a la economist Scott Sumner. The S&P 500 is a very good indicator of changes in the future expected mean NGDP growth path.

Note: This post, as is the case with all my posts, should not be construed as offering investment advice. Such advice should be tailored to the individual investor by qualified professionals who, ideally, are fiduciaries.

Links to Data